SEBI’s circular on Potential Risk Class (PRC) Matrix for debt mutual funds came into effect from December 01, 2021. The PRC matrix will apply to all existing debt schemes as well as all upcoming launches.

The existing Risk-o-Meter is based on the portfolio of the scheme and captures the actual risk in the portfolio taken by the fund. It is published on a monthly basis. On the other hand, the PRC matrix will show investors the maximum interest rate risk and credit risk a debt mutual fund can take. Each debt scheme will be classified under PRC matrix based on the maximum interest rate risk (measured by Macaulay Duration of the scheme) and the maximum credit risk (measured by the Credit Risk Value of the scheme).

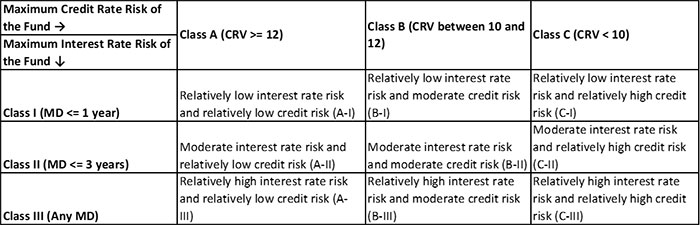

SEBI has offered Asset Management Companies (AMCs) the option to select any of the 9 combinations (see Table 2 below) to highlight the interest rate and credit risk attributes of the schemes. A scheme classified in A-I cell carries the least risk potential while those classified under C-III carries the highest risk potential. However, once the classification is done, the subsequent changes would be treated as the changes in the fundamental attributes of scheme.

The three buckets for measuring the interest rate risk based on Macaulay Duration (MD) are:

- Class I: MD <=1 year

- Class II: MD <=3 year

- Class III: Any (other) MD

In other words, the lower the MD, the lower would be the interest rate risk involved. The MD of the scheme will be the weighted average MD of each instrument in the portfolio of the scheme; weights are based on the proportion to the AUM. Moreover, the value of the debt instrument to be considered in calculating the AUM will include the accrued interest.

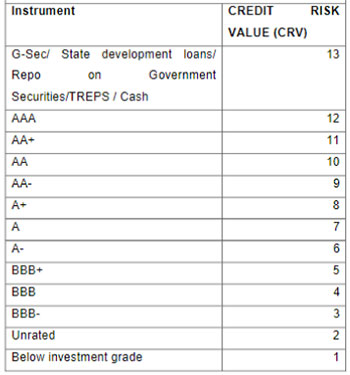

Similarly, different instruments will have pre-specified Credit Risk Values (CRVs) starting from 13 and going down to 1; wherein the highest value denotes the highest safety and vice versa. In other words, G-sec instruments will have a score of 13 and the below investment grade bonds will have a score of 1. The CRV of the scheme will be the weighted average credit risk value of each instrument in the portfolio, the weights will be based on their proportion to the AUM.

Table 1: Credit Risk Values of Debt Securities

(Source: SEBI)

As per SEBI, for investments by mutual funds in instruments having short-term ratings, the credit risk value will be based on the lowest long-term rating of an instrument of the same issuer (in order to follow a conservative approach) across credit rating agencies. But if there is no long-term rating of the same issuer, then based on credit rating mapping of Credit Rating Agencies (CRAs) between short-term and long-term ratings, the most conservative long-term rating will be taken for a given short-term rating.

The three credit risk buckets are as follows:

- Class A: CRV>=12

- Class B: CRV>=10

- Class C: CRV<10

Table 2: Risk Class Matrix for Debt Mutual Funds

(Source: SEBI)

So, if an open ended Short Duration Fund wants to invest in securities such that its Weighted Average Macaulay Duration is less than or equal to 3 years and its Weighted Average Credit Risk Value is 10 or more, it would be classified as a scheme with ‘Moderate Interest Rate Risk and Moderate Credit Risk’.

The maximum residual maturity of each instrument in the portfolio for a scheme placed in Class I (i.e. MD <=1 year) will be three years. Similarly, for scheme placed in Class II (i.e. MD <=3 years), the maximum residual maturity of each instrument in the portfolio will be seven years. A scheme placed in Class III can invest in instruments of any maturity.

The cap for Class I and Class II pertaining to maximum residual maturity of each instrument will not apply for securities issued by the central government and state governments.

The PRC positioning of the schemes will be mentioned in all the scheme related documents as well as communications to the investors, to enable them to make informed decisions.

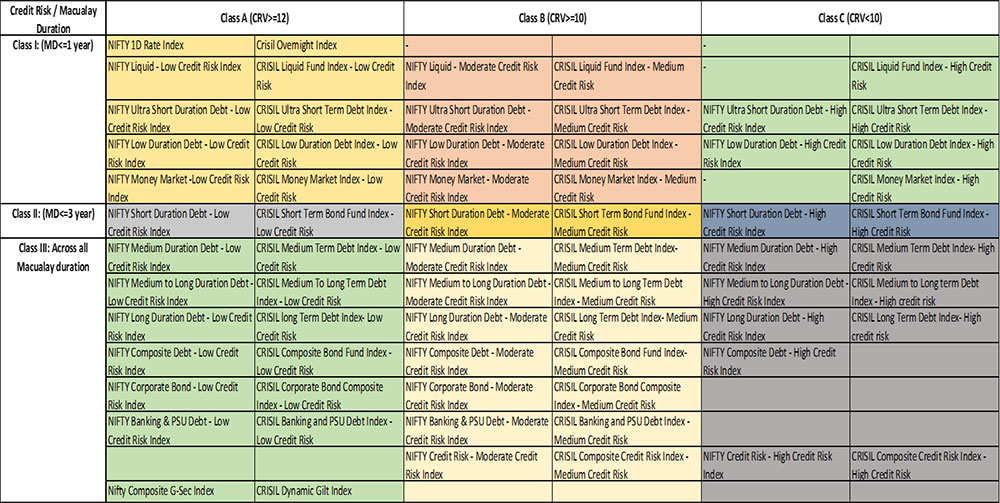

AMFI has released list of tier-I benchmarks for open-ended debt schemes based on the Potential Risk Class (PRC) matrix

As per SEBI directive, AMFI has provided the list of Tier-1 benchmarks that debt mutual funds can use based on the potential risk class (PRC) matrix.

For instance, if a Medium Duration Fund falls in the low credit risk matrix, fund houses can choose between Nifty Medium Duration – Low Credit Risk Index or CRISIL Medium Term Debt – Low Credit Risk Index.

Table 3: List of benchmarks based on Potential Risk Class Matrix

(Source: AMFI)

Here’s how the new norms will help investors to make well-informed decisions…

- The new potential risk class matrix and list of Tier 1 benchmark will help investors select suitable debt mutual fund schemes based on their risk profile and investment time horizon. Additionally, it will help investors compare and evaluate schemes within the same risk class. This eventually may help better product categorization and improve product suitability. It can also reduce instances of panic redemption during challenging market conditions.

- Earlier only certain categories such as Credit Risk Fund and Corporate Bond Fund had clear definition on how much credit risk it can take. Consequently, even relatively safer categories such as Liquid Funds exposed investors to undue risk by investing in low-rated instruments with view to generate higher returns. Moreover, even short term categories such as Ultra Short Duration Funds held securities with long term maturity of 5 years or more making it susceptible to higher volatility. The new norms will increase transparency as the scheme will not be able to assume higher risk than stated in the PRC matrix.

- To be able to classify as a ‘Class A’ scheme on CRVs, fund houses will have to chiefly target sovereign or AAA-rated instruments. This will eventually keep a check on yield hunting and investments in below AAA-rated instruments–a trait that was common among debt schemes before the Franklin Templeton’s fiasco came to light.

- If the scheme takes higher interest rate or credit risk than reflected in the PRC matrix, it will be considered as a change in fundamental attribute of the scheme. This will allow investors an exit window during which they can redeem their investment without any exit load.

To conclude, the new norms would help bring back the portfolio discipline amongst mutual fund houses, improve disclosures and achieve greater transparency. More importantly, the new rules will protect investors from potentially negligent investment practices at mutual fund houses.

It is important to note that the placement of a fund in a particular matrix does not mean it is bound to take that level of risk but it is the maximum risk that a fund manager can take. Therefore, it is important to use the Risk-o-Meter and PRC Matrix in conjunction with each other to select the most suitable scheme.

After assessing the suitability and risk profile based on the PRC Matrix, you also need to analyse the following factors to select the best debt mutual fund schemes within a category:

- The portfolio characteristics of the debt schemes

- The average maturity profile

- The corpus & expense ratio of the scheme

- The rolling returns

- The risk ratios

- The interest rate cycle

- The investment processes & systems at the fund house

Preferably select debt mutual funds that invest predominantly in securities issued by the government and public sector entities. Refrain from investing in schemes where the debt fund manager engages in undue yield hunting. Lastly, remember that investment in debt mutual funds is not risk-free. Therefore, make it a point to invest in congruence with your investment time horizon and risk tolerance.

This article first appeared on PersonalFN here

{kind=link}