Debt mutual funds witnessed net outflows of Rs 1.15 lakh crore in March 2022. The category had witnessed outflows of Rs 8,274 crore in February 2022.

Among the sub-categories of debt mutual fund, Liquid Fund saw the highest outflow of Rs 44,604 crore, while Overnight Fund saw outflows of Rs 12,852 crore.

Corporate Bond Fund, Short Duration Fund, Low Duration Fund, Banking & PSU Debt Fund, Floater Fund, and Money Market Fund were among the other sub-categories that witnessed massive outflows during the month.

This selling pressure is partly because of the quarter-end phenomena wherein corporates pull out money parked in Liquid and Overnight Fund to fulfil advance tax obligations and to pay-off short-term loans and other outstanding dues. These funds usually come back at the beginning of the next quarter.

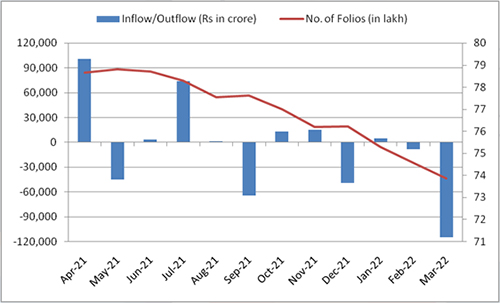

Graph: Debt mutual fund AUM and folios saw a sharp dip

Data as of March 31, 2022

(Source: AMFI, PersonalFN Research)

It is important to note that various debt mutual categories (excluding Liquid Fund and Overnight Fund) have witnessed persistent selling pressure over the past six months. The decline in flows has been highest in Short Duration Fund, Corporate Bond Fund, Banking & PSU Debt Fund, Credit risk fund, and Floater Fund categories.

The number of debt mutual fund folios too has steadily declined from 78.6 lakh in April 2021 to 73.9 lakh as of March 2022. This implies that the reason for selling pressure in the debt mutual fund categories is more than just quarter-end obligations.

The following could be the reason why investors have turned wary of debt mutual funds:

1. Debt mutual fund returns have turned unattractive in the last one year. Most categories, except Credit Risk Funds, are struggling to match returns on Bank Fixed Deposits. Debt mutual funds tend to perform well in a falling interest rate scenario. However, the interest rates are currently at a multi-year low due to RBI’s efforts to support economic growth. Furthermore, there is an expectation of a rate hike in the current financial year due to rising inflation. Accordingly, the rally in debt funds is almost over which has impacted returns on debt mutual funds.

2. With the chances of reversal in the interest rate cycle, investors are concerned about mark-to-market losses, especially on schemes that hold higher exposure to securities with long term maturity. Longer duration instruments are more sensitive to interest rate changes as compared to shorter duration instruments. Debt funds having exposure to medium to longer duration instruments tend to be more volatile in a scenario where there is an upside movement in interest rates.

3. Uncertainty about the timing, extent, and pace of the rate hike has made investors cautious about parking money in debt mutual funds. On the other hand, growing confidence among investors towards equity as an asset class and the better tax advantage that the category offers relative to debt could also be a reason why investors are turning away from debt mutual funds.

What should debt mutual fund investors do?

During the bi-monthly Monetary Policy Committee (MPC) meeting held on April 08, 2022, the RBI decided to keep the interest rate unchanged. Further, all members of the MPC voted to remain accommodative while focusing on withdrawal of accommodation to ensure that inflation remains within the target going forward, while supporting growth.

It is important to note that the inflation for March 2022 inched up to a 17-month high of 6.95%. The Russia-Ukraine war and COVID-19 induced global supply chain disruption, among other factors have caused inflationary pressure in the domestic market. This suggests that a hike in interest rate will be imminent in the current fiscal.

When the RBI starts hiking interest rates, debt mutual funds that invest in short-term securities will gain. Funds that invest in the short maturity segment witness minimal mark to market impact when interest rates rise. Therefore, you will be better off deploying your hard-earned money in shorter duration debt mutual funds such as Liquid Fund.

The lower residual maturity helps the fund to follow an accrual strategy where it can earn from coupon payments and roll over the assets on maturity. The accrual strategy also helps reduce the impact in a rising interest rate scenario.

[Read: Does Your Liquid Fund Follow the Principle of Safety? Know Here…]

Additionally, it is important to look at the credit profile of the schemes you are investing in. Even though economic sentiments have improved, avoid investing in schemes that hold higher allocation to moderate to low rated instruments as it can expose you to higher credit risk. Stick to debt mutual funds where the fund manager does not chase yields but instead focuses on government and quasi-government securities.

If you are willing to take slightly higher risk for better returns you can consider hybrid mutual funds such as Conservative Hybrid Fund or Balanced Advantage Fund.

Lastly, remember that though debt mutual funds are relatively stable compared to equity mutual funds the returns are not guaranteed. Therefore, it is important to understand the various risks involved viz. interest rate risk and credit risk before selecting a debt mutual fund for your portfolio; avoid selecting schemes based on their recent performance.

This article first appeared on PersonalFN here

{kind=link}