The geopolitical tensions in the Middle East are exacerbating. Within a fortnight after Israel’s suspected strike on Iran’s embassy in Damascus (Syria’s capital) — in which seven of Iran’s military advisers and three senior commanders were killed — Iran has avenged this attack with more than 300 projectiles (including 170 drones and around 120 ballistic missiles) launched into Israel air space.

While Israel has reported only modest damage, as a large majority of these projectiles were downed by Israeli fighter jets, and the U.S., Britain, and Jordan also came to the rescue, tensions have surely intensified. While the Iran Army has said it has “achieved all it is objectives” in the attack, according to made in “self-defence”, Israel’s member of the war cabinet, Benny Gantz, has said that they “will exact a price from Iran when the time is right.” So, in its “right to defend” and backed by the U.S., it appears that the Israeli war cabinet is in favour of hitting back. Tehran, meanwhile, has stated that it would again retaliate with great force if Israel with or without the support of U.S. military action strike back again.

This conflict could potentially build up into other regions of the Middle East, such as Iran, Lebanon, Iraq, Yemen, and Syria. Plus, escalations in the attacks in the Red Sea, may go on to disrupt trade and supply chains, lead to a rise in commodity prices, impact the disinflation process, and amplify the volatility in the financial markets.

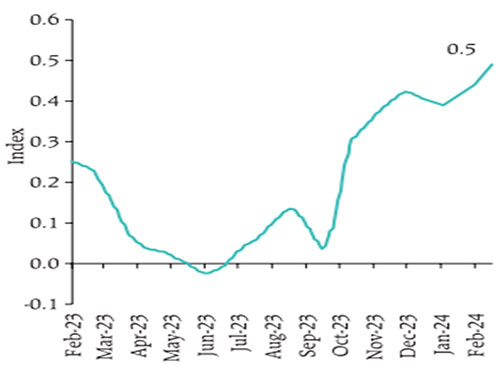

Graph: Geopolitical Risk Indicator

(Sources: Federal Reserve Bank of New York; BlackRock Investment Institute, February 2024; and Bloomberg, as per RBI’s March 2024 Bulletin)

Being cognizant of the geopolitical landscape, the Reserve Bank of India (RBI) has also observed that the spillovers from geopolitical hostilities, rising geoeconomic fragmentation, disruptions in the Red Sea, volatile global financial markets and climate shocks are the key risks to the growth and inflation outlook.

The global BlackRock Geopolitical Risk Indicator (BGRI), which aims to capture the overall market attention to the looming geopolitical risks, is also at a high. Not just in the Middle East, tensions are brewing in the Korean peninsula, China is exhibiting its military prowess in the South China Sea to provoke Taiwan and the U.S., there are China-India scruffles at the border, the ongoing Russia-Ukraine war, and more.

In such a time, volatility in the financial market has increased. India’s Volatility Index or VIX, averaged around 14.6, the highest since the fourth quarter of CY 2022. In such times, you need to wisely de-risk your portfolio.

How to de-risk your mutual fund portfolio amidst the looming geopolitical tensions?

Well, here’s what you need to do…

-

Ensure Optimal Diversification – Diversification is the basic tenet of investing. It spreads the investment risk and potentially reaps investment success. That said, care should be taken to make sure that the portfolio is optimally diversified – neither more nor less.

When you are looking at the diversification aspect of your portfolio, first, it needs to be done as per asset allocation most suited for you (taking into consideration your age, risk appetite, broader investment objective, the financial goals you are addressing, and the time in hand to achieve those envisioned financial goals). Based on that, you need to have a suitable allocation to three key asset classes: equity, debt, and gold.

Avoid going gung-ho and investing only in equities. In times like these, when equities face downside risk, it is debt that would add stability to your portfolio, while gold would play the role of portfolio diversifier, a safe haven, and command a store of value in times of economic uncertainties. In fact, weighing the risks, gold in India has already run up and breached the Rs 71,000/10 gram levels.

[Read: Why Gold Is Scaling New Highs]

Besides diversification by asset allocation, which ensures that all your eggs aren’t in one basket, care needs to be taken to diversify the portfolio within the respective asset class. For instance, when you take exposure to equities, diversify across stocks and equity mutual funds.

Make sure the equity composition of the portfolio is across large-cap, mid-cap, small-cap, and micro-caps to de-risk your portfolio, rather than skewing the portfolio to one market cap segment. In times like these, holding a significant part of your equity holdings to small-caps and mid-caps would imperil the portfolio with the risk amplified. Hence, make sure to hold a balanced multi-cap portfolio.

Also, when investing in mutual funds, diversify across houses to reduce the concentration risk, rather than showing a penchant for one fund house or going with only bigger fund houses. Keep in mind that, how big the fund house is in terms of the AUM, does not matter. What surely does is whether it’s a prudent asset manager or a mere asset gatherer. If the fund has not been delivering on its stated investment objective and is underperforming, you should be careful.

Moreover, from a diversification standpoint, invest in mutual funds across the styles and sub-categories (within the respective category). This is because not all types or sub-categories of funds would fare well always. Thus, hold dissimilar mutual funds in your portfolio. If you hold too many similar mutual funds, it can also drag your portfolio returns.

At present, in the case of equity funds, it is value and Large Cap Funds and/or Multi Cap Funds that could be worthwhile in terms of stability rather than the very-high-risk Small Cap Funds and Mid Cap Funds.

Similarly, as interest rates are almost near the peak, holding longer-duration debt mutual funds with a medium-term view of 3 to 5 years could help you benefit from higher yield and unlock capital growth. You may also invest in bank FDs now before interest rates begin to fall.

As regards geographical diversification of the portfolio, you may do so, provided you are well-versed with the investment opportunities available in the global landscape that could de-risk the portfolio and when your domestic portfolio is well-diversified.

[Read: How to Choose Mutual Funds For Your Investment Portfolio]

-

Timely Portfolio Rebalancing – Your effort of portfolio diversification could come to a zilch if timely and disciplined portfolio rebalancing is not followed. Rebalancing, as the name suggests, involves realigning the portfolio to your best-suited asset allocation. With changes in market conditions, your original allocation to three key asset classes — equity, debt, and gold — also increases or decreases.

At present, as the Indian equity market has scaled new highs, it is possible the equity allocation may have skewed much more than what’s apt for you. To de-risk and optimise returns (i.e. strike a balance between the risk and reward), portfolio rebalancing may be warranted; it is integral to the art of investment management.

Alternatively, you could also make changes in the intra-asset allocation. For example, in your equity allocation, if you are high on Small Cap Funds (which carry very high risk), consider trimming it and prefer Large Cap Funds that are expected to offer stable returns and steady growth in the long run with lesser risk and are relatively better placed on valuations. To play the opportunities across the other market segments — the small-caps and mid-caps – you may go with some of the best Flexi Cap Funds or Multi Cap Funds.

Given that portfolio rebalancing can be a tricky exercise (as you also need to account for the transaction cost and the tax implications), seeking the help of a SEBI-registered investment advisor may be worthwhile. The advisor considering your current age, evolving risk tolerance, changing financial circumstances, financial goals, and the time to achieve the envisioned goals would recommend appropriate portfolio rebalancing so that you own an appropriate mix of assets.

-

Embrace Rupee-cost Averaging – Say you are addressing long-term financial goals, and your risk appetite warrants higher allocation to equities, it makes sense to stagger your lump sum investments or, even better, take the Systematic Investment Plan (SIP) route. The inherent rupee-cost averaging feature of SIPs would mitigate the risk involved in the interim and compound wealth over the long term. If you have ongoing SIPs in some of the best mutual funds, do not make the mistake of pausing or stopping SIPs in panic, as it would put brakes on the process of power of compounding and push back from accomplishing the envisioned financial goals.

-

Make sure you have a sufficient Emergency Fund – While you may be diligently saving and investing your hard-earn for your envisioned financial goals, safeguard yourself by holding a respectable sum — around 12 to 18 months of regular monthly expenses (including EMIs on loans) — in a Liquid Fund (and/or a bank FD) apart from insurance. Liquid Funds are a smart bet during uncertain times; they are far less volatile than other debt funds, highly liquid, and may preserve the purchasing power of your hard-earned money. Money invested therein could help you in times of crisis — say you lose your job, a medical emergency in the family, and so on.

[Read: 3 Best Liquid Funds for 2024]

“Successful investing is about managing risk, not avoiding it.” – Benjamin Graham (the father of value investing and the author of the widely acclaimed book, ‘The Intelligent Investor’).

Graham further opines, “The essence of investment management is the management of risks, not the management of returns.”

Thus, invest sensibly – do not just chase high returns. Only tracking the returns of a mutual fund scheme is stupid; it may be detrimental to your health and wealth. Keep in mind that for every level of risk you seek there is risk. Thus, set your risk-return expectations right.

If you are unsure about the quality of your mutual fund portfolio, get your mutual fund portfolio reviewed by an investment expert who backs recommendations with thorough research on mutual funds. A timely portfolio review can help you identify whether you over-weight or under-weight to a respective asset class, how concentrated the portfolio is to a particular fund house, a market capitalisation segment (large-cap, mid-cap and small-cap), understand the risk you are exposed to, and take timely actions (buy, hold, or sell) with the changing circumstances, risk perceptions, your financial goals, and time to achieve those goals.

Be a thoughtful investor, be mindful of the risk, and take apt measures to de-risk your portfolio.

Happy Investing!

This article first appeared on PersonalFN here

{kind=link}