Over the last one year, bond yields in the U.S. have been rising steadily. Historically, rising bond yields in the U.S. has been negative for emerging markets. That’s because when bond yields in the U.S. rise, capital flows to emerging markets such as India, and consequently, either contract or flow back to the world’s largest economy.

Moreover, with the U.S. economy witnessing a strong recovery now, interest rate reversal and tapering of bond-buying (from USD 120 billion per month) by the U.S. Federal Reserve looks inevitable in the future.

But there’s a major difference this time. You see, unlike in the previous monetary tightening cycle, this time the balance sheet of the U.S. appears fairly large and capex plans of the U.S. government are extremely ambitious.

In February 2020, the U.S. Federal Reserve’s balance sheet was USD 4.1 trillion, which has now ballooned to around USD 8.5 trillion. Such a massive jump in just 18 months is likely to make it difficult for the Federal Reserve to raise interest rates in a hurry. It is expected that the balance sheet size will only grow going forward. The U.S. Senate has already cleared a USD 1-trillion infrastructure spending plan.

As a result, the pace of monetary tightening, as and when it happens, is expected to be very gradual. The Federal Reserve may not increase interest rates significantly even though the economy is recovering and inflation is inching up. Interest rates may be kept near zero, but the bond-buying taper may start by mid-November or December this year.

How will all this impact India’s capital markets?

Well, it would have a significant bearing on high-risk assets such as equities, as well as gold and bonds.

If bond yields in the U.S. continue to move northward, equity markets may crack under pressure. Foreign Portfolio Investors (FPIs) may turn net sellers in equities.

Higher yields in the U.S. may bring about higher yields and interest in the Indian debt market as well. As a result, there may a tactical shift from equity to debt instruments.

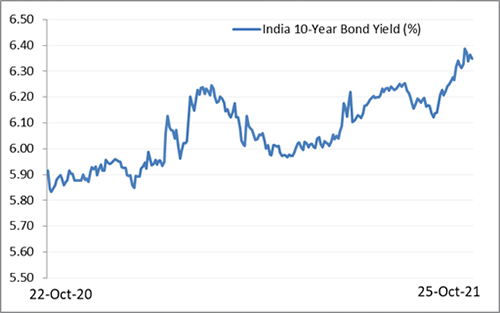

India’s 10-year G-sec bond yield has risen from 5.92% a year ago to 6.35% as of October 25, 2021, following in the footsteps of their developed-market counterparts.

Graph 1: India’s 10-year benchmark yield has climbed up since last year

Data as of October 25, 2021

(Source: Investing.com; PersonalFN Research)

Rising inflation, higher government borrowings and RBI hinting at normalisation have been the primary reasons for rising bond yields. Nevertheless, since the last couple of months, the 10-year G-sec yield is well-anchored to around 6.00% on account of the RBI’s proactive liquidity management.

According to the minutes of the 31st meeting of RBI’s Monetary Policy Committee held between October 6, 2021, and October 8, 2021, the system’s liquidity remained in large surplus and the average daily absorption rose to Rs 9.5 trillion in the first week of October 2021 (from Rs 7.7 trillion in July-August this calendar year).

The absorption under overnight Fixed Rate Reverse Repo has been Rs 4-4.5 lakh crore until now. And according to RBI’s estimates, the absorption through the overnight window is likely to be in the range of Rs 2-3 lakh crore even in December 2021.

Besides, auctions worth Rs 1.2 lakh crore under the secondary market Government Securities Acquisition Programme (G-SAP 2.0) during Q2:2021-22 provided liquidity across the term structure.

In the wake of the current and anticipated comfortable liquidity position in the future, and perhaps hinting at the normalisation of policy rates; the RBI has decided to discontinue G-SAP (which was essentially launched amid the outbreak of pandemic to address the liquidity concerns). But the RBI Governor Mr Shaktikanta Das has also mentioned his readiness to undertake G-SAPs as and when warranted by liquidity conditions, plus conducting Operation Twists (OTs) and Open Market Operations (OMOs).

To revive and sustain growth on a durable basis as well as continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward; the six-member Monetary Policy Committee of the RBI in the last bi-monthly monetary policy meeting have decided to continue with the accommodative stance as long as it is necessary. Except for Prof. Jayanth R. Varma, all other members of the MPC have voted to continue with the accommodative stance as long as necessary.

In RBI’s assessment, if there’s no further disruption on account of the pandemic, supply-side constraints may fade away sometime in FY23. Currently, close to 55% of the 404 industries are still operating at below FY20 levels, highlighting that supply constraints and lack of demand revival are deep-rooted structural problems that require policy attention.

Thankfully, the balance sheets of Indian corporates appear substantially deleveraged with their average debt-to-equity ratio falling from 60% in FY16 to roughly 35% in FY21. Also, corporate earnings have improved remarkably, supported by a favourable base effect, conscious cost reduction operation, a gradual pick-up in demand, and calculated capital expenditure.

At the same time, the results of listed Indian companies for Q2FY22 clearly show a build-up of inflationary pressure stemming from higher power and freight costs besides the short supply of certain commodities. In addition, crude oil prices are exacerbating the inflationary pressure. While some manufacturers are absorbing these higher costs, others are passing it on. It remains to be seen if inflation alters the demand revival in any way.

The festive demand is expected to be supportive of corporate earnings numbers. With the 100-billion-doses mark crossed and a better inoculation rate, near-normal economic activity is likely to prevail and boost consumer and business confidence. Having said that, the risk emanates from the looming third wave of COVID-19.

Principal Scientific Advisor, Prof. K. Vijay Raghavan, has called the third wave ‘inevitable’. Dr VK Paul, the national COVID-19 taskforce chief, speaking with India Today expressed concern that nearly 10 crore Indians who are due for the second dose of COVID-19 aren’t taking it. The new AY 4.2 variant, which is a sub-lineage of the Delta variant and considered to be highly transmissible if not necessarily fatal; is already circulating in certain states of India. And in light of the festivities of Diwali, the central government has asked states to take “utmost precautions”.

As regards the impact of bond yields in the U.S. on gold, the spotlights would turn away from gold and it may lose some of its sheen. The factors that could prop up gold price would be the high debt-to-GDP ratio in many parts of the world, rising inflation, stock market volatility, and the COVID-19 pandemic.

What should your investment strategy be?

When you approach equities for capital appreciation, don’t ignore your risk profile, time horizon in hand before the envisioned financial goals befall, and valuations. The valuation of the Indian equity markets is currently way ahead of other emerging markets. The current ground realities in India currently do not justify the lofty valuations. The margin of safety appears to have narrowed, and thus, the chances of some correction — around 5-10% — from the current elevated levels or intensified volatility cannot be ruled out.

Take note of the famous quote: “Be fearful when others are greedy and greedy when others are fearful”, by the legendary investor, Mr Warren Buffett. Given the risks at play, set realistic expectations from your equity investment and invest with a long term view.

In the current market scenario, it would be wise to diversify across market capitalisation via multi-cap funds or flexi-cap funds while holding some proportion of your equity allocation in large-cap funds as well as mid-cap funds. This is because, large-caps are established names, and the biggest advantage of having them is the stability they can provide to your portfolio. Large-cap funds should ideally be a part of the core holdings of your portfolio. Whereas to clock higher returns by assuming very high risk, mid-cap funds can be a part of your satellite portfolio, provided you have an investment time horizon of over 5-7 years.

Make sure you invest only in the best diversified equity funds, either directly or via the equity-oriented Fund of Fund scheme in a staggered manner. When planning for long-term financial goals, consider SIP-ping into mutual funds. It will enable you to mitigate the volatility with the inherent rupee-cost averaging feature and help you compound wealth in the long run with the required financial discipline.

If you are looking to preserve wealth, along with the investment horizon, pay attention to the interest rate cycle. The current interest rate cycle seems to have bottomed out. Most of the rally at the longer end of the yield curve has already come about since the time RBI started reducing policy rates.

In other words, debt funds with longer maturity papers may not be able to generate attractive returns as seen in the last couple of years. In the current uncertain times, the longer end of the yield curve could be more sensitive than the shorter end. The returns may moderate on the longer end of the yield curve and could turn riskier (may encounter high volatility) in the foreseeable future.

If you have an investment horizon of around 2-3 years and are a moderate risk-taker, consider investing in the best Banking & PSU Debt Fund. For an investment horizon of 6 to 12 months, you may invest in the best Low Duration Fund. But stick to a scheme with respectable portfolio characteristics, where the fund manager does not chase yields by taking higher credit risk but instead focuses on government and quasi-government securities.

Ideally, to approach debt funds now, the shorter end of the yield curve looks more attractive. You’ll be better off deploying your hard-earned money in shorter duration debt mutual funds. So for an investment time horizon of 3 to 6 months, consider the best Ultra-Short Duration Fund. Take care not to opt for a scheme that has a higher allocation to moderately rated instruments or those investing predominantly in instruments issued by private issuers.

For the extreme short-term investment horizon of up to 3 months, you may consider the best Liquid Fund that typically invests in Treasury Bills, Commercial Papers, Call Money, Certificates of Deposits, and so on. This helps them keep interest rate risk to a minimum. Invest preferably in a pure Liquid Fund, wherein you should not have any exposure to private debt papers. Remember, the returns are secondary when you invest in a liquid fund. The main objective is to keep your hard-earned money secure but highly liquid. So, do not expect remarkable returns from a Liquid Fund.

Note that investing in debt mutual funds earns you market-linked returns. It is neither risk-free nor safe.

If you are not comfortable parking your investments in debt funds and wish to keep your capital safe; invest in bank fixed deposits by choosing the bank carefully.

This article first appeared on PersonalFN here

{kind=link}