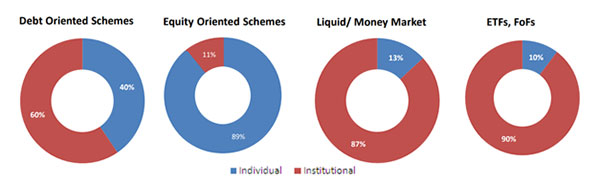

Ever since the launch of the ‘Mutual Funds Sahi Hai’ campaign by AMFI in March 2017, the interest of individual investors — retail and High Net worth Individuals — has been on the rise. As of September 30, 2023, individual investors hold a relatively higher share (58.8%) of the industry assets. The inflows have been mainly led by individual investors, both retail and HNIs, in the endeavour to clock a better return than parking money in some of the traditional investment avenues. A dominant portion (89%) of equity AUM is held by individual investors.

Data as of September 30, 2023

(Source AMFI)

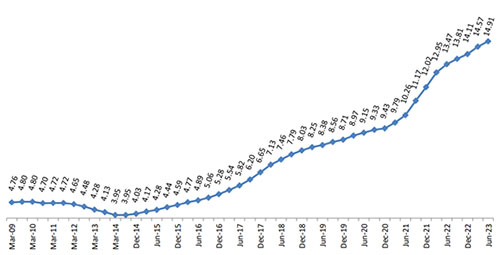

Interestingly, the inflows are also coming from the B-30 cities. As of September 2023, 26% of the assets (mainly in equity mutual funds), are from the B-30 cities. The folio count (also known as mutual fund accounts), as a result, has touched a record high. Systematic Investment Plans (SIPs) are driving the inflows and the AUM up.

Graph 2: Steady Rise in Mutual Fund Folio

Data as of September 30, 2023

(Source AMFI)

The Indian mutual fund industry’s AUM-to-GDP ratio is currently around 15% versus 8-9% a few years ago. Although this is much less than some of the developed economies, there has been a remarkable uptick, and it will continue to expand in the coming years.

However, at present, against the backdrop of looming uncertainty around the world, investors are asking: Is it the right time to invest in mutual funds?

Well, to those of you who have this question, let me first make clear that you cannot approach mutual funds with the mindset of a trader. So, stop looking at the daily NAVs of mutual funds.

[Read: Why Looking at the NAV of Mutual Funds to Create a Winning Portfolio is Futile]

With a trading mindset, you may end up, ignoring or dumping well-performing mutual funds — that have appealing and consistent performance track records, commendable portfolio characteristics, and follow robust investment processes & systems — and instead, maybe opting not so worthy schemes at low NAV. This could prove perilous for your portfolio and long-term financial well-being.

You see, mutual funds are for investment purposes, to plan for accomplishing your envisioned financial goals. So, keep away from trading in mutual funds. What is important is ‘time in the market’ and not timing the market (which could prove hazardous to your wealth and health).

Yes, at present, the volatility in the equity markets around the world has intensified. This is owing to the following factors in play…

- The Israel-Gaza War …and the possibility of it widening with many other Middle East and non-Middle East nations as Israel has prepared for a ground invasion to annihilate Hamas.

- Geopolitical tensions are simmering among other countries, i.e., between the U.S. and China, Taiwan and China, India and China, Pakistan and India, North Korea and South Korea, among others.

- The risk of geoeconomic fragmentation is emerging as a serious threat to the macro-financial stability, as warned by the IMF.

- The chance of international oil prices moving up owing to tensions in the Middle East are high.

- There is a risk to the inflation trajectory owing to supply chain disruptions.

- Possibility of a Super El Nino next year (as warned by the U.S. weather agency) pushing up food prices.

- Central banks are indicating that policy interest rates could stay high to control inflation (without offering a clear signal when the rates would begin to soften).

- A possibility that the global economy may slow down later this year (or early 2024).

- Higher borrowing costs, endangering the recovery of bank loans in case of an economic slowdown and leaving them with insufficient capital buffer.

- The burgeoning debt-to-GDP ratio of many major economies – higher than the pre-pandemic levels.

The fact also is, Indian equity markets are trading at a premium compared to their global peers.

The Morgan Stanley Capital International (MSCI) India Index Price-to-Equity (P/E/) ratio is currently around 26x, while the MSCI Emerging Markets Index and MSCI World Index trail P/Es are at around 14x and 19x (as per the latest factsheets). Even on a 12-month forward P/E, India is commanding a premium vis-a-vis emerging markets and the world.

Having said that, the present correction since the peak is reducing or moderating the valuation premium, and is healthy. Use it as an opportunity to sensibly build your equity mutual fund portfolio.

“Successful investing is about managing risk, not avoiding it.” – Benjamin Graham, the father of value investing

Uncertainty is part of life and market-linked investments.

The history of the Indian equity market stands testimony to the fact that despite the negative events, Scam 1992, the downturn of 2002, the global financial crisis of 2008-09, the Dubai debt debacle of 2009-10, the debt crisis in Greece, the slowdown in China in 2016, the COVID-19 crash in March 2020, Russia’s invasion of Ukraine, and many such events; the Indian equity markets have trounced and performed well (over the long run).

Currently, India is perceived to be a ‘bright spot’ in the global economy with several reforms being rolled out. The focus is on infrastructure development and technology, which can catalyze growth. Both public and private investment is picking up. Despite the slowdown in certain parts of the world, demand in India is buoyant thanks to the strong consumption story. In the last few years, many listed (and unlisted) companies have announced encouraging earnings, enabling both, domestic and foreign portfolio investors, to exude confidence in India as an investment destination.

If your broader investment objective is capital appreciation, have a high-risk appetite, vital financial long-term financial goals to achieve, want to clock respectable returns, and have a time horizon of at least 5 years, continue to invest in the best diversified equity funds in line with your asset allocation model. The diversified equity schemes would help you gain exposure across market capitalisations and themes.

[Read: How to Choose Mutual Funds For Your Investment Portfolio]

Also, watch this video:

The Strategy to Follow to Invest in Equity Mutual Funds

I recommend that you follow the Core and Satellite approach, a time-tested investment strategy followed by some of the most successful equity investors around the world.

The term ‘Core’ applies to the more stable, long-term holdings of the portfolio, while the term ‘Satellite’ applies to the strategic portion that would help push up the overall returns of the portfolio across market conditions.

Ideally, your ‘Core’ holdings of the equity portfolio should comprise around 65-70% of your equity mutual fund portfolio and comprise a Large-cap Fund, Flexi-cap Fund, and a Value Fund/Contra Fund.

The ‘Satellite’ holdings of the portfolio, on the other hand, can be around 30-35%, comprising a Mid-cap Fund, a Large & Mid-cap Fund, and an Aggressive Hybrid Fund.

When you construct a Core & Satellite portfolio of equity mutual funds, make sure you do not end up over-diversifying the portfolio. Select no more than 7 to 8 best equity schemes.

It would be best to ensure that no more than two equity mutual fund schemes belonging to the same fund house are included in the portfolio.

Also, no more than two schemes in the portfolio should be managed by the same fund manager, all the schemes should have a strong track record of at least five years, they have outperformed over at least three market cycles, are among the top performers in their respective categories, and are abiding by the stated objectives, indicated asset allocation, and investment style.

By wisely structuring and timely reviewing the Core and Satellite holdings, you would be able to add stability to the portfolio and prove to be a wealth multiplier in the long run.

Also, Consider Multi-Asset Funds

A Multi-Asset Fund would prove to be a meaningful choice to tactically allocate across assets such as equity, debt, and gold. A Multi-Asset Fund is mandated to invest at least 10% each in these asset classes.

The allocation between equity, debt, and gold is usually dynamic (meaning it changes) and is backed by the fund management teams’ outlook for the respective asset class. This can help protect your portfolio.

[Read: How a Multi-Asset Fund Can Protect Your Portfolio]

Should You Invest Lump Sum or do SIPs?

Given that volatility is likely to intensify, it makes sense to take the SIP route to invest in equity-oriented and aggressive hybrid funds. The inherent rupee-cost averaging feature of SIPs shall help mitigate the volatility, make timing the market irrelevant, and help remain focused.

If the market descends, you will buy more number of units, if it ascends you will be buying a lesser number of units and yet continue to grow wealth thus enabling you to accomplish your envisioned financial goals.

If you are already SIP-ping in some of the best mutual fund schemes out there, do not make the mistake of stopping or discontinuing your SIPs petrified by the market volatility. It could put brakes on the power of compounding and then accomplishing important financial goals and then achieving the envisioned goal may be a challenge.

Hold Emergency Money in a Saving Bank Account or a Liquid Fund

Given the geopolitical and economic uncertainty looming and the chances of further correction in equities cannot be ruled out, I suggest holding 12 to 18 months of regular monthly expenses (including EMIs on loan) in a savings bank account and/or a Liquid Fund. This shall help you be prepared for the worst while you hope for the best and ensure that you do not liquidate worthy investments made to accomplish your envisioned financial goals.

Also, allocate around 10-15% of your entire portfolio to gold. It would prove to be an effective diversifier for your portfolio and a safe haven amid uncertainties.

To build wealth, all you need is to follow a thoughtful, prudent approach and shut off from the noise.

Happy Investing!

This article first appeared on PersonalFN here

{kind=link}