As one of the fastest-growing economies in the world and with the steady rise of the Indian equity market, India has attracted the attention of many individuals who have settled abroad for career opportunities. Mutual funds are one of the most sought-after options for investments by NRIs.

However, the question arises here is whether NRIs can invest in mutual funds in India?

The answer is yes; NRIs are indeed allowed to invest in mutual funds.

According to a general permission by the Reserve Bank of India under Schedule 5 of the Foreign Exchange Management (Transfer or Issue of Security by a Person Resident Outside India) Regulations, 2000, Non Resident Indians (NRIs) , Persons of India Origin (PIO) residing abroad, Foreign Institutional Investors (FIIs) have been granted permission for investing in / redeeming units of the mutual funds.

In simple words, NRIs can invest in mutual funds provided they adhere to the provisions of the Foreign Exchange Management Act (FEMA).

An individual is classified as an NRI if they fulfil the following criteria:

- He/she is an Indian citizen residing abroad.

- He/she was physically present in India for less than 120 days in a financial year (April – March). This 120-day rule will apply only if the individual’s taxable income in India exceeds Rs 15 lakh in a financial year.

- If an individual’s income in India is below Rs 15 lakh, then the physical stay in India can be extended to 181 days without affecting the NRI status for taxation purposes.

What is the process NRIs need to follow to invest in mutual funds in India?

Since mutual funds in India cannot accept investments in foreign currency, there are certain procedures that NRIs need to follow before they can begin their investment journey. Here is how it can be done:

1. Complete the KYC

Just like in the case of resident investors, completion of the KYC process is mandatory for NRI investors as well before starting investments in mutual funds. Investors are required to submit the necessary documents along with the KYC registration form to KYC Registration Agencies (KRAs) such as CAMS and KFintech.

Such applicants must furnish a certified copy of proof of their identity (their PAN), passport size photograph, cancelled cheque leaf of NRE/NRO account, and copy of passport (relevant pages as specified by the mutual fund house). They also need to submit a copy of their overseas/local address proof (as applicable) certified by a local authority/Indian embassy/consulate is required. If documents are not in the English language, they must be translated into English.

In the case of NRIs, the in-person verification can be completed through authorised officials of overseas branches of Scheduled Commercial Banks registered in India, Notary Public, Court Magistrate, Judge, or Indian Embassy / Consulate General in the country where the client resides.

Investors have to go through the KYC process only once, i.e. NRIs do not need to submit the KYC form for every investment once the KYC process is complete.

It is important to note that many mutual fund houses in India do not permit investments from NRIs residing in the USA and Canada due to the stringent compliance procedures laid down under the FATCA (Foreign Account Tax Compliance Act).

Very few mutual fund houses, such as the ones listed below, allow investors from the USA and Canada to invest in their schemes:

- Aditya Birla Sun Life Mutual Fund

- HDFC Mutual Fund

- SBI Mutual Fund

- UTI Mutual Fund

- ICICI Prudential Mutual Fund

- PPFAS Mutual Fund

- Nippon India Mutual Fund

It is noteworthy that NRIs from the USA or Canada may be required to submit additional documents as well as declarations before they can begin their investment journey. Accordingly, it is important to refer to the scheme-related documents.

2. Open an NRO/NRE account

NRIs looking to invest in mutual funds in India cannot do so through a regular savings bank account. For this purpose, they need to open an NRO (Non Resident Ordinary) or NRE (Non Resident External) account.

An NRE account enables NRIs to park their foreign earnings, whereas an NRO account enables them to manage income earned in India.

The NRE Account is suitable for those who want to deposit/invest their overseas earnings in India. The earnings from Indian investments, such as mutual funds, can also be repatriated to a bank account abroad.

On the other hand, the NRO account is suitable for managing earnings/savings derived from India. NRO is a Rupee-based account and money cannot be repatriated to a foreign currency easily.

Do keep in mind that once an individual starts investing in a mutual fund scheme via an NRE/NRO account, they need to stick to the same account type for that investment in that scheme (folio).

[Read: 3 Types of Bank Accounts an NRI Can Open in India]

3. Select the mode of investment

Once the NRE/NRO account is activated, an NRI can invest in mutual funds either directly or through an authorised person.

NRIs can choose to manage their mutual fund investments on their own. In such a case, they can start investing in mutual funds directly (on their own) through normal banking channels.

They may also choose to designate someone to transact and manage the investment on their behalf. In other words, investors can issue a Power of Attorney (PoA). Both the investor and the registered PoA holder must be KYC-compliant. Investors can authorise a resident Indian to be the PoA holder.

The PoA holder has the authority to invest on behalf of the NRI investor and sign documents for initial and additional purchases and redemption transactions.

How NRIs can redeem their mutual fund units

In order to redeem the mutual fund units, the NRI investors need to submit the redemption request form at the nearest Investor Service Centres of AMCs/RTAs (such as CAMS/KFintech). Redemption requests can also be processed online through the respective websites of the AMCs/RTAs. The redemption request forms should contain the investor’s folio number and the amount/units to be redeemed, and should be duly signed by the investors or the PoA holders.

Redemption proceeds are made in favour of the first investor. Moreover, the redemption proceeds and/or dividend or income earned (if any) will be payable in Indian Rupees only. Mutual Funds are not liable for any loss on account of fluctuations in exchange rate while converting the Rupee into the US dollar or any other currency.

The AMC will credit the redemption proceeds (investment + gains) to the registered NRE/NRO bank account of the investor after deducting applicable taxes.

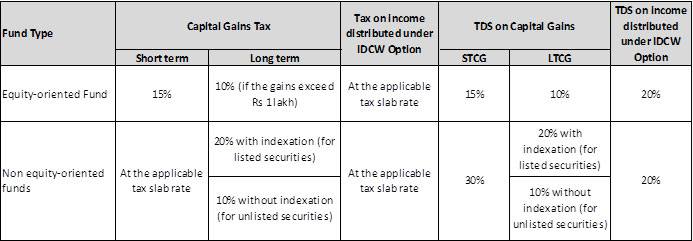

What are the tax implications of mutual fund investments for NRIs

In the case of equity-oriented mutual funds, profits earned from the sale of a mutual fund with a holding period of one year or less are termed as Short-term Capital Gains. Profits earned from the sale of a mutual fund with a holding period of more than one year are termed as Long-term Capital Gains.

In the case of non-equity-oriented mutual funds, profits earned from the sale of a mutual fund with a holding period of 36 months or less are termed as Short-term Capital Gains. Profits earned from the sale of a mutual fund with a holding period of more than 36 months are termed as Long-term Capital Gains.

Furthermore, on redemption of mutual fund units, the tax will be deducted at the source (TDS) on the capital gains made on the investment. The specific TDS rate to be deducted is determined by the type of scheme (equity or non-equity) as well as the holding period of the investment.

Tax applicable to NRIs on mutual fund investment

(Source: AMFI)

Do note that income earned in India may also attract taxation in their resident country. To prevent the instance of investors having to pay double taxes on incomes arising in one country to a tax resident of another nation, India has signed the Double Taxation Avoidance Treaty (DTAA) with around 90 countries.

Thus, under the DTAA, NRIs can claim tax credits in India on the earnings from their mutual fund units, provided India has signed such an agreement with the resident country of the investor.

The Bottom Line

NRIs can easily invest in mutual funds in India, provided they comply with the necessary KYC and other regulations. Through mutual fund investments, they can potentially build a respectable corpus for their future financial goals or meet the requirements for their dependents in India.

However, they should ensure that they select the right schemes for their financial needs based on their investment objective, risk profile, and investment horizon.

This article first appeared on PersonalFN here

{kind=link}