If you are new to stock markets and have made your first investment in equity mutual funds during the pandemic, you have most likely earned attractive returns over the last 15-18 months. But here are some words of caution: don’t get swayed and set unrealistic return expectations. Many of you may not have seen prolonged bearish market phases.

In the year 2022, if you are hoping to see a double-digit return from equity as an asset class and your equity mutual funds, the Indian equity markets are likely to disappoint you.

I don’t want to frighten you with a bearish commentary, but it’s important for you to have the right assessment of the macroeconomic situation and that of markets. If you want to sail through 2022, you need to have realistic return expectations.

Table 1: Historical Annual Returns clocked by various sub-categories of equity mutual funds

| Category | Category Average Returns (Absolute %) | |||||||

| 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | |

| Small cap Fund | 79.1 | 11.3 | 6.8 | 51.4 | -16.4 | -0.3 | 31.9 | 65.1 |

| Mid Cap Fund | 71.7 | 8.6 | 4.8 | 43.8 | -10.6 | 4.2 | 25.8 | 46.3 |

| Multi Cap Fund | 57.6 | 5.3 | 2.9 | 41.6 | -6.1 | 8.2 | 16.4 | 44.5 |

| Dividend Yield Fund | 46.0 | -3.5 | 7.7 | 37.4 | -7.3 | 4.4 | 20.5 | 39.8 |

| Large & Mid Cap Fund | 52.7 | 5.5 | 7.4 | 39.8 | -6.2 | 9.7 | 17.2 | 39.1 |

| Contra Fund | 51.3 | 1.4 | 6.8 | 42.3 | -3.9 | 6.1 | 23.6 | 38.1 |

| Value Fund | 61.4 | 3.9 | 7.8 | 41.2 | -8.9 | 2.8 | 16.2 | 37.2 |

| Flexi Cap Fund | 51.3 | 2.7 | 4.8 | 36.5 | -3.2 | 11.3 | 17.5 | 33.3 |

| Focused Fund | 53.7 | 3.8 | 6.5 | 38.5 | -5.5 | 12.6 | 17.4 | 33.1 |

| Large Cap Fund | 42.3 | 1.9 | 4.4 | 32.0 | -0.8 | 12.9 | 15.2 | 27.3 |

| NIFTY 50 – TRI | 32.9 | -3.0 | 4.4 | 30.3 | 4.6 | 13.5 | 16.1 | 25.6 |

| NIFTY 500 – TRI | 39.3 | 0.2 | 5.1 | 37.7 | -2.1 | 9.0 | 17.9 | 31.6 |

Data as of December 31, 2021

(Source: ACE MF, PersonalFN Research)

In Table 1 seen above, the highlighted categories have been the top performers in the respective years. For instance, Small-cap Funds outperformed all other sub-categories of equity mutual funds in 2020 and 2021. During the COVID-19 pandemic, as ultra-accommodative fiscal and monetary policies were followed across the globe and that caused unprecedented rallies in global equities; small-caps emerged to be the biggest beneficiaries of this trend.

But the two years preceding 2020 belonged to Large-cap Funds and during this time period, the Small-cap Funds remained at the bottom of the return tally. In 2016, Value Funds outperformed. So in short, no single category has managed to outperform consistently throughout the 8-year period.

And if you delve deeper and analyse the reasons for outperformance, you will see a pattern. If you remember, between 2011 and 2013, the markets were under pressure for various reasons-sovereign debt crisis in Europe, falling Indian rupee, rising Non-Performing Assets (NPAs) in the Indian banking system, and so on. As a result, the small and mid-caps stocks received mighty blows in those three years and valuations became cheap.

In 2014 after the Modi-led-NDA government came to power with a thumping majority, the market sentiment improved substantially and the overall stability in the global markets helped those smaller companies triumph, i.e. the mid-cap and small-cap category outperformed in 2014 and 2015.

The U.S. Federal Reserve (Fed) started increasing the interest rates in December 2015 for the first time after the 2008 global financial crisis. Due to this, the market sentiment turned weak in 2016 and the valuations of small-caps suddenly started appearing expensive. This caused the growth momentum to decelerate. Needless to say, Value Funds outperformed in 2016.

In December 2016, the Fed initiated another rate hike, despite which markets rallied in 2017. Back home, factors such as demonetisation nudged conventional investors to turn towards financial assets, which in a way helped the Indian markets. But with Fed raising rates thrice in 2017, the markets became jittery.

In 2018, the Fed went with four rate hikes, thereby the rates of Fed funds effectively went up from 0.25% in 2015 (before the first rate hike) to 2.5% by December 2018. During this difficult phase, the market rallies became narrower.

Speaking about the Indian economy, the double speed-breakers in the form of demonetisation and the challenges in GST affected the pace of economic growth. Only the big companies managed to sail through, while the informal economy suffered miserably. That’s one of the reasons why Large-cap Funds outperformed in 2018 and 2019.

And in the last two years, we all know what happened: we saw a broad-based rally across the large-caps, mid-caps, and small-caps, as people chose to save and invest in equities amidst the pandemic supported by favourable liquidity conditions due to accommodative monetary policy stance followed by major central banks of the world. The extraordinary performance of equities attracted lots of new investors to the equity markets. Those who selected equity mutual funds made striking double-digit returns in 2021, particularly in Small-cap Funds.

You see, small-caps were cheaper at the start of the COVID-19 pandemic, but now these look expensive compared to large caps despite the correction since the peak. The P/E multiple of the S&P BSE Midcap and S&P BSE SmallCap Index is around 28x and 47x, respectively — not offering enough margin of safety.

Currently, the equity markets are likely to experience certain headwinds. The Fed has hinted at aggressively rolling back its bond-buying programmes and raising interest rates at least three times in 2022. This is likely to make the year 2022 a tricky one for the equity markets.

Also, please do not underestimate the threat of a surge in COVID-19 cases (Delta + the Omicron variant) across India. The current vaccines are not holding up against the new Omicron variant. Also, the uneven distribution of vaccines has been creating disparities globally in the fight against coronavirus. As of January 10, 2022, India’s active case count touched 7.24 lakh and the daily new caseload was over 1.3 lakh. As a precautionary step, the Indian government has rolled out a booster dose for healthcare and frontline workers, as well as for senior citizens with co-morbidities.

The coronavirus pandemic poses a potential risk to economic activity and may have a bearing on corporate earnings if further restrictions or localised lockdowns are imposed. After the state assembly plus municipal elections conclude, India could witness a spike in daily new cases; this could weigh down on business and consumer sentiments.

The RBI’s Financial Stability Report released in December 2021 warns of loss in GDP growth because of Omicron threat and clouded near term outlook. It is very likely that the RBI may revise India’s full-year FY22 GDP growth projections downwards from 9.5%. The National Statistical Office (NSO) has already pared India’s GDP growth estimate to 9.2% in FY22 from 9.5% projected earlier, indicating that consumption (which comprises 55% of the GDP) may take a hit.

Under such circumstances, overheated equity markets might find it difficult to justify high valuations, thereby posing a threat to the potential stock market returns. In 2022, the Indian equity markets are expected to move in a pro-cyclical manner rather than in a counter-cyclical way as witnessed in 2021 and 2020.

So how should you position your investment portfolio in 2022?

Striking the right asset allocation mix is the best way to mitigate the impact of uncertain and volatile market conditions. This involves investing across equity, debt, and gold, etc. based on your risk profile, investment objectives, the financial goals you are addressing, and the time in hand to achieve those goals.

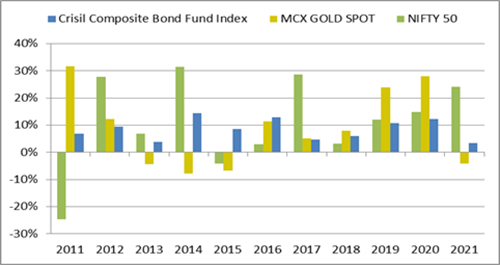

If a particular asset class performs poorly in a year, a sensible allocation to other asset classes would help lower the risk of the investment portfolio, provide freedom from timing the market (as long as you have made the best investments), earn efficient inflation-adjusted returns, and ensure adequate liquidity of the portfolio. The graph below depicts that not all asset classes perform well at all times. There have been instances where equities have failed to deliver returns.

Graph 1: Annual performance of various asset classes

Data as of December 31, 2021

(Source: ACE MF, PersonalFN Research)

“It is the part of a wise man to keep himself today for tomorrow, and not venture all his eggs in one basket,” wrote the Spanish writer, Miguel de Cervantes, in the novel Don Quixote. Thus, take care to ensure that your portfolio is well-diversified in 2022 and beyond.

The overall returns on the investment portfolio would hinge on the asset allocation best suited for you, the type of mutual fund schemes you hold and the performance of their underlying portfolios.

To invest in equity mutual funds in 2022 and beyond, follow a time-tested ‘Core & Satellite’ approach. Many experienced successful equity investors have adopted this investment strategy and benefited from it. The Core & Satellite approach allows you to take advantage of the higher margin of safety and stability large-caps offer while simultaneously capitalising on the potential high growth opportunities of small and midcaps.

The term ‘Core’ applies to the more stable, long-term holdings of the portfolio, whereas the term ‘Satellite’ applies to the strategic portion that would help push up the overall returns of the portfolio across market conditions. The ‘Core’ holding should comprise around 65-70% of your equity mutual fund portfolio and consist of a Large-cap Fund, Flexi-cap Fund, and Value Fund/Contra Fund. Whereas the ‘Satellite’ holdings of the portfolio can be around 30%-35%, comprising of a Mid-cap Fund, an Aggressive Hybrid Fund, and maybe a tiny portion in a Small-cap Fund (if you have a time horizon of at least 8 to 10 years and the stomach for high risk).

By wisely structuring and timely reviewing the Core and Satellite portions and the holdings therein, you would be able to add stability to the equity mutual fund portfolio while strategically boosting your portfolio returns at the same time.

The ‘Core & Satellite Investment Strategy’ would facilitate optimum diversification across market capitalisation and investment styles to gradually build wealth in the long run. But take care to select the best equity mutual funds for investments for the long term.

Here are a few ground rules to follow to build a portfolio of equity mutual fund schemes based on the Core & Satellite strategy:

1) Consider equity mutual funds that have a strong track record of at least 5 years and have been amongst the top performers in their respective categories.

2) The schemes should be diversified across investment styles and fund management.

3) Ensure that each equity mutual fund selected scheme abides with its stated objectives, indicated asset allocation, and investment style.

4) You should not only invest across investment styles (such as growth and value), but also across fund houses.

5) The equity mutual fund schemes should be managed by experienced and competent fund managers and belong to fund houses that have well-defined investment systems and processes in place.

6) Not more than two equity mutual fund schemes managed by the same fund manager should be included in the portfolio.

7) Not more than two equity mutual fund schemes from the same fund house shall be included in the portfolio.

8) Each equity mutual fund scheme that is to be included in the portfolio should have seen an outperformance over at least three market cycles.

9) You should restrict the count of equity mutual schemes in your portfolio to seven.

Since the markets are expected to remain volatile as the liquidity dries up, it would be wise to take the Systematic Investment Plan (SIP) route to build a portfolio of the best equity mutual fund schemes following the ‘Core and Satellite’ approach.

[Read: 3 Best ELSS for 2022 to Save Tax]

If you correctly follow the ‘Core & Satellite’ approach when investing in equity mutual funds, here are the six key benefits it will adduce:

1) Facilitate optimal diversification among the best equity mutual fund schemes.

2) Reduce the need to frequently churn your entire equity mutual fund portfolio.

3) Reduce the risk to your equity mutual portfolio.

4) Enable you to benefit from a variety of investment styles and strategies.

5) Create wealth by cushioning the downside.

6) Help you to potentially outperform the market.

Note, the Core & Satellite investment strategy may work for you in 2022 and beyond.

This article first appeared on PersonalFN here

{kind=link}