The year 2024, as you may know, is an election year. At least 64 countries have their national elections scheduled in 2024, including India, the U.S. countries in Europe, Mexico, Russia, Indonesia, Thailand, North Korea, Sri Lanka, and several others. Nearly half of the world’s population, or approximately 4.2 billion people, would head to the polls.

The outcome of the general elections is set to shape government policies and have an impact on geopolitics, macroeconomic conditions, and society at large. We are going to experience interesting times ahead.

Speaking of India, the current dispensation, under the leadership of Prime Minister Shri Narendra Modi, has already sounded the poll bugle, saying the BJP alone will touch 370 seats in the 2024 Lok Sabha elections (higher than 303 seats won in the 2019 Lok Sabha elections).

Earlier this month (in February 2024), a White Paper on the Indian Economy was released by the Modi-led-NDA government, bringing to the fore how India moved up from the fragile five to the top five in the last 10 years, and deeply criticising the earlier two terms of the Congress-led-UPA regime for policy paralysis, significant corruption, high NPAs of banks, high fiscal deficit, and high retail inflation (particularly from 2009 to 2014).

Perhaps the White Paper was a rejoinder to sharp criticisms of the high unemployment rate, shutdown of small and medium enterprises, price rise, weak Indian Rupee (INR), slow GDP growth average than the UPA regime, high debt-to-GDP, widening income inequality, and loss of democratic values levelled by the opposition. The Indian National Congress, as a riposte to the White Paper of the Modi-led-NDA, released a Black Paper alleging how the decade-long rule under the present government devasted the economy, destroyed the agriculture sector, and aggravated unemployment.

Now, while there may be some concerns on governance as the opposition parties have pointed out, the fact remains that, in the two terms of the Modi-led-NDA government, several structural reforms have been implemented at a record pace:

- Make in India (to promote manufacturing in India)

- Production-Linked Incentive Scheme (for various sectors in the manufacturing space),

- Introduced numerous schemes for farmers

- Skill India (aimed at improving the skill set of youth and making them employable)

- Startup India (to promote the culture of entrepreneurship and innovation)

- Digital India (to make India a digitally empowered society)

- Unified Payment Interface or UPI (which made transacting online so much simpler),

- Simplified the indirect tax structure with the Goods & Services Tax or GST

- Focused on developing core infrastructure (roads, railways, ports, etc. to improve connectivity),

- Housing for the poor through the Pradhan Mantri Awas Yojana

- Financial inclusion through Jan Dhan Yojana

- The Direct Benefit Transfer scheme (aimed at transferring subsidies and other benefits directly to the beneficiaries’ bank account)

- Introduced social security schemes for the poor

- Enacted the Insolvency and Bankruptcy Code (giving powers to the lender to suspend the board, sue promoters and ensure speedy recovery)

- Set up bad banks (as part of a wider strategy to clean up the balance sheets of banks),

- RERA (a quasi-judicial body regulating builders and developers)

…and many more!

Today, India is perceived to be a “bright spot” in the global economy, a promising investment destination, and in the last decade has gone on to create wealth for its investors.

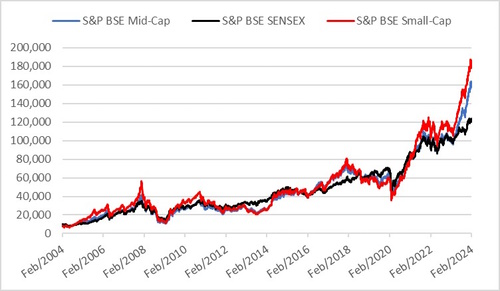

Ever since the Modi-led-NDA government has been in power, the bellwether, S&P BSE Sensex has clocked a pleasing CAGR return of +11.5% (as of February 21, 2024), while the S&P BSE Mid-cap, and S&P BSE Small-cap, during this period have fared relatively better clocking +17.6% CAGR and +19.1% CAGR, respectively (as of February 21, 2024). Translating these into absolute returns, the S&P BSE Sensex has gained +201.1%, the S&P BSE Mid-Cap +408.3%, and the S&P BSE Small-Cap +477.5% over the last 10 years.

Will The General Elections Have an Impact on The Indian Equity Markets?

The table below shows how Indian Indices have fared around general election time. Around three months before the general elections, markets usually have been watchful—like in 2004. Three months before the 2004 general election, the S&P BSE Sensex corrected -10.2% before the election results were announced. And when the election results showed the surprising defeat of the Vajpayee-led-NDA government (despite the ‘India Shining’ campaign), Indian equities corrected by a further -17.2% in the ensuing two trading sessions.

Thereafter, when UPA came to power under the able leadership of Dr Manmohan Singh, reassessing the new realities and policies decisions of the government in power, the bellwether index clocked a CAGR of nearly +16.9% from May 2004 to May 2014 (combined UPA I and UPA II).

Table 1: Performance of Indian Equity Markets Around General Elections

Data as of February 21, 2024

The table is for illustration purposes only.

Returns expressed are point-to-point.

*Please note, that this table represents past performance.

Past performance is not an indicator of future returns.The securities quoted are for illustration only and are not recommendatory.

Speak to your investment advisor for further assistance before investing.

(Source: ACE MF, data collated by PersonalFN Research)

In 2014 sensing the anti-incumbency owing to the corruption of the UPA regime, when the change in power was evident, and Shri Narendra was projected as the Prime Ministerial candidate of the BJP-led-NDA, markets did better both, pre and post elections.

Thus, note that, typically, whenever the election results are not on expected lines, markets do show knee-jerk reactions in the short term. But when the new government in power continues to frame sensible policies and reforms, equity markets fare well over the long term.

By and large, equity markets have reacted positively to the outcome of the general elections over longer periods. Despite many challenges faced (such as the COVID-19 pandemic, geopolitical tensions, supply chain disruption, inflation, high interest rates, financial market volatility, etc.) in the interim by the government, the graph below vindicates the power of equities to build wealth over the long term.

Graph 1: Performance of Key Equity Indices Over Two Decades

Data as of February 21, 2024

For the Indices graph, the base is taken as Rs 10,000

Past performance is not an indicator of future returns.

(Source: ACE MF, data collated by PersonalFN Research)

In this context, note the famous quote of legendary value investor, Benjamin Graham: “In the short run, the market is a voting machine but in the long run, it is a weighing machine.”

In the short run, sentiment and expectations drive stock prices. But over the long run, it is the fundamentals. As long as the fundamentals of the Indian economy remain strong, the corporate earnings trend is positive, and foreign portfolio investors along with domestic investors (retail, HNI, and institutional) perceive Indian markets to be promising, you don’t need to be worried about the outcome of the general elections.

Yes, of course, there are some key risks to watch out for in 2024, such as spillover of global developments, geopolitical tensions, supply chain disruptions, higher energy and food prices, and elevated borrowing costs, among others, which could have an impact on India’s GDP growth.

[Read: Key Investment Risks to Watch Out for in 2024]

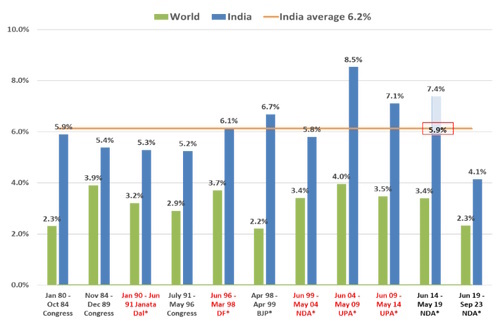

Graph 2: India’s Real GDP Growth Rate Across Governments Has Been 6.2% p.a.India may Grow >6%!

Note: The number in the red rectangle is from a changed data series starting Jan 2015. While a “superior” series, there is no comparable number to equate the “New” with the “Old”. Most economists deduct 0% to 1.5% from the “New” to equate to the “Old”; therefore, under Modi, the GDP has been at 5.9% at best matching the 5.6% under the BJP-led coalition government of Vajpayee, which resulted in the rout for the BJP at the time of the next election in 2004.* Please note that data used for World GDP for 2021 & 2022 is a median Estimate since World Bank data is not yet available and India GDP data is the government’s third advance estimate released at the end of November 2023.

(Source: RBI and www.parliamentofindia.nic.in; data as of September 2023)

Having said that, as long as India’s GDP grows at around 6.0%, it would be decent enough to generate wealth. The graph above reveals that India’s GDP growth over the last 43+ years has averaged 6.2%. In fact, in coalition governments backed by innovative thinking and all allies, GDP growth has been better.

The nation and its equity markets have created wealth. All that the government must do is continue with its reform measures, spend money on building robust infrastructure, attract sizeable fresh investments, create jobs, and ensure that the overall policy environment remains conducive to growth.

You see, not every election brings a change in the government or its policies (particularly when there isn’t any sign of anti-incumbency), but you can surely change the way you approach investments in an election year and not merely speculate.

Temperatures may rise this summer amidst the 2024 election rallies; however, you stay cool and approach your equities sensibly.

How to Approach Equity Investments Now?

For the equity markets, corporate earnings continue to play a vital role. Thankfully, the earnings trend in the last few years has been encouraging and justifies the premium that India’s equity markets command relative to its global peers.

That being said, it would be unwise to get carried away by irrational exuberance and unrealistic earnings estimates.

Near the lifetime high of the Indian equity market, tread cautiously rather than going gung ho. Particularly avoid skewing your portfolio small and mid cap segments of the market, which have run up quite a lot and the margin of safety seems to have narrowed.

[Read: Can Small Cap Funds Deliver Big Returns Going Forward]

Diversify your portfolio suitably by paying attention to asset allocation best suited for you.

Keep in mind that for every level of return you seek, there is risk. Hence, manage the risk by following a sensible asset allocation.

Broadly, when approaching equity mutual funds, it would be wise to follow a ‘Core & Satellite’ strategy – which is followed by some of the most successful equity investors around the world.

It would be worthwhile holding a Large Cap Fund, a Flexi-cap Fund, and a Value Fund as part of your Core holdings (around 65-70% of your equity portfolio) with a time horizon of around 3 to 5 years. Doing so shall offer you portfolio stability.

The Satellite holdings (around 30-35% of your equity portfolio), on the other hand, may comprise a Mid Cap Fund and a Small Cap Fund provided you have a long time horizon of around 7 to 8 years and the stomach for high-risk. This would help push up the overall returns when the market conditions favour these market cap segments.

As regards whether to take the lump sum or the SIP route, given that the markets are at a lifetime high and there may be evident ups and downs in the equity market due to several risk factors in play, even if you have the surplus funds to invest, it would be prudent to stagger your investments. Meaning, invest it in parts or piecemeal manner keeping an eye on the opportunities available.

Even better is taking the SIP route, which shall help mitigate or reduce the ups and downs of the Indian equity markets, make timing the market irrelevant, instil investment discipline, and potentially compound your wealth in the long run. SIPs, particularly when planning to achieve certain long-term financial goals, are a worthwhile mode of investing.

Finally, be a thoughtful investor and set your return expectations right. The overall returns on the equity portfolio you clock would hinge on your asset allocation.

Happy Investing!

This article first appeared on PersonalFN here

{kind=link}