The Interim Budget 2024 is a much-awaited event. Although a temporary budget — technically, a vote of account before the polls — most industries and individuals have high expectations. After all, it is Modi 2.0’s last budget before the upcoming Lok Sabha elections (to be held mostly in April and May 2024).

Usually, on the eve of the Union Budget, the Chief Economic Advisor (CEA), presents the Economic Survey, providing insights on the state of the economy and how the previous budget worked. However, this year, swerving from the usual practice, the CEA, Mr V. Anantha Nageswaran, has stated this year the government will not present the Economic Survey since it is an election year.

The Economic Survey will be presented only in July 2024 after the respective government is voted to power and the full budget is announced.

That said, the review on the Indian Economy released by the Department of Economic Affairs has some takeaways…

According to the review, the Indian economy is expected to be a USD 5 trillion economy in the next 3 years (from the current USD 3.42 trillion) and could reach USD 30 trillion by 2030.

With reforms rolled out, the government believes this goal is achievable, and comes on the back of robust domestic that has helped the economy clock 7%+ growth in the last three years. The supply side measures have also been strengthened investment in infrastructure — physical and digital — and measures that aim to boost manufacturing. These have combined to provide an impetus to economic activity in the country, cites the Review on the Indian Economy.

The National Statistical Organisation (NSO) and the Reserve Bank of India (RBI) have projected to grow at 7.3% and 7.0%, respectively, in FY24. In FY25, the government is of the view that real GDP growth would be closer to 7.0%. Plus, there is considerable scope for the growth rate to rise well above 7.0%, observes the Economic Review of the government.

However, as per the review, there are certain challenges or risks that confront the Indian economy:

- India’s growth will also show the spillover effects of global developments. The geopolitical tensions/conflicts, increased geoeconomic fragmentation, repercussions on global trade, and inflation, would weigh on economic growth.

- Global energy prices have escalated due to the Russia-Ukraine war, tensions in the Middle East and policy actions pursued by individual countries.

- The advent of Artificial Intelligence (AI), could pose a challenge for governments around the world to create jobs. As per the International Monetary Fund, 40% of global employment is exposed to AI, with the benefits of complementarity operating beside the risks of displacement.

- Domestically, ensuring the availability of a talented and appropriately skilled workforce to the industry, age-appropriate learning outcomes in schools at all levels and a healthy and fit population will be crucial. These are important policy priorities in the coming years. A healthy, educated, and skilled population augments the economically productive workforce.

Now while these issues or challenges are very much on the government’s radar and policy thrust, 7% GDP growth looks rather ambitious given the headwinds in play.

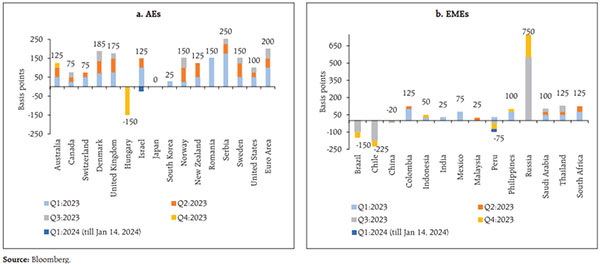

Policy interest rates in major economies such as the U.S., U.K., France, Germany, Russia, Brazil, China and many others, are still high after the rate hikes.

Graph 1: Changes in Policy Rates

(Source: RBI Bulletin, January 2024)

While the central banks would want to reduce interest rates to support growth, much depends on the inflation trajectory. December 2023 saw a marginal uptick in inflation in major economies such as the US Euro area, as well as India. The RBI in its December 2023 bi-monthly monetary policy statement, envisages risk to the inflation emanating from:

– Food prices

– Volatility in Crude oil

– Financial markets

– And uncertain international environment

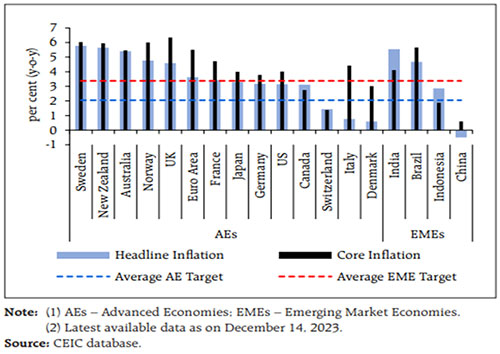

Now, while much of the disinflation has happened, the headline CPI inflation continues to remain above the target of most central banks in Advanced Economies and Emerging Market Economies (EMEs).

Graph 2: Headline Inflation is still way above average target in many economies

(Source: RBI Financial Stability Report, December 2023)

According to the Word Bank, while the headline CPI is expected to moderate in 2024-25 with core inflation and commodity prices declining, it is expected to remain above the pre-pandemic average beyond 2024.

Mr Ajay Banga, the World Bank President, has expressed that high interest rates would stay for long and would complicate investments for companies across the word. In other words, it could have a bearing on the economic growth. He told a news conference in October 2023 that wars are extremely challenging for central banks that are trying to find a way to steer their economies towards a soft landing.

The International Monetary Fund (IMF) too, has recently stated that renewed geopolitical tensions in the Middle East could cause supply disruptions (amidst increased shipping costs) and the situation remains volatile. The core inflation could prove more persistent.

In such a scenario, the IMF cautions that central banks must avoid prematurely easing rates – even though the market seems excessively optimistic about rate cuts. According to the IMF, reducing policy interest rates prematurely would undo many hard-earned credibility gains and lead to a rebound in inflation.

In an election year, where usually government spends and injects money into the economy (to win over voters), it is unsurprising to witness demand-pull inflation while it boosts economic activity.

In the upcoming 2024 elections while potential fiscal slippage due to populist moves is a concern, at least India is by and large expected to walk on the path of fiscal consolidation.

The IMF observes, that emerging markets (like India) have been very resilient, with stronger-than-expected growth and stable external balances, partly due to improved monetary and fiscal frameworks.

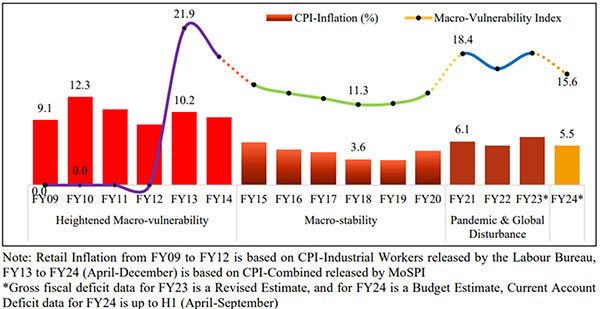

Graph 3: Macro-vulnerability Index# and Retail Inflation

#Macro-vulnerability index is calculated by combining a country’s fiscal deficit, current account deficit, and retail inflation. A lower number indicates a lower vulnerability.

(Source: Indian Economy: A Review, January 2024)

As per the Indian Economy: A Review, the fiscal balance of the general government and the country’s external balance improved, progressively reducing macro-vulnerabilities and generating buffers for turbulent times ahead. Having said that, due to global disturbances or geopolitical tensions, the reading of the Macro-vulnerability Index is still high.

The IMF in its latest World Economic Outlook release in January 2024 has projected global growth at 3.1% in 2024 and 3.2% in 2025, with the 2024 forecast 0.2% higher than that in the October 2023 World Economic Outlook on account of greater-than-expected resilience in the U.S. and several large emerging market and developing economies, as well as fiscal support in China.

India is perceived as a bright spot by the IMF, projected to grow at 6.7% in FY24 (40 basis points higher than what was projected in October 2023) and expected to remain strong at 6.5% in both 2024 (i.e. FY25) and 2025 (i.e. FY26), reflecting resilience in domestic demand. These projections make India the fastest-growing major economy.

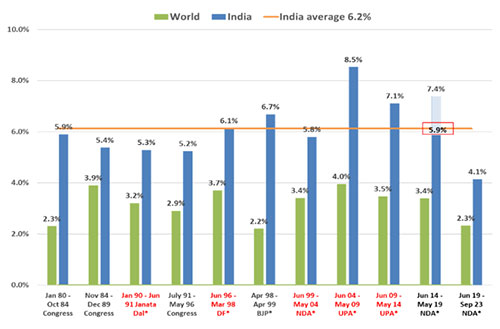

Graph 4: India’s GDP real growth rate across governments has been 6.2% p.a.India may grow >6%!

Note: The number in the red rectangle is from a changed data series starting Jan 2015. While a “superior” series, there is no comparable number to equate the “New” with the “Old”. Most economists deduct 0% to 1.5% from the “New” to equate to the “Old”; therefore, under Modi, the GDP has been at 5.9% at best matching the 5.6% under the BJP-led coalition government of Vajpayee, which resulted in the rout for the BJP at the time of the next election in 2004.* Please note that data used for World GDP for 2021 & 2022 is a median Estimate since World Bank data is not yet available and India GDP data is the government’s third advance estimate released at the end of November 2023.

(Source: RBI and www.parliamentofindia.nic.in; data as of September 2023)

The graph above reveals that India’s GDP growth over the last 40+ years has averaged 6.2%. In our view, even if India’s GDP grows around the average GDP growth rate of around 6.0%, it would be decent enough to generate wealth. However, the government must continue with its reform measures, spend money on building robust infrastructure, attract sizeable fresh investments, create jobs, and ensure that the overall policy environment remains conducive to growth.

How to Approach Investments in 2024?

The Indian equity markets are expected to remain volatile owing to a variety of factors in play. Ahead of the budget and general elections, we have already witnessed the volatility. Markets are looking for certain decisive aspects to chart their trajectory. Indian equities are anyways trading at a premium compared to their global peers.

It is important to tread cautiously rather than going gung ho. Avoid going overweight or skewing your investment portfolio, particularly to mid-and-small cap mutual fund schemes. In an overheated market, consider investing in largecaps instead. Large Cap Funds that follow robust investment processes and systems hold the potential to generate meaningful alpha over the benchmark.

[Read: 4 Best Large Cap Mutual Funds for 2024]

Diversify your portfolio suitably and sensibly.

It would be ideal to follow a Core and Satellite approach when investing in equity mutual funds. It is a strategy followed by some of the most successful equity investors around the world.

Your ‘Core’ holdings of the equity portfolio should comprise around 65-70% of your equity mutual fund portfolio and consist of some of the best Large-cap Funds, a Flexi-cap Fund, and a Value Fund/Contra Fund. These shall offer more stability to your portfolio.

The ‘Satellite’ holdings of the portfolio, on the other hand, can be around 30-35%, comprising a Mid-cap Fund, a Large & Mid-cap Fund, and an Aggressive Hybrid Fund. These shall help push up the returns in favourable market conditions.

When you construct a Core & Satellite portfolio of equity mutual funds, make sure not to end up over-diversifying the portfolio. Select not more than 7 to 8 best equity schemes.

Also, it would be best to ensure that no more than two equity mutual fund schemes belonging to the same fund house are included in the portfolio.

Further, no more than two schemes in the portfolio should be managed by the same fund manager, all the schemes should have a strong track record of at least five years, ensure they have outperformed over at least three market cycles, are among the top performers in their respective categories, and are abiding by the stated objectives, indicated asset allocation, and investment style.

By wisely structuring and timely reviewing the Core and Satellite holdings, you would be able to add stability to the portfolio and prove to be a wealth multiplier in the long run. The Core & Satellite investment strategy may work for you in 2024 and beyond. When approaching equity-oriented funds with the Core and Satellite strategy, make sure to have an investment time horizon of at least 5 years.

For tactical asset allocation to equity, debt, and gold, a Multi-Asset Fund would also be a meaningful choice now at a market high.

It would be wise to stagger your investments at this juncture, or even better, take the SIP route. The inherent rupee-cost averaging feature of SIPs shall help mitigate the volatility, make timing the market irrelevant, and help remain focused.

When investing in debt, you may consider investing in some of the best Banking & PSU Debt Funds (with a 2 to 3 years investment horizon) or Dynamic Bond Funds (with a 3 to 5 years investment horizon).

If your investment time horizon is shorter, say a couple of months to a year, Liquid Funds would be appropriate and an alternative to keeping money in a savings bank account. A pure liquid fund that invests in T-bills, government and quasi-government securities with maturity of up to 91 days, can also help you plan your contingency needs. For this purpose, it makes sense to hold 12 to 18 months of regular monthly expenses (including EMIs on loan) in a Liquid Fund. Alternatively, you may also consider parking money into a bank fixed deposit.

Given the uncertainty looming, it also makes sense to strategically allocate around 10% to 15% of your entire investment portfolio towards gold and hold with a long-term view (of over 5 to 10 years) by assuming moderately high risk. Gold will continue to play its role as a portfolio diversifier, a safe haven, and a store of value during macroeconomic and geopolitical uncertainties.

In fact, recognising the risks in play (while countries are hoping to clock better economic growth), central banks are buying gold as part of their risk management.

You see, unlike financial assets, gold is a real asset — meaning gold does not carry credit or counterparty risk. Even a stronger U.S. Dollar hasn’t deterred investors from buying gold, since it is perceived to be a strategic long-term asset class. So, approach gold the smart way –in the form of Gold ETFs, Gold Savings Funds, and/or Sovereign Gold Bonds, as opposed to buying physical gold (unless you are buying for a family wedding).

In general, when investing, be mindful of the risk involved — and do not invest blindly going by just the past returns, which is in no way indicative of the future returns. Keep your return expectations rational and keep in mind that for every level of return you seek, there is high risk.

Be a thoughtful investor.

Happy Investing!

This article first appeared on PersonalFN here

{kind=link}