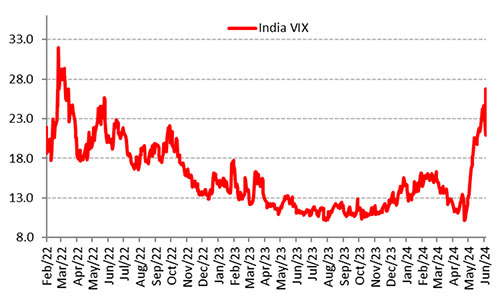

On the counting day of the Lok Sabha 2024 election results, i.e. June 4, 2024, the Indian equity market plunged worryingly – the S&P BSE Sensex by over 4,200 points and the Nifty 50 by over 1,300 points, a loss of nearly 6%, after gaining over 3% the previous trading day. This was a major single-day loss since February 2022.

India’s Volatility Index or VIX also jumped to nearly 40x, remarkably surpassing the level of 29 seen in May 2024.

Graph 1: India’s VIX jumped during the Lok Sabha 2024 election results

Data as of June 4, 2024

(Source: NSE, data collated by PersonalFN Research)

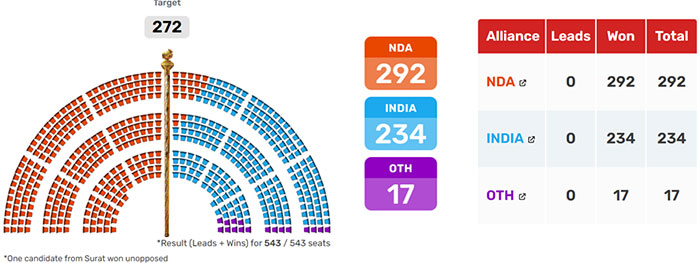

The key reason for market turmoil was the Bharatiya Janata Party (BJP), under the leadership of Shri Narendra Modi, failed to get a clear majority. It won 240 seats, 32 short of the halfway mark of 272 seats in the Lok Sabha.

The BJP’s alliance partners, mainly the TDP (under the leadership of Shri N. Chandrababu Naidu) and JDU (led by Shri Nitish Kumar), who secured 16 and 12 seats, respectively, plus all other partners, proved to be a saving grace for the National Democratic Alliance (NDA) taking the final tally of 292 but short of 300 mark – and no way close to 370 and 400 benchmarks set by the Modi-led-NDA government.

Image: Route to Political Power in Lok Sabha Election 2024

(www.indiatoday.in; as of June 4, 2024)

With some element of anti-incumbency and key issues such as unemployment, inflation and threat to democratic values highlighted well in the narrative of the opposition, the I.N.D.I.A (Indian National Developmental Inclusive Alliance) and other parties, managed to give a tough fight, securing 234 and 17 seats respectively.

While NDA technically has the numbers to form the government, the question is whether will it be led by Shri Narendra Modi as the Prime Minister. Media reports indicate that he will be taking oath on June 8, 2024, but whether he will continue to remain the Prime Minister for the complete term of five years needs to be seen. We have seen in the past that politics is a game of possibilities; equations could change if some candidates and parties decide to switch sides. So, there will be political uncertainty even if has the mandate for now. The Indian equity market too is perhaps taking this into account and therefore, is edgy (although partially recovered some of the loss of June 4, 2024).

The outcome of the general elections is set to shape government policies and have an impact on geopolitics, macroeconomic conditions, and society at large. In short, the outcome of the general election influences the country’s socio and economic outlook.

That said in my view, as long as good policies and reforms continue, irrespective of who leads the country, you need not be worried. Some of the worthy reforms under the Mod-led-NDA regime are:

- Make in India (to promote manufacturing in India)

- Production-Linked Incentive Scheme (for various sectors in the manufacturing space),

- Introduced numerous schemes for farmers

- Skill India (aimed at improving the skill set of youth and making them employable)

- Startup India (to promote the culture of entrepreneurship and innovation)

- Digital India (to make India a digitally empowered society)

- Unified Payment Interface or UPI (which made transacting online so much simpler),

- Simplified the indirect tax structure with the Goods & Services Tax or GST

- Focused on developing core infrastructure (roads, railways, ports, etc. to improve connectivity),

- Housing for the poor through the Pradhan Mantri Awas Yojana

- Financial inclusion through Jan Dhan Yojana

- The Direct Benefit Transfer scheme (aimed at transferring subsidies and other benefits directly to the beneficiaries’ bank account)

- Introduced social security schemes for the poor

- Enacted the Insolvency and Bankruptcy Code (giving powers to the lender to suspend the board, sue promoters and ensure speedy recovery)

- Set up bad banks (as part of a wider strategy to clean up the balance sheets of banks),

- RERA (a quasi-judicial body regulating builders and developers)…and many more!

With reforms continuity, the country can potentially be the third largest economy by 2027-28 (overtaking Germany and Japan), as well as improve its rank on purchasing power parity.

The IMF and the World Bank have estimated India’s GDP to grow at 6.8% and 6.6% respectively in FY25 considering robust domestic demand, the rise in public spending, and favourable demographics (more working-age population).

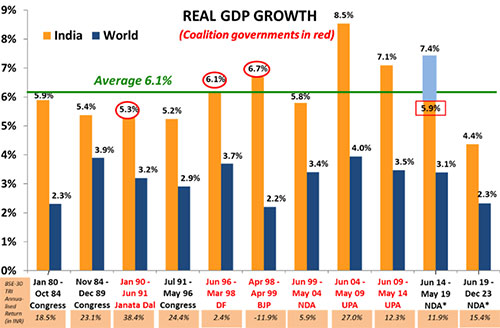

While one may argue that coalition government may make accomplishing the ranks difficult, the graph below is a testimony to the fact that during coalition governments, the real GDP growth has been usually better than when there is a single-party majority government. This is because the ideas of the partners are better heard and implemented.

Graph 2: GDP real growth rate across 10 governments

Note: RBI and https://parliamentofindia.nic.in/ as of December 2023. Note: The number in the red rectangle is from a changed data series starting Jan 2015. While a “superior” series, there is no comparable number to equate the “New” with the “Old”. Most economists deduct 0% to 1.5% from the “New” to equate to the “Old”; therefore, under Modi, the GDP has been at 5.9% at best matching the 5.6% under the BJP-led coalition government of Vajpayee resulting in a rout for the BJP at the time of the next election in 2004.* Please note that data used for World GDP for 2021 & 2022 is a median Estimate since World Bank data is not yet available and India GDP data is the government’s third advance estimate released at the end of February 2024.

Source:RBI and www.parliamentofindia.nic.in; data as of February 2024.

As seen in the graph above, the GDP growth across 10 governments has been 6.2% p.a. over the past 40 years. In my view, even if India’s GDP grows around the average GDP growth rate of around 6.0%, it would be decent enough to generate wealth. Also, what is important is that we see jobs-led growth and not jobless growth so that it yields a demographic dividend.

India’s GDP growth has reflected positively on the wealth creation process through equities as well over decades. India’s market cap-to-GDP ratio is at 132%, way higher than the long-term average of around 80%.

For the equity markets in the short run, sentiment and expectations will add to the volatility. But over the long run, it is the fundamentals that will drive the markets.

“In the short run, the market is a voting machine but in the long run, it is a weighing machine.” — Benjamin Graham (father of value investing and author of the best-seller, The Intelligent Investor)

As long as fundamentals are robust, the corporate earnings trend is positive, and foreign portfolio investors along with domestic investors (retail, HNI, and institutional) perceive Indian markets to be promising, you need not be worried about who is the leader at the helm.

The Indian equity market is currently commanding a premium to global peers. So, the correction witnessed on the counting day of election results, in a sense, was much needed and healthy after the bellwether index moved up rather unconvincingly on exit polls.

Going forward, if corporate earnings meet market expectations, then the valuation premium which Indian equities command, may still seem justified and may encourage participation of domestic and foreign investors.

Having said that, never get carried away by irrational exuberance and unrealistic earnings estimates. Often corporates and ‘sell- side’ analysts play the old trick in the book, wherein the long-term earnings are overestimated while the near-term earnings are possibly toned down.

Keep in mind that factors such as political stability, policy continuity, reforms, inflation dynamics, monetary policy actions, and infrastructure development that define growth are pivotal for corporate earnings. Particularly when there are ostensible clouds of global economic uncertainty and geopolitical tensions, you ought to tread carefully.

[Read: Key Risks to Watch Out for in 2024]

In such times what should you, the investor, do?

Well, if you have made prudent investments considering your risk profile, investment objective, the financial goals you are addressing and the time in hand to achieve the envisioned goals, you need not worry. Stay calm.

However, if you have been following your friends, colleagues, relatives, neighbours, etc. who may not be qualified to render valuable advice, or you have made ad hoc investments based on historical returns, then perhaps you carefully need to evaluate the portfolio.

Investing in an individualistic exercise, there is no such thing as a one-size-fits-all approach. You ought to invest as per the asset allocation best suited for you and diversify the portfolio.

Near the lifetime high of the Indian equity market, avoid skewing your portfolio to small-cap and mid-cap segments of the market, which have run up quite a lot and the margin of safety seems to have narrowed. If the markets correct further from the current levels mid-caps and small-caps would be more vulnerable than large-caps.

Do large-cap mutual funds make more sense in an overheated and volatile equity market? Click here to know.

Broadly, when approaching equity mutual funds, it would be wise to follow a ‘Core & Satellite’ strategy – which is followed by some of the most successful equity investors around the world.

It would be worthwhile holding a Large Cap Fund, a Flexi-cap Fund, and a Value Fund as part of your Core holdings (around 65-70% of your equity portfolio) with a time horizon of around 3 to 5 years. Doing so shall offer you portfolio stability.

The Satellite holdings (around 30-35% of your equity portfolio), on the other hand, may comprise a Mid Cap Fund and a Small Cap Fund provided you have a long time horizon of around 7 to 8 years and the stomach for high-risk. This would help push up the overall returns when the market conditions favour these market cap segments.

For tactical asset allocation to three key asset classes, i.e., equity, debt, and gold, a Multi-Asset Fund would also be a meaningful choice now to reduce risk. As you may be aware, there is no consistent winning asset class; markets are cyclical (full of ups and downs). For this reason, asset allocation is called the cornerstone of investing and investing in multi-asset funds makes sense.

Want to know more about which are the Best Multi-Asset Allocation Funds? Watch this video:

By wisely structuring your investment portfolio and devising a sensible strategy, you could earn optimal returns with optimal diversification and reduce the risk to the portfolio.

When choosing among the best mutual funds, do not give much weightage to past performance. It will be akin to driving a car by predominantly looking at the rare view mirror, potentially proving disastrous.

You see, the historical performance of mutual funds (and stocks) is in no way indicative of how they would yield returns in the future. Instead, assess how the scheme has fared across market phases (bull and bear), assess the risk the fund has exposed its investors to, the portfolio characteristics, the risk mitigation measures, the philosophy of the fund house and whether they follow sound investment processes and systems to drive performance in the long run.

Lump sum v/s SIP

As regards, the question of whether to invest a lump sum or through the SIP (Systematic Investment Plan) mode. Well, given that the markets are at a lifetime high and there may be evident ups and downs in the equity market due to several risk factors in play, even if you have the surplus funds to invest, it would be prudent to stagger your investments. Meaning, invest it in parts or piecemeal manner keeping an eye on the opportunities available. Keep the powder dry and use market corrections as an opportunity to buy for the long-term.

When planning for envisioned financial goals, it is better to take the SIP route, which shall help mitigate or reduce the ups and downs of the Indian equity markets, make timing the market irrelevant, instil investment discipline, and potentially compound your wealth in the long run. SIPs, particularly when planning to achieve certain long-term financial goals, are a worthwhile mode of investing.

Historical data shows that in the ensuing years after the general elections, the Indian equity market has clocked attractive double-digit returns for investors. Nevertheless, set your risk-return expectations right and avoid hinging it on past returns.

If you already have been investing in equities and have a portfolio of equity-oriented funds, I suggest you first review the investment portfolio comprehensively seeking the help of a proficient SEBI-registered investment advisor. This will help you, the investor, in the following ways…

- Ensure that your investments and the asset allocation are in line with the financial objectives/goals, the risk appetite, and the time in hand to achieve the envisioned financial goals

- Facilitate portfolio rebalancing and consolidation

- Weed out the underperformers and replace them with better and more suitable ones

- Minimise portfolio risk and ensure the liquidity of the portfolio

- Facilitate portfolio optimal structuring and portfolio diversification

- And keep a check if you are on track to accomplish the envisioned financial goals

Amidst, the outcome of Lok Sabha elections, avoid getting absorbed by the noise. Keep emotions under control and be a thoughtful investor.

Happy Investing!

Note: This write-up is for information purposes and does not constitute any kind of investment advice or a recommendation to Buy / Hold / Sell a fund. Returns mentioned herein are in no way a guarantee or promise of future returns. Mutual Fund Investments are subject to market risks, read all scheme-related documents carefully before investing.

This article first appeared on PersonalFN here

{kind=link}