All eyes were on India’s GDP growth data for Q3FY21 with many market participants expecting an expansion. The data is finally out. The Indian economy, after contracting for two consecutive quarters, has reported a positive growth rate of 0.4% in Q3FY21.

Which sectors attributed to the rise after the slump?

Agriculture remained steady reporting a 3.9% growth year-on-year (Y-o-Y). Financial, Real Estate, and other Professional Services made a strong comeback with 6.6% growth Y-o-Y. Similarly, Electricity, Gas, Water Supply, and other Utility Services (7.3% growth Y-o-Y) and Construction (6.2% growth Y-o-Y) helped the Indian economy come out of recession. The Manufacturing sector, which saw a noticeable impact during the pandemic has also sprung up and grown 1.6% Y-o-Y.

However, Mining and Quarrying continued to contract -5.9% Y-o-Y, although some improvement was noticed since the previous two quarters. Trade, Hotels, Transport, Communications, and Services related to broadcasting, amidst the COVID-19 pandemic, continued to contract (-7.7% growth Y-o-Y) but reported a better reading compared to the previous two quarters.

Speaking of the expenditures, it reveals that the government has loosened its purse strings to support the economy and fight the COVID-19 pandemic. The government’s final expenditure contracted far lesser at -1.1% in Q3FY21, compared to -24.0% in Q2FY21.

Thus, the Private Final Consumption Expenditure (i.e. the expenditure incurred by the resident households and Non-Profit Institutions Serving Households (NPISH) on the final consumption of goods and services, whether made within or outside the economic territory) also contracted to -2.3% in Q3FY21 vis-a-vis -6.8% in the previous quarter. The Gross Fixed Capital Formation (GFCF), which throws light on the net investments and the capex cycle, got a new lease of life as it grew 2.5% in Q3FY21 versus -6.8% in the previous quarter.

Overall, the government’s final spending cooled off a bit to make up 9.8% of the current GDP versus 10% in Q2FY21 and Q3FY20, respectively. Consumer spending has improved quarter-on-quarter (Q-o-Q) and now forms 58.6% of the GDP against 54.3% in Q2FY21. However, on a Y-o-Y basis, the consumption demand is still weak: in Q3FY20, private consumption constituted 60.2% of GDP.

What does the latest GDP reading mean for your mutual fund investments?

A ‘V-shaped’ economic recovery forecast made in the Economic Survey 2020-21 is supported by the latest GDP reading. However, for the financial year 2020-21 as a whole, the National Statistical Office has projected India to contract at -8.0% as against -7.7% forecasted earlier.

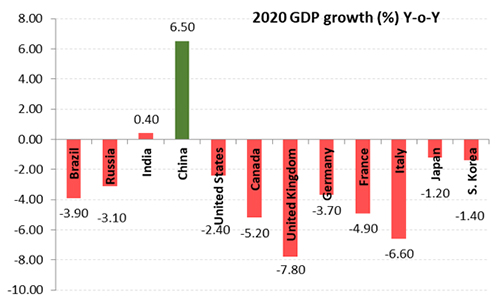

Graph 1: India’s GDP growth rate versus BRIC and developed nations

GDP at constant prices 2011-12 for IndiaIn the graph, the GDP data for Brazil and Canada is as of September 2020 quarter.

(Source: www.tradingeconomics.com)

In my view, although we are out of recession technically speaking, the latest GDP reading does not look very assuring to validate that in Q4FY21 as well the Indian economy would grow. Currently, not all components of India’s GDP are demonstrating growth. It is likely that the reading for the ensuing few quarters could slip back into a contraction, which means we could see a sort of ‘W-shaped’ recovery, where we would dip again before moving up.

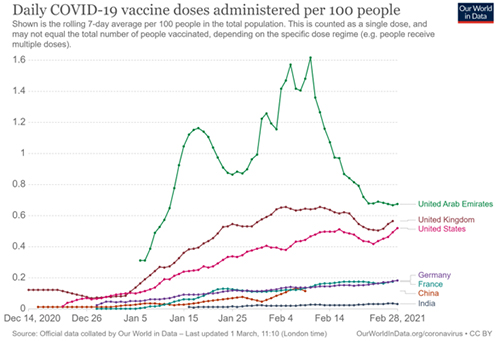

Graph 2: India at the start of a second COVID-19 wave, and lagging on the vaccination drive

Data from December 14, 2020, to February 28, 2021

(Source:: https://ourworldindata.org)

India, after bending the COVID-19 curve, is at the precipice of witnessing the beginning of the second wave. States like Maharashtra, Kerala, Karnataka, Andhra Pradesh, Telangana, Tamil Nadu, West Bengal, Punjab, and Gujarat are seeing a rise in cases –contributing to almost 86% of the new cases–due to easing of lockdown restrictions and citizens not adhering to the necessary COVID-19 protocols (such as wearing mask correcting, following hand hygiene, and maintain safe social distancing). While we are officially in phase-II of the vaccination programme (which focuses on people above 60 and also those above 45 with comorbidities), India is still lagging behind many other nations when it comes to the vaccination drive. So far only around 1.37 crore doses of the vaccine are administered in India …and that’s just the first dose of the two doses required.

It is important to note that the virus is mutating and we are seeing new strains, which were unheard of when the current vaccines were developed. If India reports a remarkable rise in cases, and certain restrictions are reinstated to curb the spread of the deadly pathogen, it may weigh on India’s GDP.

The Indian equity market, although is reading the COVID-19 data carefully, for now, is finding solace in the fact that the ‘helicopter money’ (powered by the easy monetary policy actions by the way of near-zero or sub-zero interest rates and bond-buying programmes in the developed markets) will continue. The U.S. Federal Reserve in the last meeting decided to keep interest rates near zero levels and keep buying bonds on the backdrop of slower economic recovery, job creation, and since inflation in the U.S. is still way below the long-range target (of 2.00%).

Bond yields in the U.S. have of course risen, anticipating a stronger economic recovery and the possibility of inflation with it. But with that, the potential positive impact on the Indian equity market, too, is not ruled out by market participants–they are taking calculated risks and investing in equities; wherein India continues to be an attractive investment destination.

Foreign Portfolio Investors (FPIs) in the first two months of the calendar year 2021 have been net buyers to the tune of Rs 34,259 crore and the tally for FY21 has been massive Rs 2,55,083 crore by February 2021-highest ever in any financial year.

The government to address growth concerns amidst the pandemic has widened the fiscal deficit target for the current year to 9.5% of GDP, while for the next fiscal year, i.e. 2021-22 estimated it to be 6.8% of the GDP. That said, it is important that the government spends the resources available judiciously for sustainable economic recovery. The 10-year G-sec yield in India has also ascended over 6% (despite RBI’s assurance that it would provide ample liquidity and ensure a smooth government-borrowing programme), but that has not dimmed the excitement in equity as an asset class for wealth creation. On Dalal Street, the bulls are treading positively and celebrating the announcements made in the Union Budget 2021-22.

One key risk that could derail the process of economic recovery and upset the equity market is the bad loan problem. The RBI’s Financial Stability Report (FSR) has indicated a potential surge in the Non-Performing Assets (NPAs) of the banking sector. The FSR points out NPAs could rise to 13.5% by September 2021 from 7.5% in September 2020. And under a severe stress scenario, the bad loans could mount to 14.8%.

You may be aware, as of August 31, 2020, nearly 40% of the bank loans were under moratorium with as many as 78% MSME and individual retail borrowers availed the moratorium facility.

Another obstacle in India’s growth prospects may be inflation. If the Consumer Price Index (CPI) inflation rises beyond 6%, the RBI may find it difficult to continue with its accommodative stance. Under such a scenario, higher government borrowings and higher deficit may hurt India’s fiscal position as well. Several commodity prices are already on the rise; especially, industrial metals have witnessed an unprecedented rally, not only in India but across the globe.

Copper has gone up 15% in February alone, so has Steel; whereas Brent Crude oil has shot up 17%, over the last one month. The increase in prices of industrial metals would increase prices of goods that include some of these metals in the production of finished goods, viz. Vehicles (two-wheelers and four-wheelers) Air-Conditioners, etc. Similarly, the rise in fuel could result in transport and food prices getting dearer. On the aforesaid backdrop, I do not see India’s GPD moving up linearly. We may witness a sort of ‘W-shaped’ recovery, where we would dip again before moving up.

How to approach equity-oriented mutual funds now?

First, note that the current rally is highly liquidity-driven, based on ‘helicopter money’.

Secondly, the valuations in the Indian equity markets are expensive (trail P/E is around 35x) and the margin of safety across the market capitalisations appears to have narrowed. While the Union Budget 2021-22 announcements have set the bulls raging, the chances of intermediate corrections and high volatility cannot be ruled out.

Corporate earnings of many Indian companies have, of course, remarkably improved after the unlocking from COVID-19 national lockdown and easing restrictions. But we need to assess how well the recent earning momentum sustains in the ensuing quarters. It is important that India Inc. earnings consistently improve, wherein a positive trend is visible. So, do not get swayed by unrealistic corporates earnings estimates.

Take note of the famous quote, “Be fearful when others are greedy and greedy when others are fearful” , by the legendary investor, Mr Warren Buffett. And set realistic post-tax return expectations from your investment portfolio.

Recently, SEBI Chief, Mr Ajay Tyagi highlighted the glaring disconnect between the economic growth and the mood of equity investors while addressing a webinar organised by SEBI at the NISM Research Conference on Behaviour of Securities Markets. According to him, nearly 1 crore fresh equity accounts were opened in the first 10 months of FY21, which took the total number of accounts to 5 crore.

It’s noteworthy that the industry took 28 months to reach the tally of 4 crore from 3 crore. Against that, the number of Systematic Investment Plans (SIP) accounts with mutual funds are only 3.56 crore, according to data published by the Association of Mutual Funds in India (AMFI). And the net addition of SIP accounts in the first 10 months of FY21 was just 38.6 lakh.

This is an indication that investors have preferred the direct equity route (via stocks) over equity mutual funds. Retail participation in the NSE Cash market has gone up 8.3% and that of institutional investors and partnership firms has reduced by an equal number.

In my honest view, those who are shunning the mutual funds and taking the direct route are perhaps getting swayed away by the unprecedented market performance since April last year. However, during market sell-offs, investors pay a heavy price for such thoughtless decisions.

Even during the previous multi-year market boom that happened between 2003 and 2008; many investors blindly invested in infrastructure companies, power companies, and real estate companies. They also took a very high exposure to sectoral and thematic funds, and when markets collapsed in 2008 and the early part of 2009, they experienced massive wealth erosion. It took several years for such investors to flock back to the markets.

At this juncture, when markets are near the zenith and valuations look stretched; it is important that you take a prudent approach and follow asset allocation that is best suited to your investment objective. Avoid overexposure to equity; and when you invest in equities, opt for some of the best equity-oriented mutual funds and ensure that your portfolio is strategically structured. This will help you own an all-weather portfolio that is well-diversified across categories, sub-categories, investment styles and asset classes, considering your risk appetite, investments objectives, the financial goals you are addressing and investment horizon in this process.

To build the equity mutual fund portfolio, I suggest adopting the ‘Core & Satellite’ approach;–a time-tested investment strategy followed by some of the most successful investors that can help you get the best of both the worlds, i.e., the stability of large-sized companies and high return potential of smaller companies.

The term ‘Core’ applies to more stable, long-term holdings of the portfolio while the ‘Satellite’ applies to the strategic portion that would help push up the overall returns of the portfolio, across market conditions.

Your ‘Core’ holdings may comprise around 65%-70% of your equity mutual fund portfolio and consist of Large-cap Fund, Multicap/Flexicap Fund, and a Value Style Fund. The ‘Satellite’ holdings of the portfolio could be around 30%-35% comprising of a Mid-cap Fund, a Large-cap & Mid-cap Fund, and an Aggressive Hybrid Fund. If your risk appetite permits, you may also consider investing a small portion in a Small-cap Fund.

Following the Core & Satellite approach can help you in the following ways:

- Adequately diversify the portfolio

- Reduce the need for portfolio churning

- Optimize risks and portfolio returns

- Take advantage of a variety of investment strategies

- Create wealth, cushioning the downside

- Create a portfolio that can potentially outperform the market

The core & Satellite investment strategy may work for you in 2021 and beyond; it is an evergreen approach that brings along immense benefits.

When you invest in a diversified portfolio of equity funds, it will be beneficial if you stagger it over time, preferably through the Systematic Investment Plan (SIP) route.

If you are planning for long-term financial goals, consider SIP-ping into the best equity-oriented mutual fund schemes following the ‘Core & Satellite’ approach. And if you are already SIP-ping into some of the best equity mutual fund schemes, do not discontinue your SIPs irrespective of whether India achieves 8% GDP growth or falters in the path. To invest and generate wealth, India continues to be an attractive investment destination.

This article first appeared on PersonalFN here

{kind=link}