The year 2024 is going to be an eventful one. We have geopolitical tensions simmering (owing to tensions in the Middle East, there are attacks on vessels in the Red Sea by Houthis, the relations between the U.S. and China seem strained, China’s military activity in the South China Sea — to sort of threaten Taiwan, tensions brewing between North Korea and South Korea, and the ongoing Russia-Ukraine war.

Plus, there is a possibility of geoeconomic fragmentation, several economies are at risk due to global supply chain, international crude oil prices are rising, food price uncertainties continue to weigh on the inflation outlook, central banks would possibly pushing bank policy interest rate cuts and it would potentially weighing down on global economic growth, volatility in the financial market has increased, and there are general elections in numerous countries, including India and the U.S.

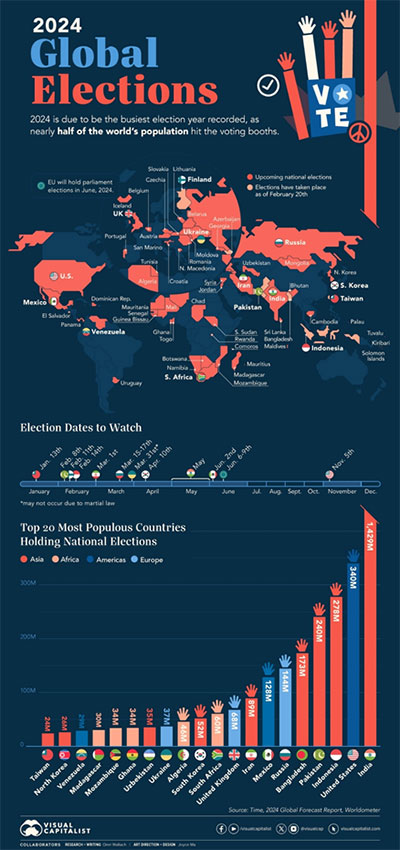

(Source: https://www.visualcapitalist.com)

Speaking of India, while the broader consensus seems that the Modi-led-NDA government would return to power again (Modi 3.0); the price rise, unemployment, alleged corruption and crony capitalism could set in anti-incumbency.

If the Modi-led-NDA does not get a clear mandate as they did in the previous two general elections, India’s financial markets, particularly equities (a high-risk asset class), could see heightened volatility and may correct in the short-to-near term (similar to what happened in 2004 when, despite the India-shining sloganeering, the Vajpayee-led-NDA government was voted out and Congress-led-UPA was back in power).

Against the aforementioned backdrop where there are headwinds in play, it would be worthwhile considering Multi-Asset Allocation Funds now from a strategic or tactical asset allocation standpoint. This shall help reduce the risk.

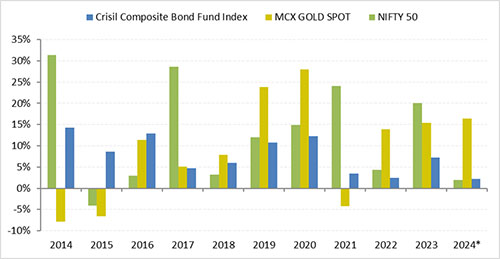

The graph below reveals that not all asset classes move in the same direction always. In times when equities have disappointed investors — as they did in the calendar years 2015, 2016, 2018, and 2022 — it is usually debt and gold that fare well.

Graph: Performance Of Equity, Debt, and Gold in the Respective Calendar Years

Data as of April 19, 2024

(Source: ACE MF; PersonalFN Research)

The point is that there is no consistent winning asset class; markets are cyclical (full of ups and downs). Hence, asset allocation, as you know, is a cornerstone of investing.

A Multi-Asset Allocation Fund is a meaningful choice to have tactical exposure to the three key asset classes — equity, debt, and gold — with a single fund. Multi-Asset Allocation Fund is a hybrid fund that is mandated to invest in at least three asset classes with a minimum allocation of at least 10% in each.

Its investment objective is to generate modest capital appreciation while trying to reduce overall risk to the portfolio from a combined portfolio of low-correlated assets.

While history reveals that equities hold the potential to build wealth and beat inflation over the long term, in the short term-to-near term, it could be subject to drawdowns owing to various factors or headwinds in play.

This is where debt as an asset class offers stability to your investment portfolio. At a time when interest rates are near the peak, and bond yields at the longer end of the maturity are attractive, it makes sense to have exposure to debt and other fixed-income instruments (such as bank FDs and small saving schemes).

As regards gold, it would continue to prove its trait of a safe have and command a store of value while there are geopolitical tensions and macroeconomic uncertainties. Recognising the risks involved, gold currently has scaled new highs. The precious yellow metal is proving to be an effective portfolio diversifier. Central banks, too, as part of their reserve and risk management are buying gold.

The fund managers of a Multi-Asset Allocation Fund, ascertaining the risks and opportunities, shall decide the positioning of these three asset classes taken into consideration:

- Macroeconomic factors prevailing in India and globally

- Valuations in the equity markets

- Interest rate outlook

- Outlook for gold

- Fundamental attributes of the securities

So, the fund manager of a Multi-Asset Allocation Fund has much leeway in building a suitable portfolio based on the market conditions.

That being said, there is price risk, credit risk, interest rate risk, and allocation risk when investing. But given that allocation to equity, debt, and gold is dynamic (not static), and that these three asset classes usually have a low positive correlation, the risk is kind of balanced. In bear market phases, Multi Asset Allocation Funds have arrested the downside risk better than Aggressive Hybrid Funds and Large Cap Funds.

Who Should Invest?

If you have a moderately high-risk appetite, a medium-to-long-term investment horizon, i.e. around 3 to 5 years, and want to balance risk by investing in equity, debt, and gold, consider investing in some of the best Multi-Asset Allocation Funds. You could earn moderate-to-high returns (by way of long-term capital appreciation and current income). Over the last 3 years and 5 years, the compounded annualised category average returns of Multi-Asset Allocation Funds are 18.7% and 15.5%, respectively (as of April 19, 2024).

Watch this video to know which are the 3 Best Multi-Asset Allocation Funds:

Holding a Multi-Asset Allocation Fund would save you the hassle of timing and market monitoring, portfolio rebalancing at your end, and, yet capitalise on the opportunities in the respective asset classes, as well as prove to be cost-effective and tax efficient.

Tax Implications of Investing in Multi-Asset Allocation Funds

The tax implications of investing in a Multi-Asset Allocation Fund shall depend on its allocation to domestic equities.

If a Multi-Asset Allocation Fund maintains an exposure of a minimum of 65% in domestic equities over the past 12 months, then the scheme is taxed like an equity fund; otherwise, it is taxed like a debt-oriented fund.

| Domestic Equity Exposure | Short Term Capital Gains | Long Term Capital Gains |

| Up to 35% | As per the investor's tax slab | As per the investor's tax slab |

| Between 35-65% | As per the investor's tax slab | For a holding period of more than three years, taxed at 20% with indexation benefit |

| Above 65% | Taxed at 15% | For a holding period of more than one year, taxed at 10% (if the gains are above Rs 1 lakh) |

Thus, when you are considering a Multi-Asset Allocation Fund, don’t forget to check whether its portfolio is skewed toward equities or debt.

Be an informed and thoughtful investor. And when in doubt, consult a SEBI-registered investment advisor.

Happy Investing!

This article first appeared on PersonalFN here

{kind=link}