When an investor deploys his/her hard-earned money in any mutual fund scheme, often three aspects are looked at: the scheme’s investment mandate; its investment objective; and the performance track record.

But when the fund manager of the scheme does not stick to the investment mandate set out, not only does it potentially endangers the scheme’s investment objective but also exposes investors to an unprecedented level of risk — quite dissimilar to what was anticipated at the time when the initial investments were done.

Some debt scheme fiascos are the burning examples of the recklessness and apathy mutual fund houses have demonstrated towards their investors. When a short term debt fund loses money on account of defaults, it only reveals the weaknesses in the investment processes & systems at the fund house level. The best way to correct this behaviour is to impose stricter disclosure norms on mutual funds and make them more accountable so that tracking misconduct can become easy.

Last month, the Securities and Exchange Board of India (SEBI) revised disclosure norms for transactions in debt and money market securities by mutual funds, which came into effect from October 1, 2020. My colleague, Divya Grover, wrote an extensive piece explaining how this would prove to be in the investors’ interest.

[Read: SEBI Brings In New Norms to Improve Transparency in Debt Securities Transaction by Mutual Funds]

The capital market regulator wants to make sure that fund houses clearly communicate with their existing and potential investors.

Time and again, the regulator has advised fund houses to stick to their labels and convey the risks involved in mutual fund investing clearly. Keeping this in mind, last week the regulator (vide a circular dated October 5, 2020), based on the recommendation of its Mutual Fund Advisory Committee (MFAC) reviewed and revised the guidelines for product labelling of mutual fund schemes. The new risk-o-meter guidelines come into force from January 1, 2021, and will apply to all existing schemes and new schemes to be launched on or thereafter.

At present, mutual fund schemes are classified across five risk levels, namely – Low risk, Moderately low risk, Moderate risk, Moderately high and High risk. The capital market regulator, now, has introduced a new sixth level i.e. very high risk.

Moreover, the market regulator has directed mutual fund houses to carry out the exercise of risk labelling at the ‘scheme level’ as against the earlier practice of being done at the scheme category level. So, if all mutual funds classified their equity schemes in the ‘high risk’ category earlier, now the classification will differ from one scheme to another depending on their portfolio attributes.

Risk evaluation for equity schemes…

The calculation of risk value for an equity scheme is fairly straight forward. Large caps will be assigned a risk score of 5, mid-caps 7, and small caps will have the highest risk score of 9, as per the capital market regulator.

The market capitalisation data as published by AMFI on a six-monthly basis shall be considered.

Based on the weighted average of the above Market Capitalisation values of each security (weights being AUM of the security), Market Capitalisation Value of a portfolio shall be assigned.

(Source: SEBI/HO/IMD/DF3/CIR/P/2020/197)

Besides market cap, price volatility will be the other parameters used to calculate the overall risk value of a scheme on the portfolio weighted average basis.

Based on the weighted average of above volatility values of each security (weights being AUM of the security), Volatility Value of a portfolio shall be assigned.

If an instrument is traded on multiple stock exchanges, then the most conservative volatility value across stock exchanges for a given month shall be considered.

(Source: SEBI/HO/IMD/DF3/CIR/P/2020/197)

For securities with daily volatility of less than or equal to 1% (based on past two years prices), the volatility value assigned shall be 5, while for those whose daily volatility is greater than 1%, a volatility value assigned shall be 6.

Further, as per the capital market regulator, the average impact cost of the security for the previous three months including the month under consideration shall be evaluated as a measure for liquidity. The impact cost value should be assigned as under:

Based on the weighted average of impact cost values of each security (weights being AUM of the security), impact cost value of a portfolio shall be assigned.

If an instrument is traded on multiple stock exchanges, then the impact cost shall be based on the average value of impact costs across stock exchanges for a given month.

(Source: SEBI/HO/IMD/DF3/CIR/P/2020/197)

With the above, the less volatile and more liquid securities will have lower risk values and vice-a-versa.

Initial Public Offers (IPOs) and equity derivatives as well will carry risk values following a similar process (with a few variations to the score value assigned).

Measuring risk in debt funds…

Risk scores for the debt schemes will be assigned by taking the simple average of scores on three parameters: credit risk score; interest rate risk score; and liquidity risk score.

Here’s how it will work…

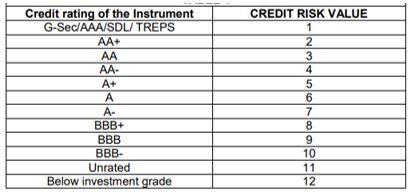

Depending on the credit rating of an instrument and the weightage of the security, the credit risk value for each security will be calculated and added to arrive at the credit risk value of the scheme.

Based on the weighted average value of each instrument (weights based on the AUM), credit risk value of the portfolio shall be assigned.

The price of a debt instrument to be considered for calculating AUM shall include the accrued interest i.e. dirty price.

For the above purpose, the credit rating of the instrument as on the last day of the month shall be considered

(Source: SEBI/HO/IMD/DF3/CIR/P/2020/197)

‘AAA’ rated instruments and sovereign securities etc. will have the credit value of 1 (least risky) and below-investment-grade securities will have a credit value of 12 (denoting the maximum risk).

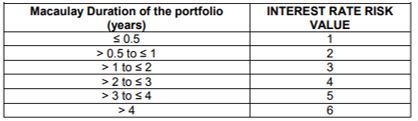

For calculating the interest rate risk, the capital market regulator has prescribed using the Macaulay Duration (MD) of the Portfolio. Macaulay Duration, named after Frederick Macaulay, is the weighted average term-to-maturity of the cash flows from a bond. The weight of each cash flow is determined by dividing the present value of the cash flow by the price.

For the above purpose, Macaulay Duration of an instrument as on the last day of the month shall be considered.

(Source: SEBI/HO/IMD/DF3/CIR/P/2020/197)

As per the regulator, the portfolio of 6 month’s duration will have the lowest interest rate risk value of 1 and for debt papers with MD of over 4 years will have the maximum risk value of 6.

As far as liquidity risk is concerned, a scheme will have to take into account the credit rating, nature of instrument and issuer’s profile among others, plus the listing status of the security. Tri-party repos and government securities will have the lowest risk value of 1 and below-investment-grade unrated securities will have the highest liquidity risk score of 14.

Similarly, if the liquidity risk value is higher than the average of credit risk value, liquidity risk value and interest rate risk value; then the liquidity risk will be considered as the risk value of the debt scheme.

The capital market regulator has taken an ultra-conservative approach to factor in credit risk and liquidity risk in the risk-o-meter, which, in my view, was much warranted.

For investments in Real Estate Investment Trusts (REITs), Infrastructure Investment Trusts, (InvITs), gold and gold-related instruments, foreign securities, as well as units of mutual fund schemes held by a mutual fund the capital market regulator has outlined risk evaluation guidelines to be followed by fund houses.

Based on a comprehensive risk evaluation process, the final risk-o-meter will reflect the risk as under:

| Risk value | Risk-o-meter reading |

| Less than or equal to 1 | Low |

| Greater than 1 but less than or equal to 2 | Low to Moderate |

| Greater than 2 but less than or equal to 3 | Moderate |

| Greater than 3 but less than or equal to 4 | Moderately High |

| Greater than 4 but less than or equal to 5 | High |

| Greater than 5 | Very High |

(Source: SEBI/HO/IMD/DF3/CIR/P/2020/197)

Disclosure requirements:

Mutual fund houses are expected to evaluate the risk-o-meter on a monthly basis and disclose the reviewed risk-o-meter along with the portfolio disclosures for all their schemes on their respective website and the AMFI website within 10 days from the close of each month.

Besides, on the 31st March every year, mutual funds are expected to disclose the number of times risk level has changed over the year, on their website and AMFI website in the format below:

(Source: SEBI/HO/IMD/DF3/CIR/P/2020/197)

Furthermore, all advertisements and other corporate communications including KIMs, SIDs and Common Application Forms must disclose the risk-o-meter in proximity to the caption of the scheme.

How will the changes in the risk-o-meter affect existing and potential mutual fund investors?

The risk-o-meter in its new form will definitely capture a lot more information about risks involved, especially in case of debt funds. Since the capital market regulator has taken an ultra-conservative approach in the calculation of risk scores of shorter maturity debt instruments, it highlights the regulator’s concern for investors who have received possibly the rudest shocks in the recent past. Fund managers, who in the past over-stepped the investment mandate to generate high returns at unprecedented risk, may become more careful and stop finding ways to get around with regulations.

Going forward, most of the equity funds will be re-labelled as ‘very high-risk’ funds, and rightly so.

Moreover, the new risk-o-meter guidelines would certainly help investors understand the risk traits of a scheme not just at the time of investing but even after the investments are done. As a result, investors could take timely actions if they see a drastic shift in the risk-o-meter of the respective mutual fund scheme vis-a-vis their personal risk profile.

That being said, the decision to buy, hold or sell should not be taken solely look at lone the risk-o-meter. A Host quantitative as well as qualitative aspects of the scheme under consideration need to be evaluated, plus your own investment objective, risk appetite, financial goals you are addressing, and time to achieve the envisioned financial goals.

If you wish to select worthy mutual fund schemes, consider subscribing to PersonalFN’s unbiased premium research service, FundSelect. Each fund recommended under FundSelect goes through our stringent process, where they are tested on both quantitative as well as qualitative parameters.

Every month, PersonalFN’s FundSelect service will provide you with insightful and practical guidance on equity mutual funds and debt schemes – the ones to Buy, Hold, or Sell. Click here to subscribe to PersonalFN’s FundSelect service.

Dividend options to become more transparent

The capital market regulator, through a separate circular (dated October 5, 2020) has also asked mutual fund houses to offer more clarity to investors on the dividend option. Based on the recommendations of SEBI’s Mutual Funds Advisory Committee (MFAC), with effect from April 1, 2021, mutual funds will have to rename the dividend option under:

| Option / Plan | Name |

| Dividend Payout | Payout of Income Distribution cum capital withdrawal option |

| Dividend Re-investment | Reinvestment of Income Distribution cum capital withdrawal option |

| Dividend Transfer Plan | Transfer of Income Distribution cum capital withdrawal plan |

(Source: SEBI/HO/IMD/DF3/CIR/P/2020/194)

A need to communicate more clearly under the dividend option of a Mutual Fund Scheme was found my SEBI’s MFAC.

At present, mutual fund schemes can distribute dividends from the realized profits of the scheme which are kept in the ‘Equalization Reserve Account’.

The regulator has directed all mutual funds to disclose the amount that can be distributed out of equalization reserve which represents realized gains in their offer documents.

Plus, fund houses shall disclose this information to investors at the time of investing in such options.

The regulator also wants mutual funds to maintain clear segregation between income distribution (appreciation on NAV) and Capital Distribution (Equalization Reserve) in the consolidated account statement provided to investors.

Investors must keep in mind that fund houses can’t guarantee future dividend payments. The new guidelines in this regard will compel asset management companies to become more transparent about their dividend policies with mutual fund investors. We can hope that mis-selling in the name of high dividend payments will stop.

Looking at the recent regulatory changes, it appears that the capital market regulator may take even harsher steps if required. At present, how mutual funds respond to these changes, remains interesting to watch out for now.

This article first appeared on PersonalFN here

{kind=link}