Individuals looking to invest their hard-earned money for long-term capital appreciation have the option to choose between Portfolio Management Services (PMS) and Mutual Funds.

PMS and mutual funds are broadly similar as both invest investor’s corpus in various securities such as equity and debt. Both have a designated fund manager to oversee the investments and to ensure that the portfolio aligns with the investment objective of the scheme.

Yet, PMS and mutual funds differ in more ways than one.

This article explores the many ways in which mutual funds outscore PMS.

What are PMS?

As the name suggests, a Portfolio Management Service or PMS is a personalised investment service in which a qualified portfolio manager manages the investment portfolio of individuals on their behalf.

A PMS can be discretionary or non-discretionary. In the case of discretionary PMS, the portfolio manager makes the investment decisions and has the power of attorney (PoA) to buy and sell shares on behalf of the investor.

Meanwhile, in the case of non-discretionary PMS, the portfolio manager executes the trades only after getting approval from the individual investor for each suggestion.

PMS offers tailor-made investment strategies depending on the investor’s financial goals, risk profile, and personal preferences. In the case of PMS, investors own the securities in their names.

What are Mutual Funds?

A mutual fund scheme, as the name suggests, is a fund that pools money from multiple investors and invests the collected corpus in various securities, such as stocks and fixed-income instruments.

The investments are made in accordance with the investment objectives as disclosed in the scheme offer document. For instance, an equity mutual fund scheme will invest predominantly in stocks of listed Indian companies, while a debt mutual fund will invest a significant portion of its assets in debt and money market instruments.

Each mutual fund scheme is managed by a fund manager/s who analyses the underlying assets on a day-to-day basis and then decides when to buy and sell investments.

In the case of mutual funds, investors can own only the units of the scheme/s they invest in.

Like PMS, mutual funds too have the potential to generate high returns. As we can see in the table below, various equity mutual fund schemes generated high returns across different time frames. Amid a broad-based market rally in recent years which was mainly lead by small-cap and mid-cap stocks, Small Cap Funds turned out to be winners.

How have Mutual Funds performed compared to PMS?

It is noteworthy that unlike mutual funds, PMS do not have a clear definition and classification of schemes or market cap limit for investments in various categories. Therefore, there may be a stark difference in strategies adopted by fund managers for the selection of securities for the portfolio even if they focus on the same market cap range.

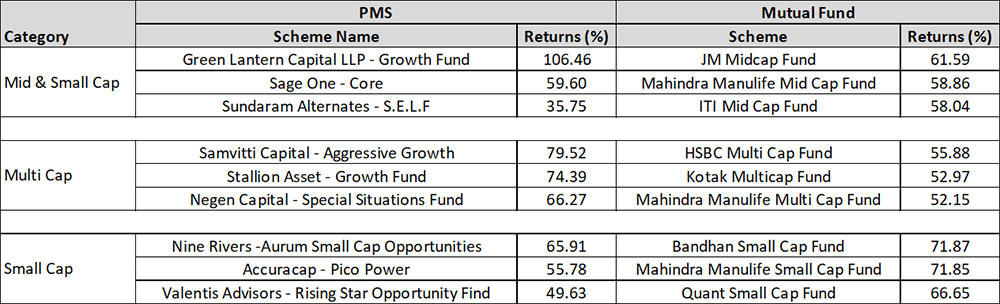

PMS vs Mutual Funds: 1-year returns

Data as of January 31, 2024

Past performance is not an indicator for future returns

Due to unavailability of rolling returns for PMS, point-to-point returns considered. Returns are Absolute in %. Note: Rolling returns are better tool for evaluation of scheme performance

(Source: www.pmsaifworld.com, ACE MF, data collated by PersonalFN)

This trend is clearly visible in the performance of PMS where one may find sharp divergence in the returns generated by schemes within a certain category. As a result, investors need to have a clear understanding of the asset allocation strategy of the PMS they consider investing in and the kind of risk the fund manager is taking. For instance, on a 1-year return basis, one of the top performing mid-cap oriented PMS schemes generated approximately 106% absolute returns, while the next top-performing scheme achieved substantially lower returns at about 60%, absolute. Conversely, the top performers in the comparable mid-cap mutual fund category exhibited similar performance. This highlights that mutual funds adhere to a well-defined investment mandate that fund managers are expected to follow, unlike PMS, where fund managers may easily deviate from the mandate in pursuit of extraordinary gains.

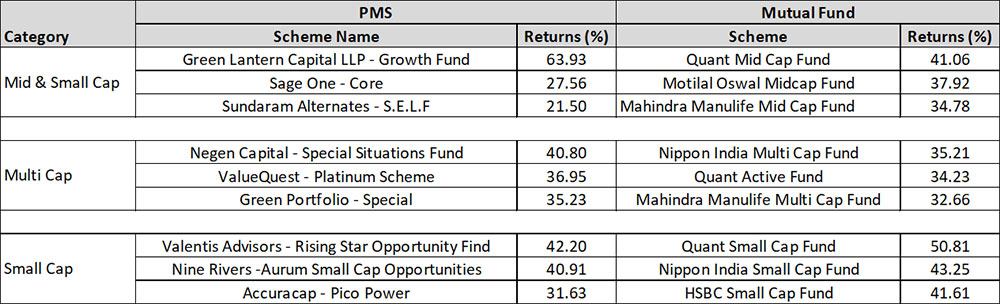

PMS vs Mutual Funds: 3-year returns

Data as of January 31, 2024

Past performance is not an indicator for future returns

Due to unavailability of rolling returns for PMS, point-to-point returns considered. Returns are CAGR in %. Note: Rolling returns are better tool for evaluation of scheme performance

(Source: www.pmsaifworld.com, ACE MF, data collated by PersonalFN)

Over the course of the 3-year period, the mutual funds schemes within the Mid Cap Fund and Small Cap Fund categories fared better compared to PMS. However, it is worth noting that certain PMS with a focus on the Multi Cap strategy exhibited strong performance compared to the top-performing Multi Cap Mutual Funds.

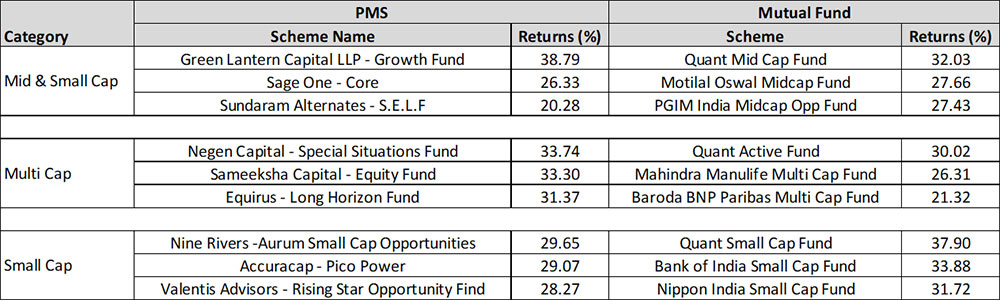

PMS vs Mutual Funds: 5-year returns

Data as of January 31, 2024

Past performance is not an indicator for future returns

Due to unavailability of rolling returns for PMS, point-to-point returns considered. Returns are CAGR in %. Note: Rolling returns are better tool for evaluation of scheme performance

(Source: www.pmsaifworld.com, ACE MF, data collated by PersonalFN)

In the last 5 years, the remarkable upswing in the broader market following the post-COVID crash has led to impressive returns for both PMS and Mutual Fund schemes that primarily invest in mid-cap and small-cap stocks, as well as those following a multi-cap strategy.

However, the substantial difference in the strategies adopted by the fund managers of PMS and the resulting margin gap in returns generated by PMSs can complicate the process of comparing two or more PMS schemes.

On the other hand, since mutual funds within a category invest in a pre-defined investment universe, and also have a uniformity in benchmark, the evaluation of schemes belonging to a particular category is relatively easier.

While certain PMS schemes may outperform similar mutual funds, not all of them can be as dependable and predictive when compared to mutual funds with explicit mandates and guidelines on their management approach. So, it is important to choose the approach that aligns with your investment goals and assess its suitability for your risk profile.

Why mutual funds can be a better option for investors?

Here are the different ways in which mutual funds are better than PMS…

1) Portfolio size:

SEBI has prescribed a minimum ticket size (minimum investment) of Rs 50 lakh for PMS. This means PMS are suitable only for high net-worth individuals.

On the other hand, an individual can start investing in mutual funds with an amount as low as Rs 500 (depending on the type of scheme you choose), making it suitable for every type of investor.

[Read: Begin with Minimum Investment in Mutual Funds And Watch Your Money Grow]

2) Transparency:

A PMS is required to disclose scheme-related data only to its client. Therefore, it is not accessible to the general public, making it difficult for individuals to compare and select the right PMS to invest in.

In the case of mutual funds, all the data related to performance, risk ratio, expense ratio, portfolio, NAV, etc., is publicly available. Thus, investors have a clear understanding of the risk-reward matrix, making it easier to select the one suitable for their needs.

3) Taxation:

In the case of PMS, since investors own the securities under their name, the investors also bear the charges (such as brokerages) and tax implications arising out of the transaction (such as securities transaction tax, capital gains tax, etc.).

On the contrary, the transactions carried out by a mutual fund scheme are not treated as your own. Thus, all the ‘buy’ and ‘sell’ transactions done by the fund manager of a mutual fund do not affect an individual’s tax liability. Investors are only liable to pay tax on the capital gains earned on the redemption of units.

[Read: 3-Tiered Taxation of Mutual Funds: Here’s All You Need to Know]

4) Regulation:

The regulations for PMS are not very stringent as they are not required to disclose information publicly. It is possible that flexibility in terms of regulatory disclosure can result in anomalies such as window dressing of returns. Notably, there have been reports of sharp deviations in returns of model portfolios of PMS and actual returns of investors, as well as reports of PMS not using appropriate benchmark for disclosing the performance of the scheme.

Meanwhile, mutual funds are subject to strict regulations and timely scrutiny by SEBI, which results in better accountability and ensures that they prioritise investors’ interests over chasing returns.

5) Diversification:

PMS usually cater to savvy investors who prefer high risk – high return investment strategy. These schemes generally have personalised asset allocation, having no more than 20-30 stocks in their portfolio, keeping in mind each individual’s risk appetite and investment goals. However, this can result in concentration risk if the bets do not pay off as planned.

In the case of mutual funds, they generally invest in at least 40 to 50 stocks. Moreover, they cap the individual stock weights at 10% and sector weights at 25%. This strategy enables to limit the downside risk during bearish market conditions, thereby earning optimal risk-adjusted returns.

[Read: Asset Allocation: The Cornerstone of Successful Investing]

Thus, most investors will be better off investing in mutual funds. There are numerous types of mutual funds available in the market that can help investors create a suitable portfolio that aligns with their needs.

Watch this video to know about the 5 best mutual fund types for long-term investment:

This article first appeared on PersonalFN here

{kind=link}