After the capital market regulator’s diktat on a stress test for small cap and midcap mutual funds issued earlier in March, the S&P BSE Small Cap Index particularly has corrected by -4.8% so far on a year-to-date basis (as of March 13, 2024).

The S&P BSE Mid Cap Index and the bellwether index, i.e. the S&P BSE Sensex (which represent larger companies on market cap), on the other hand, have shown resilience posting +2.0% and +0.7% absolute returns, respectively (as of March 13, 2024).

[Read: Do Large Cap Funds Make More Sense in An Overheated Equity Market?]

SEBI came up with the stress diktat for small cap and mid cap funds recognising the froth building up in the small and mid cap segment of the market. Soon thereafter, the Association of Mutual Funds in India (AMFI) directed the industry players to disclose the results of the stress test once in 15 days beginning March 15, 2024.

Here’s what AMFI wants fund houses to disclose to investors in small cap and mid cap mutual fund schemes:

- The liquidity of the portfolio. In other words, how many days would it take to liquidate or encash the underlying portfolio in case the fund faces heavy redemption pressure (in case of adverse market conditions). In this respect, nearly 80% of the portfolio’s liquidity details must be disclosed according to AMFI considering 10% Participating Volume (PV) and multiplying it 3 times.

- On the liability side, the percentage of Assets Under Management (AUM) of the scheme held by the top 10 investors.

- Percentage of the assets held by the fund/scheme in large cap, mid-cap, and small cap securities alongside the cash-and-cash equivalents in the portfolio.

- The volatility of the fund, wherein the fund should disclose its annualised standard deviation vis-a-vis that of the benchmark. This shall help you, investors to assess the risk taken by the fund compared to the risk of the benchmark.

- How sensitive is the fund’s portfolio relative to the market changes, which is measured by Beta.

- The valuations of the portfolio, wherein funds are asked to disclose a 12-month trail Price-to-Equity Ratio (PE) relative to the PE of the benchmarks.

- The portfolio turnover ratio of the fund/scheme to show how frequently the assets or underlying securities in the portfolio are bought and sold by the fund manager over a period of time. The higher the ratio, higher the churn. It sheds light on whether the fund manager indulges in momentum play or holds the portfolio with conviction.

The guidelines do not make it mandatory for AMCs to sell securities on a pro-rate basis (i.e. sell securities in the same ratio as the portfolio composition). However, it appears that abide the guidelines, mutual fund houses have already begun trimming or realigning the portfolio of small cap funds, particularly if there are illiquid stocks – and that’s why small caps (and some mid caps) are feeling the heat.

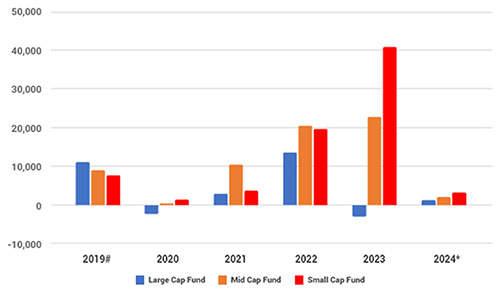

Fund houses are already restricting inflows or fresh money into small cap funds and mid cap funds in some form or other. This after over Rs 41,000 crore worth of inflows into small cap funds in 2023, double than the inflows seen in 2022 (see graph below).

Graph 1: Small Cap Funds and Mid Cap Funds Have Sparked Interest of Investors

The segment-wise data reported by AMFI is from April 2019 onwards.

(Source: ACE MF, data collated by PersonalFN Research)

Even now in 2024, investors are chasing small cap funds and mid cap funds, perhaps lured by the historical returns, which are in no way indicative of the future. Only in February 2024, inflows into small cap funds and mid cap funds have reduced by 10% and 12%, respectively, from the previous month.

AMFI CEO, Mr Venkat Chalasani, speaking to the media expressed that the intention of the regulator and the industry is not to stop inflow into small-cap funds but to enhance disclosure and transparency so that investors can make informed decisions while investing in these funds.

While the regulator hasn’t explicitly directed fund houses to moderate inflows into small cap funds and mid cap funds, in my view, the implicit message in an effort to manage the risk (amidst the froth) appears to be the same. In a sense, what the regulator is saying is: know your game; watch the stress building up and manage the risk well while you endeavour to achieve the state investment objective of the respective mutual fund schemes.

I believe, that just as every production unit has a capacity to produce goods and services with certain consistency, the asset management business also has a capacity. But in the race to garner more AUM, most fund houses are disregarding their capacity to manage their respective mutual fund scheme.

Even as there is froth in the small and mid-cap segments of the market and the margin of safety seems to have narrowed, many mutual fund houses in India are still accepting inflows into small cap funds and mid cap funds (as retail investors are drawn to them for higher returns).

As custodians of people’s wealth, asset management companies have a fiduciary role to play. The hard-earned money of investors needs to be handled thoughtfully being self-aware of the capacity. Asset management companies need to be prudent asset managers and not just asset gatherers.

You see, only when the fund houses recognise capacity the risk can be managed and could bring consistency to the expected results. Increasing the number of holdings in the underlying portfolio does not reduce risk. It is just a camouflage to accommodate increasing AUM. Too many holdings –say 100 or more — and less than 1% weightage in the stock is meaningless: it does not necessarily derive value or enhance the liquidity of the fund’s portfolio. The portfolio needs to be well-diversified and not over-diversified.

Moreover, a majority of the portfolio must be in liquid stocks. Liquidity is an important tool to mitigate the risk. Liquidity is a key criterion for smooth transactions and to ensure investors get their money back on time when there is redemption pressure.

Some fund houses complying with diktat have already begun disclosing the liquidity details of their small cap funds and mid cap funds:

- Nippon India Small Cap Fund – the largest small cap fund by AUM – can liquidate 25% portfolio in 13 Days, and 50% portfolio in 27 Days

- Quant Small Cap Fund can liquidate 25% portfolio in 11 Days, 50% portfolio in 22 Days

- Edelweiss Small Cap Fund can liquidate 25% portfolio in 2 Days, 50% portfolio in 3 Days

- DSP Small Cap Fund can liquidate 25% portfolio in 16 Days, 50% portfolio in 32 Days

- Axis Small Cap Fund can liquidate 25% portfolio in 14 Days, 50% portfolio in 28 Days

- Quant Mid Cap Fund can liquidate 25% portfolio in 3 Days, 50% portfolio in 6 Days

- Edelweiss Mid Cap Fund can liquidate 25% portfolio in 1 Day, 50% portfolio in 2 Days

- Nippon India Growth Fund can liquidate 25% portfolio in 4 Days, 50% portfolio in 7 Days

More small cap funds and mid cap funds will make the required disclosures as per AMFI’s advisory on risk parameters starting today (March 15, 2024) and will update the disclosures every 15 days.

As regards liquidity, we believe that at least 80%-90% of the underlying portfolio of a small cap and mid cap fund must be liquidated within 66 trading days. This ought to be the case, irrespective of the size of the fund.

[Read: Liquidity Check – Is Your Small Cap Fund Under Pressure?]

Even when the AUM increases, fund managers ought to pay attention to liquidity.

Investors, too, when adding a small cap fund and/or mid cap fund must pay attention to the liquidity of the fund’s portfolio. Only when the portfolio of a fund is built without compromising on liquidity you can win the game of investing. Glad that SEBI and AMFI have asked fund houses to make disclosures in this regard.

Keep in mind, that it is only when the underlying portfolio of the fund is liquid, it can be less susceptible to downside risk and can generate predictable returns.

[Read: Choose Predictable Investing When Adding Mutual Funds to Your Portfolio]

Ensure the small cap fund and mid cap fund (or any other fund for that matter) you own in your portfolio or considering adding, have robust portfolio characteristics without diluting the mandate of the fund. Ask yourself and/or your investor advisor or mutual fund distributor pertinent questions, such as…

- Does the fund have the capacity to take inflows?

- Will they ever put brakes on the inflows and when?

- Can it effectively handle AUM and do justice to investors?

- How liquid is the underlying portfolio of the fund?

These are critical questions, which you, the investor must have answers to.

In the exuberant phase of the Indian equity market, when the Indian equity markets are at a lifetime high, make a conscious decision to invest sensibly. Avoid skewing your portfolio only to mid cap and small cap mutual funds just because they are offering high return potential.

Keep in mind that for every level of return you seek, there is a certain level of risk you are exposed to.

Thus, invest in mutual funds (and other investment avenues) as per the asset allocation best suited for you. Avoid investing irrationally or in an ad hoc manner.

Invest in such a way that you are taking care of emergency needs (by having 12 months of regular monthly expenses, including EMI on loans in a liquid fund or a savings account), and then allocate to equity mutual funds taking cognisance of the risk involved, and holding some portion (around 20%) to gold as a portfolio diversifier.

Ensure your investment portfolio is on a solid financial foundation.

Be a thoughtful investor.

Happy Investing!

This article first appeared on PersonalFN here

{kind=link}