Investing in mutual funds is a popular strategy for individuals looking to grow their wealth while diversifying their risk. Thanks to Fintech, access to mutual fund investments has become simpler for both beginners and seasoned investors, contributing to the recent surge in mutual fund inflows.

The AUM of the Indian MF Industry has grown from Rs 10.11 trillion as of May 31, 2014, to Rs 58.91 trillion as of May 31, 2024, around 6 fold increase in a decade and more than a 2-fold increase in a span of 5 years. The total number of accounts (or folios as per mutual fund parlance) as on May 31, 2024, stood at 18.60 crore (186 million).

Indian Mutual Funds currently have about 8.76 crore (87.6 million) SIP accounts through which investors regularly invest in Indian Mutual Fund schemes. The highest inflows in the month of May 2024 have been in the Sectoral/Thematic category, which is Rs 19,213 crores as compared to other segments under diversified equity mutual funds.

[Read: Why You Should Declutter and Consolidate Your Mutual Fund Portfolio]

The rise in inflows in Sectoral/Thematic mutual funds may be attributed to the excitement surrounding the Lok Sabha 2024 election results and the predictions by various experts that the establishment of a Modi 3.0 government will benefit a wide range of companies, primarily those in domestic cyclical industries/sectors including infrastructure, manufacturing, capital goods, automobile, defence, energy and power, etc.

Many investors, especially beginners, fall into the trap of holding too many mutual funds (MFs) in their portfolios. It could be due to the tendency, which often stems from a misunderstanding of diversification and the fear of missing out on potential opportunities like the recent one with the frenzy of the general election. This phenomenon, often called portfolio clutter or bloat, can hinder your investment goals.

At first glance, having a wide array of mutual fund schemes might seem like a sensible strategy. After all, each fund promises unique benefits, such as exposure to different market sectors, varying risk profiles, or specialised investment strategies. This diversity appears to spread risk and potentially enhance returns by capturing different market trends.

[Read: Diversification in Mutual Fund Portfolio-The Secret to Long-Term Investing Success]

While diversification is the cornerstone of investing, excessive diversification can potentially dilute portfolio returns. Moreover, unintentional overlap among various schemes within your portfolio is also a concern.

The Reality of Over-Diversification

- Duplication of Holdings: Many mutual funds, especially large cap or blue-chip funds, often hold similar stocks in their portfolios. Investing in multiple funds that have significant overlap can dilute the benefits of diversification without adding meaningful variation.

- Complexity and Monitoring: Managing a portfolio with too many funds becomes cumbersome. It requires constant monitoring of each fund’s performance, expenses, and alignment with your financial goals. This complexity can lead to decision paralysis and missed opportunities for portfolio optimisation.

- Cost Considerations: Each mutual fund incurs expenses, including management fees, administrative costs, and possibly sales charges (loads). Holding numerous funds increases the overall cost burden, which can eat into your returns over time.

However, what I’ve noticed is that investors, in their quest to select the best mutual funds or by participating in New Fund Offers (NFOs), often end up overcrowding their mutual fund portfolios. At PersonalFN, when we analyse the mutual fund portfolios of individuals, we often find that many hold over 30 schemes and multiple folios within the same fund house.

A common question arises: how many mutual funds should one invest in? This article delves into the considerations and strategies to help you determine the optimal number of mutual funds for your investment portfolio.

There are various factors that could influence the higher number of mutual fund schemes in your portfolio:

- Misguided Diversification: Diversification is a key principle in investing, aiming to spread risk across different asset classes. However, some investors misinterpret this and believe more MFs equal better diversification. They end up holding multiple funds with overlapping investments, achieving little additional diversification but adding complexity.

- Following the Herd: Investors might chase “hot” funds based on recommendations or past performance. This can lead to them accumulating funds with similar investment styles, negating the diversification benefit.

- Emotional Bias: Reacting to market fluctuations or chasing short-term gains can lead to impulsive purchases of new MFs. This emotional investing can clutter the portfolio and deviate from your long-term strategy.

- Lack of Financial Literacy: Without a clear understanding of asset allocation and risk management, investors might struggle to choose the right mutual funds and hold onto too many.

[Read: Here is Why Holding Too Many Similar Mutual Funds Can Drag Your Portfolio Returns]

Instead of spreading investments across numerous schemes, consider these principles to streamline and strengthen your mutual fund portfolio:

- Define Your Goals: Start by clearly defining your financial goals, risk tolerance, and investment time horizon. This clarity will guide the selection of mutual funds that best align with your objectives.

- Focus on Asset Allocation: Allocate your investments across different asset classes (equity, debt, and possibly others like gold or international funds) based on your risk profile. Within each asset class, select a few well-managed funds that complement each other rather than compete or duplicate holdings.

- Quality Over Quantity: Choose mutual funds with a proven track record of consistent performance aligned with your risk appetite. Look for funds managed by reputable fund houses with a clear investment philosophy and transparent communication.

- Regular Review and Rebalancing: Periodically review your portfolio to ensure it remains aligned with your goals and market conditions. Rebalance, if necessary, to maintain the desired asset allocation.

Let us find the answer to the question – ‘how many mutual funds should I invest in?’ with an example:

For instance, Mr A, a 30-year-old individual, has 20 mutual fund schemes in his mutual fund portfolio. Out of these, 4 are Equity Linked Savings Scheme (ELSS), and 6 are large cap funds, mid cap funds, and small cap funds 2 under each category, respectively.

Moreover, Mr A has invested in two sectoral funds offered by different fund houses based on a friend’s advice. Sector and Thematic funds bank on opportunities limited only to a specific sector or a theme. Last year, one of the relatives suggested a couple of debt funds, which, according to Mr A, had a high-return potential.

According to Mr A, the portfolio is well-diversified since the investment is diversified into multiple schemes from different asset classes and categories of mutual funds. But it’s important to realise that you should invest according to your suitability, not on the advice of friends or family or market trends. The portfolio of Mr. A is an illustration of simple over-diversification.

Diversification is primarily used to lower portfolio risk. However, you need to be aware of your risk tolerance and financial objectives before considering diversification. Like Mr A, if you hold 2 mid and small cap funds each despite having a low risk appetite, it would serve no purpose. Investing in equity mutual funds is a high-risk activity. Debt funds aren’t as risky as equity funds are, but they aren’t completely risk-free.

Do note that a mutual fund’s risk varies depending on each scheme’s management styles and portfolio concentration.

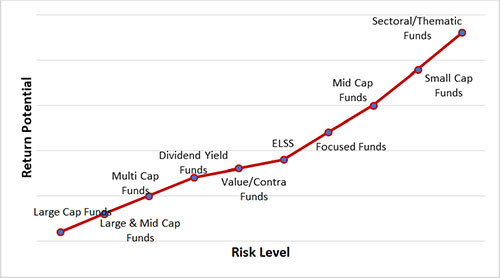

Graph 1: Equity Mutual Funds: Risk-Return Profile

(Source: PersonalFN Research)

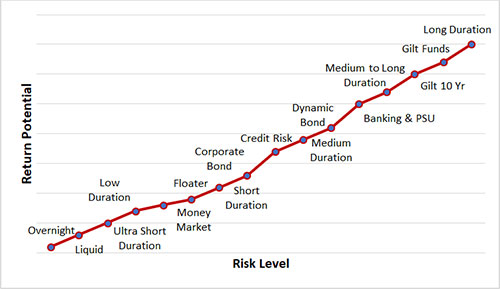

Graph 2: Debt Mutual Funds: Risk-Return Profile

(Source: PersonalFN Research)

The mistakes made by Mr A and how one can avoid them…

Mr A listened to everybody who offered investment advice, including relationship managers and relatives, without bothering to know if they were qualified to give investment advice. You may only consult with a SEBI-registered investment advisor and make informed investment decisions.

As mentioned earlier, it is crucial to invest in mutual funds based on your suitability; Mr A didn’t invest as per the financial goals and risk appetite. And missed out on several fund categories which would have offered a true diversification with decent returns.

For example, it would have made more sense to hold a multi cap fund instead of holding 2 schemes each in large cap, mid cap and small cap categories, respectively. Small and mid-cap funds occupied more than 50% of the portfolio-again, contrary to Mr A’s moderate risk appetite.

How Many Mutual Funds Should I Invest in?

There’s no magic number for the ideal number of mutual funds. It depends on your individual circumstances. Some experts generally recommend 5-10 well-chosen funds. This allows for diversification across asset classes like equity, debt, and gold while keeping the portfolio manageable.

You need to strike a fair balance across categories and sub-categories of mutual funds schemes. With a suitable asset mix (of equity, debt and gold), the returns of the portfolio are optimised; otherwise, it inflicts unwarranted risk.

The asset allocation resetting exercise, in which you may have to redeem from schemes of a respective asset class, may help trim a large number of funds in your portfolio:

1. Remove schemes with portfolio overlap

2. Redeem from schemes that do not align with your financial goals

3. Eliminate schemes whose objective and strategy have changed, as they may no longer be aligned with the investment objectives you invested with

4. Reset your asset allocation

5. Do away with consistently underperforming mutual fund schemes.

Broadly, when it comes to equity mutual funds, you should be fine with holding 5 to 7 of the best mutual fund schemes with distinctive investment mandates. When investing in debt funds, you need to prioritise capital over returns. You may choose schemes paying attention to your personal risk profile and liquidity needs/investment horizon.

Apart from holding equity and debt schemes, it would be sensible to tactically own gold in your portfolio (up to 10 to 15%) in the form of a gold ETF and/or gold saving fund, which are the smart ways to take exposure to gold.

[Read: Top 7 Equity Mutual Funds That Delivered Over 20% CAGR in Last 5 Years]

Strategies for Building a Mutual Fund Portfolio

You may consider adopting a Core & Satellite Approach, a proven investment strategy favoured by some of the most successful mutual fund investors worldwide.

In the prevailing market conditions, investing in Large-cap Funds, Flexi-cap Funds, and Value Funds as part of your ‘Core’ holdings, which account for about 65-70% of your equity portfolio, could be a prudent choice. This shall offer your portfolio a certain level of stability.

However, if an investor holds large and mid-cap and/or mid-and-small-cap funds as part of their ‘Satellite’ holdings, which could be 30-35% of the equity portfolio, they could generate substantial returns in favourable market conditions.

The allocation to each sub-category should align with your risk tolerance, financial objectives, and investment horizon. This strategy helps navigate volatile equity markets, emphasises time in the market, enhances portfolio stability, and has the potential to multiply wealth over the long term.

Remember: A well-diversified portfolio with a handful of well-chosen MFs is often more effective than a cluttered one with many redundant holdings. Focus on quality over quantity and prioritise strategic asset allocation to achieve your investment goals.

This article first appeared on PersonalFN here

{kind=link}