A mutual fund portfolio consists of various stocks, bonds, and other asset classes. SEBI has clearly defined the types of assets/sub-assets each category and sub-category of a mutual fund can invest in. For instance, Large-cap Funds are mandated to invest at least 80% of their assets in equities of large-sized companies, i.e., top 100 stocks in terms of market capitalisation.

For Mid-cap and Small-cap Funds, the universe of stocks is relatively larger. Mid-cap Funds invest in companies ranking 101st to 250th while Small-cap Funds invest in companies ranking 251st onwards. However, there are only a limited set of stocks that can be considered as worthy of investment.

Thus, mutual fund schemes within a category hold more or less the same set of stocks in their portfolio. So, when an investor invests in two or more schemes within a category, it is likely that they have the same stocks in their portfolio. This results in mutual fund overlap.

Often investors add two or more schemes within a category with an aim to achieve diversification. But if the portfolio composition of the schemes is similar to a major extent, i.e., the mutual fund overlap is high, it defeats the purpose of diversification which is mitigating the risk by investing in dissimilar assets, sub-asset classes.

On the contrary, it can expose your portfolio to concentration risk leading to polarised returns as it will be skewed towards a few set of stocks, sectors, market cap, or investment styles. It also increases the burden of monitoring and makes portfolio review/rebalancing difficult.

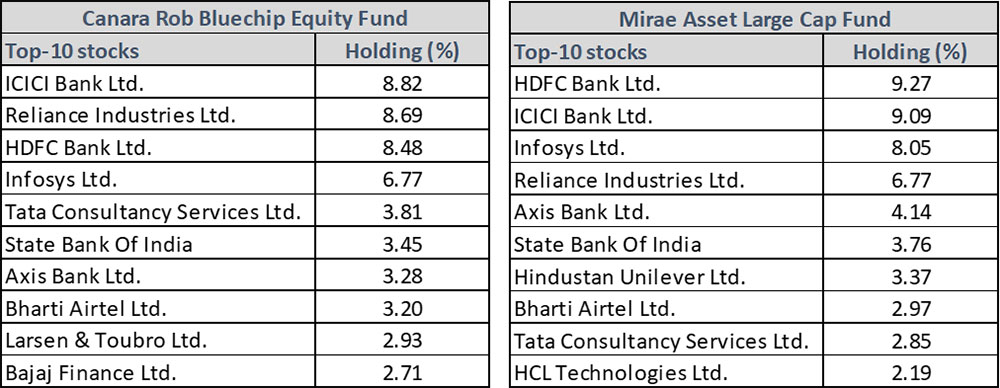

Consider this, let’s assume that you are looking to invest in two Large-cap Funds, viz. Mirae Asset Large Cap Fund and Canara Robeco Bluechip Fund assuming that it will help you in diversifying your portfolio. However, if you analyse the portfolio holdings, you will realise that the two schemes have 29 common stocks (or 45-65% of the portfolio). The top-10 holdings of the schemes have 8 common stocks. Evidently, the two schemes have high portfolio overlap and therefore, adding both schemes in your portfolio will not offer substantial diversification.

Table: Adding schemes within the same category can lead to mutual fund portfolio overlap

Data as of May 31, 2022

(Source: ACE MF)

You can add more schemes within the same category only if they follow distinct investment styles or strategies. It also makes sense to invest in two or more schemes within a category if you have a large investible corpus and are thus wary of putting in all the money in one scheme/fund house. However, if you are a small investor, one scheme within each category would suffice to meet your diversification needs.

If you are holding too many schemes and are worried about portfolio overlap, here is how you can optimise your portfolio:

1) Aim for optimal diversification

Optimal diversification is necessary to mitigate the risk to the portfolio. To achieve optimal diversification, align your investments to your goals, risk appetite, and investment horizon, and then invest accordingly. Large-cap Funds are suitable if you have a moderate risk appetite and are looking to earn steady returns over a period. If you are willing to take a higher risk, consider adding Flexi-cap Funds, Large & Midcap Funds, and Mid-cap Funds. Avoid adding more than 1-2 schemes within the same category. This will help you to monitor the progress of the schemes in achieving your goals.

Do note that most individual investors do not require more than 5-10 mutual fund schemes, depending on the size of the portfolio. These would include schemes across equity mutual funds, debt mutual funds, hybrid mutual funds, and ELSS. If you are investing a modest amount every month, even 3-4 schemes may suffice to create a well-diversified portfolio.

[Read: The 5 Best SIPs to Start in 2022 – Top Performing Mutual Fund SIPs in 2022]

2) Eliminate consistent underperformers

If you have added multiple schemes within the same category, eliminate the one that has consistently underperformed its benchmark and the category average. The proceeds from the scheme can be invested in the scheme/s that are performing well. However, do not take the decision solely on short-term underperformers. The fund should be able to actively participate during recovery and bull phases while simultaneously being able to protect the downside risk better during bear phases.

To check whether the scheme is a consistent performer, analyse it on various risk-reward parameters such as, performance across market phases, Sharpe Ratio, Sortino Ratio, Standard Deviation, etc. While determining the consistency of a scheme’s performance, bear in mind the importance of its quantitative parameters, such as the portfolio characteristics of the scheme, the efficiency of the fund house, and the quality of the fund management team.

3) Avoid adding new fund offers (NFOs)

Investors often add newly launched schemes hoping that it will help them in diversifying their portfolio. However, if the NFO has a similar investment objective and is benchmarked against the same index, there are high chances that the portfolio will overlap with your existing mutual fund schemes. In addition, when you invest in an NFO, there is no reliable track record of the fund’s performance, portfolio quality, risk-return profile, etc., that will help you determine if it is a worthy scheme for your portfolio. This makes NFOs a risky proposition for investors, and you would be better off cutting down on NFOs.

If you are willing to take the risk, you may consider adding NFOs to your portfolio, provided they offer a unique proposition that is currently not available in the market and if it aligns with your financial goals.

[Read: How to Reduce the Number of Schemes in Your Mutual Fund Portfolio]

To conclude

Adding too many schemes to your portfolio can lead to mutual fund overlap. It also makes the crucial task of monitoring your portfolio a challenging exercise. You may even end up with a portfolio consisting of underperforming schemes or an unsuitable asset mix.

Therefore, ensure that you include only those schemes in your mutual fund portfolio that align with your financial goals and personalised asset allocation plan.

Review your portfolio periodically (at least once a year) to see if the mutual fund overlap is not too high and is well placed to achieve your goals. When you review the portfolio, check whether there is a need to weed out the underperforming schemes and replace them with a more suitable alternative. Also, check if there is a need to rebalance the portfolio so as to align it with your personal asset allocation plan.

This article first appeared on PersonalFN here

{kind=link}