The capital market regulator, SEBI, in mid-March 2024, warned of froth building in small cap and mid cap segments of the Indian equity market. It appears that most mutual fund investors have taken this guidance seriously.

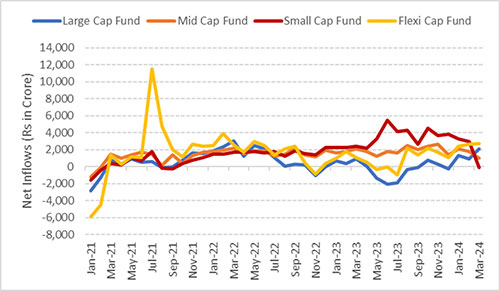

The Association of Mutual Funds in India (AMFI) data revealed that for the first time since September 2021, Small Cap Funds reported net outflows in March 2024 to the tune of Rs 94.17 crore. Investors preferred to redeem or book profit after making some handsome gains in this sub-category in the last couple of years.

Even in the Mid Cap Funds, net inflow slowed down to Rs 1,017.69 crore in March 2024 versus Rs 1,808.18 crore in the previous month.

This shows the caution adopted by most investors in these market cap segments, where the valuations seem even more expensive than large caps.

Moreover, AMFI in collaboration with the regulator issued stress test guidelines for Small Cap Funds and Mid Cap Funds, with liquidity being one of the important criteria, also weighed on investor sentiment.

[Read: Liquidity Check – Is Your Small Cap Fund Under Pressure?]

Some fund houses also paused lump sum inflows into their Small Cap Funds, while some allowed Systematic Investment Plans (SIPs) and Systematic Transfer Plans (STPs) for investments.

Graph: Investors Turning Watchful of Investing in Small Cap Funds

(Source: ACE MF, data collated by PersonalFN Research)

In such a scenario, Large Cap Funds reported noticeably higher net inflow in March 2024, worth Rs 2,127.79 crore compared to Rs 921.14 crore in the previous month.

Similarly, the net inflows into Flexi Cap Funds increased to Rs 2,738.11 crore in March 2024 from Rs 2613.23 crore in the previous month.

Investors perhaps recognised the fact that large caps offer stable returns and steady growth in the long run with lesser risk (than mid caps and small caps) and are relatively better placed on valuations.

Also, investors wanting to benefit from wealth creation across market cap segments and diversify their portfolio, chose to invest in Flexi Cap Funds recognising that these funds have the flexibility to increase/decrease exposure to a particular segment depending on market conditions, liquidity conditions, and valuations.

[Read: 4 Best Flexi Cap Funds for 2024]

The entire equity funds category (comprising of 11 sub-categories) also reported 16% less net inflow worth Rs 22,633.15 crore in March 2024 owing to end-of-the-financial year redemptions and re-allocations, showed the AMFI data.

Why You Should Not Panic and Sell Equity Funds

India is one of the fastest-growing major economies of the world (“a bright spot”) in the global economy, with a demographic dividend and pushing structural reforms. Investors, by and large, seem positive about the wealth-creation prospects of Indian equities.

The corporate earnings of Indian Inc. in the last couple of years have been rather encouraging, abetted by macroeconomic conditions and demand. The corporate profit upcycle is in progress — we are witnessing more earning upgrades than downgrades.

The profit share of India Inc. in GDP is roughly around 5% and is likely to expand in the following years abetted by the capex/investment cycle, credit growth, healthy banking system, stable tax policies, PLI, and structural improvement in demand.

Recognising the wealth creation potential Indian equities have to offer, India’s market capitalisation-to-GDP ratio, famously called the Buffett indicator (named after legendary investor Warren Buffett), is also in the ‘fairly valued’ zone.

That being said, if markets rise further and corporate earnings do not keep pace, then it would be pointless getting carried away by irrational exuberance. In such a case, markets may seem overvalued.

How to Approach Equity Mutual Funds Now?

I suggest following a sensible asset allocation, considering your age, risk profile, broader investment objective, the financial goal/s you are addressing, and the time in hand to achieve those envisioned goals. Avoid investing in an ad hoc manner and mindlessly going gung ho.

In the current market, where valuations of mid caps and small caps are relatively more expensive than large caps, and since the Small Cap Index-to-Sensex ratio is above 0.6 vis-a-vis the long-term median of 0.4, avoid going overweight or skewing your investment portfolio, particularly to Small Cap Funds.

Follow a ‘Core & Satellite’ approach — an investment strategy followed by some of the most successful equity investors around the world.

The term ‘Core’ refers to more stable and long-term holdings. Typically, these should be around 65%-70% of the equity mutual fund portfolio and comprise some of the best Large Cap Funds, Flexi Cap Funds/Multi-cap Funds, and Value/Contra Funds. They could help potentially multiply your wealth with stability but make you keep an investment horizon of at least 5 years.

The term ‘Satellite’ refers to the strategic portion that would help push up the overall returns of the portfolio with relatively high risk. This portion of the portfolio could comprise around 30%-35% of the equity portion and a couple of best Mid-cap Funds (max 2), and if you have a very high-risk appetite, then one of the best Small Cap Funds. That said, you need to keep a longer time horizon of 7 to 8 years for Satellite holdings to alleviate the downside risk if the broader markets correct in the near term (due to the macroeconomic and geopolitical uncertainty in play).

By wisely structuring your mutual fund portfolio (based on your age, risk profile, broader investing objective, the financial goal/s you are addressing, and investment time horizon), you would set the path to wealth creation.

The overall returns on the equity mutual fund portfolio you clock would hinge on your asset allocation best suited for you, the type of schemes held and the performance of their underlying portfolios.

Take care to ensure that your portfolio is well-diversified in the year 2024 and beyond.

When in doubt, speak to a SEBI-registered investment advisor.

Happy Investing!

This article first appeared on PersonalFN here

{kind=link}