How do you select a mutual fund?

What is your thought process behind picking a mutual fund from more than 2,500 schemes available? Do you base your mutual fund investment on the popular children’s game “eenie meenie miney mo”? Or are you blinded by the star ratings given to mutual fund schemes?

Do you make mutual fund investments based on hearsay or advice from your relatives, colleagues or train companions? Or do you believe that selecting a mutual fund is a no-brainer?

After all, they are managed by expert fund managers, so what is the point of managing something that is already managed by experts, some of you might say.

Well, if your answer to any of the above questions is yes, then you are in for a surprise. Contrary to popular opinion and what distributors would like you to believe, all mutual funds are not the same.

They have different investment styles, strategies, objectives, risk-reward ratios, and investment costs that need closer examining. Selecting a mutual fund is an art and science that is tough to learn but rewarding in the long run.

You must learn the nitty-gritty of mutual fund investments to be able to zero in on the best mutual fund if you want to create a winning equity mutual fund portfolio.

How do you do this? By asking these questions every time you make a mutual fund investment. Ask yourself or your investment adviser/mutual fund distributor:

-

Is this mutual fund scheme really unique?

-

Is this fund really required in my portfolio?

-

Does this mutual fund investment match my risk profile, investment objective and time horizon?

-

Does this mutual fund investment fit in well with the asset allocation best suited for me?

A lot of hard work and analysis goes into every successful mutual fund investment, especially equity mutual funds. They are driven by market fundamentals and technical factors which change every day making selecting equity funds a tricky job. You need to perform both quantitative and qualitative analysis while selecting equity funds to build a truly winning and superior mutual fund portfolio.

[Bonus: Download 10 Steps to Create Winning Portfolio Guide for FREE]

Well, it is time you said goodbye to your old ways of selecting mutual fund investments blindly. In this article, we will discuss in detail how you should select top equity funds for your portfolio.

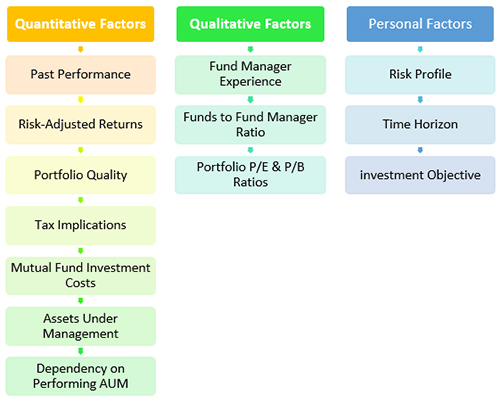

How to Select Best Equity Mutual Funds – Quantitative & Qualitative Factors Behind Successful Mutual Fund Investment

Let us start with quantitative factors, i.e. ones that deal with numbers. The first criteria to select quality mutual funds is ‘past performance’.

-

Past Performance: This is the first thing investors look at while selecting mutual funds. After all, the end goal of a mutual fund investment is to make money, i.e. to generate handsome returns.

Studying a fund’s past performance will help you set realistic expectations of its future performance. Note, we use the word set realistic expectations and not determine future returns. This is because the equity markets are constantly evolving and changing.

However, when you evaluate a fund’s past performance, ensure that you do not give undue importance to this aspect when making mutual fund investments. This is because past performance is not necessarily indicative of how the fund will perform in the future.

So, how do you analyse a fund’s past performance? There are three ways to do this:

-

Compare performance against the peers within the same Category and Sub-category: This is your mutual fund’s first test. If it cannot beat its peers consistently, then the fund is not worth investing in. But remember to keep the comparison fair. You should not compare apples to oranges, i.e. large-cap funds with mid or small-cap funds and arrive at a conclusion.

The below table shows the peer comparison for Axis Bluechip Fund, one of the best large-cap funds in 2021.

Axis Bluechip Fund Vs Large Cap Peers

Scheme Name Ratings 1-Year Return (%) 3-Year Return (%) 5-Year Return (%) Axis Bluechip Fund – Regular Plan – Growth

41.56 15.04 16.75 SBI Blue Chip Fund – Regular – Growth

47.82 13.68 12.71 ICICI Prudential Bluechip Fund – Growth 47.37 13.15 14.03 Mirae Asset Large Cap Fund – Growth

44.61 14.36 15.58 Aditya Birla Sun Life Frontline Equity Fund-Growth Unrated 49.30 12.43 12.34 HDFC Top 100 Fund – Growth Option Unrated 46.44 10.90 12.28 Returns as on 13th August 2021

(Source: ACEMF, PersonalFN Research)Now, Axis Bluechip Fund has actually underperformed its peers in the last one year, but look at its 3-year and 5-year outperformance. So, when you are making a mutual fund investment, lay emphasis on consistent long-term outperformance against peers.

-

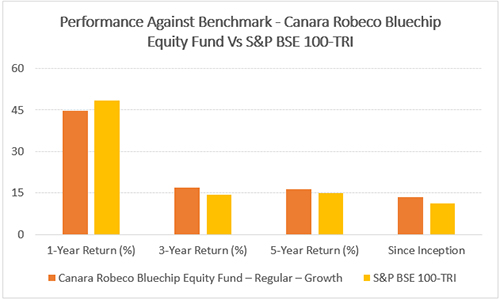

Compare the performance against Benchmark Returns: Every mutual fund scheme has a benchmark against which it tracks and evaluates its performance. The sole aim of an active fund manager is to beat the fund’s benchmark, i.e. to generate ‘alpha returns’. The logic is straight: if an actively managed fund cannot beat its benchmark, then investors would be better off investing in an index fund, which is passively managed and whose returns are almost in line with the benchmark. What is the point of ‘active’ fund management?

So, consistent outperformance against the benchmark is a must while selecting actively managed mutual funds.

The below chart shows Canara Robeco Bluechip Equity Fund‘s performance against its benchmark, S&P BSE 100 – TRI as of 13th August 2021.

Performance of Canara Robeco Bluechip Equity Fund Vs S&P BSE 100 TRI

Returns as on 13th August 2021

(Source: ACEMF, PersonalFN Research)Barring the last one-year performance, Canara Robeco Bluechip Equity Fund has consistently outperformed its benchmark. So, when you make your next mutual fund investment, ensure that your selected mutual fund is able to consistently outperform its benchmark.

-

Evaluate the fund’s Performance Across Market Cycles: Like us, even the equity markets experience different weathers. They have their share of bull phases and bear phases. A majority of mutual funds will perform well in a bull market because all stocks rally when there is euphoria.

But what happens when the overall market sentiment is hit by a negative event and there in panic? Is your fund capable of sailing through a bear market? This is exactly what you need to evaluate while selecting a mutual fund.

You don’t want a bull market hero or a bear market dragger. To make an evergreen mutual fund investment, you need to select a consistently well-performing mutual fund. Hence, it is critical to analyse a fund’s performance across bull and bear markets.

The below chart shows the performance of Mirae Asset Emerging Bluechip Fund across different bull and bear markets.

Performance of Mirae Asset Emerging Bluechip Fund Across Bull & Bear Markets

Bear Bull Bear Bull Bear Bull From 05-11-10 20-12-11 03-03-15 25-02-16 14-01-20 23-03-20 To 20-12-11 03-03-15 25-02-16 14-01-20 23-03-20 08-06-21 Mirae Asset Emerging Bluechip Fund -19.43 44.27 -9.93 23.35 -36.29 100.81 Category Average -26.06 31.34 -17.38 16.74 -34.73 86.3 Nifty LargeMidcap 250 Index – TRI -30.87 30.59 -17.80 16.84 -36.83 97.28 The Mirae Asset Emerging Bluechip Fund has performed well across both bull and bear markets. In the bull market rally between 23rd March 2020 and 8th June 2021, the fund generated a return of 100.81% against a benchmark return of 97.28%.

Mirae Asset Emerging Bluechip Fund has also limited the downside risk in a bear market. During the bear market between 3rd March 2015 and 25th February 2016, the fund fell by 9.93% while the benchmark fell 17.80%! So, the fund has managed to limit the downside risk.

So, while selecting a mutual fund investment, always study the fund’s performance across bull and bear markets.

-

-

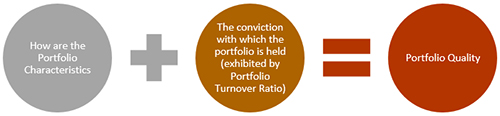

Portfolio Quality: This is the most important and often overlooked aspect of selecting a mutual fund. The performance of a mutual fund is extensively dependent on the quality of its underlying portfolio, i.e. stocks and other securities. If the underlying securities do well, your mutual fund is likely to reward you well, i.e. generate good returns.

A quality portfolio is reflected by:

-

The portfolio characteristics of the mutual fund scheme

-

And the conviction with which the portfolio is held – the fund should have a reasonable portfolio turnover ratio, not very high.

Adequate Portfolio Concentration shows the level of diversification in a fund. Is the fund manager overexposing the corpus to a few stocks only or is the corpus adequately spread across stocks from different sectors? The whole point of investing in mutual funds and not stocks is to benefit from diversification. So, when you select a mutual fund, ensure that it does not invest more than 50-55% of the corpus in the top 10 stocks.

Reasonable Portfolio Turnover Ratio measures the number of times stocks are bought and sold by your fund manager. Imagine a fund manager who constantly buys and sells stocks without even letting them realise their full potential. This results in high transaction costs which are taken from the funds’ assets. This leads to a high expense ratio, which is again borne by the unitholders. So, the next time you make a mutual fund investment, pay special attention to the fund’s portfolio turnover ratio.

-

-

Mutual Fund Investment Costs: Every good thing comes with a price tag. So, does your mutual fund investments. The two main costs borne by mutual fund investors are:

– Expense Ratio

– Exit Loads

Expense Ratio: A mutual fund is not solely about the fund manager. There are several moving parts and characters behind the screen which come with a price tag. The fund has to pay the salaries of fund managers, research team, bear marketing expenses, administrative costs, overheads, legal costs, etc., and all this you, the investor, pays for from your pocket in the form of an expense ratio.

However, there is a relief in this regard-courtesy the Securities and Exchange Board of India (SEBI). As per SEBI, equity mutual funds cannot charge more than 2.25% expense ratio. But as a prudent investor, it is your responsibility that while selecting mutual funds, you choose funds with a low expense ratio.

Exit Loads: Exit load is a penalty levied by the fund house on premature exit from the fund. It varies across different types of mutual fund schemes. Equity funds usually have an exit load period of one year, whereas debt funds, like liquid funds, have an exit load for a period as low as seven days. However, there are certain debt funds like the HDFC Credit Risk Debt Fund which comes with an exit load period of 540 days.

[Read More: What Should be your Debt Mutual Fund Strategy in 2021?]

Remember, exit load is not the same as a lock-in period. In the case of equity funds, you can redeem before one year after paying 1% as exit load. But if the fund has a lock-in period, like in the case of the Equity Linked Savings Scheme (ELSS), then you cannot redeem even after paying the exit load!

[Read More: Best ELSS Funds to Invest in 2021]

-

Tax Implications: Benjamin Franklin, the founding father of the United States, a writer, a political philosopher, printer, publisher, inventor, and scientist once famously said, “Nothing is certain in life but death and taxes.” Unfortunately, your investments in equity mutual funds are also taxable. Both capital gains and dividend income are taxable.

-

If you sell your mutual fund units before 12 months, you incur short-term capital gains (STCG) which are taxed at a flat 15%.

-

Whereas if you sell your mutual fund units after 12 months at a gain – referred to as Long Term Capital Gain (LTCG) – they are taxed @10% above Rs 1 Lakh in a financial year.

-

Dividend income was earlier taxed at the fund level, but post the union budget of 2020, dividend income is taxed 10% in the hands of the investor.

-

-

Assets Under Management (AUM): This is also referred to as the corpus of the fund. It indicates how big or small a respective fund is. Note that while a high AUM shows the funds growing popularity, it does not necessarily mean that it will translate into better returns. On the contrary, it may also hamper the fund’s ability to perform. This is because every mutual fund scheme has a certain capacity of fund management, beyond which it may not be able to generate returns efficiently.

When a fund has an enormous asset size, its fund manager may have trouble manoeuvring in and out of positions and investing in certain securities with lower trading volume or smaller market caps. But the degree to which asset size affects a manager’s ability to do his or her job depends on the type of fund and strategy its fund manager employs.

Pure large-caps funds may not witness a sharp deterioration as their fund size increases. Such funds usually adopt a buy-and-hold strategy, investing in top-quality blue-chip companies. As expected, larger funds tend to hold more liquid stocks than smaller funds, since larger funds deliberately avoid stocks with insufficient liquidity. Hence, the growth in AUM of such funds rarely affects the risk-return potential.

The problem arises with funds that invest across market-caps. A small fund can easily put all its money into its best ideas. Unfortunately, liquidity concerns force a large fund to invest in its not-so-good ideas and take larger positions per stock than is optimal, thereby eroding performance. Research findings suggest that liquidity is an important reason behind why size erodes performance.

Given the burgeoning size of some equity funds in India, it is best to assess the proportion of AUM actually performing. This will help you assess if the fund houses offering various mutual fund schemes, is a ‘prudent asset manager’ or an ‘asset gatherer’.

-

Dependency on Performing AUM: Many investors look at the fund’s AUM while selecting mutual fund investments. They believe that a fund with high AUM is always a winner. This is a wrong notion. While a fund with high AUM can ward off redemption pressure, it can also dilute your returns.

Imagine a fund with an AUM of Rs 20,000 crores spread across 20 mutual fund schemes. Of these 20 schemes, only 5 schemes are performing well and their collective AUM is Rs 7,500 crores only. The remaining Rs 12,500 crore AUM is invested in 15 poor-performing schemes. So, technically, 62.5% of the fund’s massive AUM is stuck in poor quality funds.

This is why you should not get carried away by a fund’s AUM. When it comes to your mutual fund investment, what matters is the quality of the AUM not quantity.

-

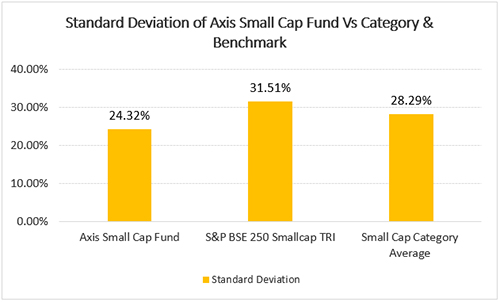

Evaluating Mutual Fund Risk: Mutual fund investments, especially equity funds come with their own inherent risks. The biggest risk in equity funds is market risk, i.e. when the fund moves up or down owing to a variety of factors. This risk of deviation from expected returns is measured using standard deviation.

A funds standard deviation tells you how much volatile or risky a fund can be compared to the benchmark and its peers.

The below chart shows the standard deviation of Axis Small Cap Fund against its peers and benchmark, S&P BSE 250 SmallCap TRI as of 13th August 2021:

Standard Deviation of Axis Small Cap Fund Vs Category & Bechmark

Returns as on 13th August 2021

(Source: ACEMF, PersonalFN Research)Axis Small Cap Fund has the lowest standard deviation at 24.32% against its benchmark’s 31.51% and small-cap category peers, 28.29%. Additionally, the fund has generated a Sharpe ratio of 0.96 against its benchmark Sharpe ratio of 0.51. Thus, it can be said that the fund has rewarded its investors well on a risk-adjusted basis. Fund performance being equal, you should invest in funds with a lower standard deviation.

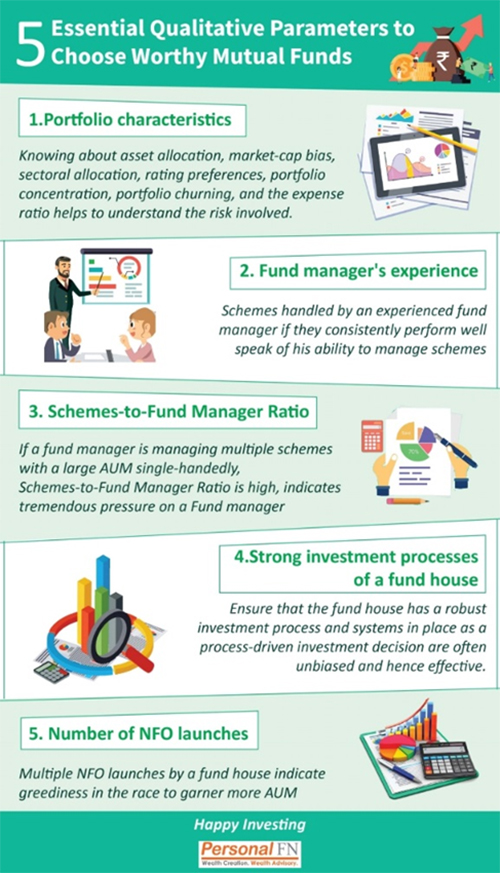

How to Select Mutual Fund Schemes – Qualitative Factors Behind Successful Mutual Fund Investments

Quantitative factors are easy to find and analyse while selecting mutual funds. But the real art is to discover and analyse the hidden qualitative factors. There is more than mere number-crunching involved in selecting best mutual funds.

You need to study the portfolio characteristics of a mutual fund scheme in-depth, understand its investment strategy, credentials of the fund management team, the schemes-to-fund manager ratio, among many other facets.

Evaluating these hidden qualitative factors is crucial while selecting mutual funds.

-

Experience of the Fund Manager: Will you be comfortable navigating treacherous terrain with a driver holding a learner’s license? Absolutely not!

An equity mutual fund investment is no different than that treacherous terrain. An equity fund goes through various ups and downs and hence you must assess the experience of the fund manager.

Apart from knowledge and market experience, the fund manager’s approach should be void of investment biases and he/she must be quick to accept and rectify his/her mistakes. He/she ideally should adhere to the investment processes & systems set out by the fund house. There have been instances where fund managers have stuck to poor-quality stocks due to their personal biases. Such fund managers and funds should be avoided at all costs. Remember, the fortune of the fund is closely linked to how it is managed by the fund manager/s.

-

Schemes-to-Fund Manager Ratio: Imagine if Virat Kohli was tasked with scoring a triple hundred in all test matches. He is after all one of the best batsmen in the world. Will he be able to do it? In all probability, no! The same is true for fund managers as well.

You might have noticed fund managers handling multiple schemes. When the same fund manager is managing multiple schemes, there are high chances of inefficiency kicking in. This is because, just as a fund has capacity in terms of the AUM it manages, a fund manager too can manage only a certain number of schemes. The fund can also suffer from high portfolio overlap.

Neelesh Surana is the fund manager of Mirae Asset Emerging Bluechip Fund and Mirae Asset Tax Saver Fund. Can you guess the portfolio overlapping between these two funds? 75%! Yes, these funds share 75% of their stocks. So, what’s the point of investing in both the funds together?

This is why you must ensure that a single fund manager does not manage more than five schemes at the same time.

-

Price to Earnings (P/E) & Price to Book Value (P/BV) Ratio: Mutual funds derive their value from the underlying securities held in the portfolio. This is why you must study a funds P/E and P/B ratio while selecting an equity mutual fund scheme.

Price to Earnings ratio tells you the price you are paying for a share in the company’s earnings. Whereas price to book value ratio evaluates the price you paid for a company’s net assets, i.e its book value.

In the case of value funds, you will the underlying securities to have low P/E and P/BV ratios while growth-oriented funds don’t mind buying stocks at high P/E as they envisage high and quick growth potential in them.

[Read More: Best Value Funds to Invest in 2021]

So ensure that when your fund says it’s a value fund, it is following value style investment strategy only.

This covers our discussion on how to select equity mutual funds for your portfolio. While we have discussed the qualitative and quantitative aspects in detail, you should also pay attention to general factors. These factors are personal to each and every investor.

Three General Factors to Consider While Selecting Mutual Funds

-

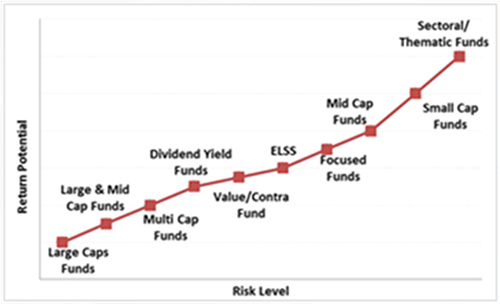

Risk Profile: Risk profiling is the most overlooked factor while selecting a mutual fund. Will you be comfortable sky diving if you suffer from vertigo? In all probability, no. Similarly, if you do not have the apetite for high risk, then you should stick to large-cap funds and not foray into mid or small-cap funds no matter how exciting they may look. The chart below shows the risk levels of different types of mutual fund schemes:

Risk – Return Ratio of Different Types of Mutual Fund Schemes

Note: For illustrative purpose only

(Source: PersonalFN Research) -

Time Horizon: This is a key element of any mutual fund investment decision. If your time horizon is three to five years and you wish to take a balanced risk, then you may be better off with a true balanced fund (maintaining a 50:50 ratio between equity and debt) or a pure large-cap fund (and not flexi-cap or mid-cap funds). The logic is simple: the more your time horizon, the more the risk you can take and the more time you will have to even out your losses.

[Read More: Best Balanced Fund to Invest in 2021]

-

Investment Objective: Don’t invest blindly, in greed or just because your agent, friend, relative or next-door neighbour tells you to invest. Investing is an individualistic exercise, and therefore you should follow a need-based approach.

Barry Ritholtz, an American author, newspaper columnist, and equity analyst, has aptly said, “When it comes to investing, there is no such thing as a one-size-fits-all portfolio.”

Whenever you are making a mutual fund investment, ask yourself what is your investment objective, the financial goals you wish to address, assess your risk profile, and the time in hand in to achieve the envisioned goals. This will help you make a sensible choice among the various categories and sub-categories of mutual funds.

Follow these principles while selecting a mutual fund and you will surely be able to build a winning mutual fund portfolio. It’s time you stop blindly investing in funds or investing in them based on star ratings which change quicker than the weather. Invest in fundamentally sound mutual funds and you will have a peaceful and successful investment journey.

Happy Investing!

This article first appeared on PersonalFN here

{kind=link}