The Reserve Bank of India (RBI) , for the fourth successive time, has kept the policy repo rate under the Liquidity Adjustment Facility (LAF) unchanged at 6.50% in its October 2023 bi-monthly monetary policy 2023-24 meeting.

On October 06, 2023, the RBI Governor Shaktikanta Das-led Monetary Policy Committee (MPC) maintained the status quo on repo rates and stance. The MPC decided unanimously to keep the policy repo rate unchanged at 6.50%.

All six members of the MPC – Dr Shashanka Bhide, Dr Ashima Goyal, Prof. Jayanth R. Varma, Dr Rajiv Ranjan, Dr Michael Debabrata Patra, and Shaktikanta Das voted in favour of this decision.

Consequently, the Standing Deposit Facility (SDF) rate remains at 6.25% and the Marginal Standing Facility (MSF) rate and the Bank Rate at 6.75%. The MPC also decided by a majority of 5 out of 6 members to remain focused on withdrawing accommodation to ensure that inflation progressively aligns with the target while supporting growth.

To know about RBI’s August 2023 bi-monthly monetary policy 2023-24 meeting, you may consider reading… RBI Keeps Policy Rates Unchanged Again! Here’s How to Approach Debt Mutual Funds Now

According to the RBI Governor, Mr Shaktikanta Das, the headline inflation in the first quarter of the current fiscal year was 4.6%. However, in the first quarter of FY 2022-23, it was 7.3%, and the repo rate has risen by 250 basis points (bps) since May 2022.

Table: RBI Monetary Policy Actions and Stance

| Month | Repo Policy Rate | Policy Action (Basis points) |

Monetary Policy Stance |

| Feb-2019 | 6.25% | -25 | Neutral |

| Apr-2019 | 6.00% | -25 | Neutral |

| Jun-2019 | 5.75% | -25 | Accommodative |

| Aug-2019 | 5.40% | -35 | Accommodative |

| Oct-2019 | 5.15% | -25 | Accommodative |

| Dec-2019 | 5.15% | Status quo | Accommodative |

| Feb-2020 | 5.15% | Status quo | Accommodative |

| Mar-2020 (an exceptional off-cycle meeting) | 4.40% | -75 | Accommodative |

| May-2020 (an exceptional 2nd off-cycle meeting) | 4.00% | -40 | Accommodative |

| Aug-2020 | 4.00% | Status quo | Accommodative |

| Oct-2020 | 4.00% | Status quo | Accommodative |

| Dec-2020 | 4.00% | Status quo | Accommodative |

| Feb-2020 | 4.00% | Status quo | Accommodative |

| April-2021 | 4.00% | Status quo | Accommodative |

| June-2021 | 4.00% | Status quo | Accommodative |

| Aug-2021 | 4.00% | Status quo | Accommodative |

| Oct-2021 | 4.00% | Status quo | Accommodative |

| Dec-2021 | 4.00% | Status quo | Accommodative |

| Feb-2022 | 4.00% | Status quo | Accommodative |

| Apr-2022 | 4.00% | Status quo | Accommodative |

| May-2022 (Off-cycle meeting) | 4.40% | +40 | Accommodative |

| June-2022 | 4.90% | +50 | Focus on withdrawal of Accommodative stance |

| Aug-2022 | 5.40% | +50 | Focus on withdrawal of Accommodative stance |

| Sep-2022 | 5.90% | +50 | Focus on withdrawal of Accommodative stance |

| Dec-2022 | 6.25% | +35 | Focus on withdrawal of Accommodative stance |

| Feb-2023 | 6.50% | +25 | Focus on withdrawal of Accommodative stance |

| Apr-2023 | 6.50% | Status quo | Focus on withdrawal of Accommodative stance |

| May-2023 | 6.50% | Status quo | Focus on withdrawal of Accommodative stance |

| Aug-2023 | 6.50% | Status quo | Focus on withdrawal of Accommodative stance |

| Oct-2023 | 6.50% | Status quo | Focus on withdrawal of Accommodative stance |

Data as of October 09, 2023

(Source: RBI Monetary Policy Statements, Data collated by PersonalFN Research)

Prior to making a rate cut decision, RBI tries to closely monitor domestic and global inflation trends. Market analysts expected the RBI to maintain rates and its current monetary stance in order to keep inflation under control. The latest MPC meeting confirmed the ‘status quo’ policy as predicted, reinforcing the importance of the 4% inflation target and robust macroeconomic indicators.

The Outlook for Inflation…

Global growth is losing momentum. Although inflation is easing gradually, major economies have been struggling to contain inflationary pressure on the economy. In contrast to past predictions, central banks are likely to keep raising interest rates to keep inflation under control.

On the strength of the recent drop in LPG prices and the correction in vegetable prices, the outlook for inflation in the near term is anticipated to improve. A number of variables, including a decrease in the area planted in pulses, a drop in reservoir levels, El Niño conditions, and unstable global energy and food prices, will influence the future trajectory.

The Reserve Bank’s enterprise survey reveals that manufacturing firms anticipate greater input cost pressures in Q3 compared to Q2 but marginally slower growth in selling prices. Infrastructure and service companies anticipate a slowing of price and input increases.

There has been a fall in kharif sowing, lower reservoir levels, and volatile global food and energy prices. Inflation surged in July and August 2023, driven by higher tomato and vegetable prices, while as expected it eased in the month of September.

The inflation forecast for FY 2023-24 was revised upward by 30 bps in light of the skewed south-west monsoon outturn, the growing likelihood of an El Niño event and the worsening global food prices outlook.

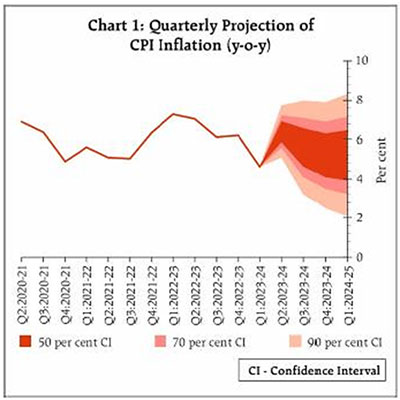

The governor has identified geopolitical tensions, a global economic slowdown, and an erratic monsoon as significant threats to India’s future economic growth. Taking these factors into account, CPI inflation is projected at 5.4% for 2023-24, with Q2 at 6.4%, Q3 at 5.6% and Q4 at 5.2%, with risks evenly balanced. CPI inflation for Q1 FY 2024-25 is projected at 5.2%.

Graph: RBI’s quarterly projection of CPI Inflation

Data as of October 09, 2023

(Source: RBI 4th bi-monthly Monetary Policy Statement 2023-24)

The baseline forecasts are subject to several upside and downside risks. The upside risks include persistent food price rises brought on by weather-related disruptions, which could feed inflation expectations, a further tightening of global commodity prices amid an increase in geopolitical tensions, and a greater pass-through of input cost pressures to output prices.

In the case of a dramatic slowdown in global GDP, an early resolution of geopolitical tensions, a steep correction in global crude and commodities prices, and additional supply improvement, downside risks could arise.

While core inflation appears to be slowing down and vegetable prices may experience additional declines, the MPC noted that headline inflation is above the tolerance zone and that its alignment with the target has been interrupted. As a result, the MPC will continue to be steadfast in its commitment to bringing inflation under control and stabilising inflation expectations.

However, if CPI inflation moves up and worries the RBI in future, the policy rate could go up later in the year by another 25-35 bps. Having said that, it appears that we are almost near the peak of the interest rate upcycle.

Global financial markets are becoming more volatile due to worries about rising rates for a longer period of time. The US currency has strengthened, sovereign bond yields have increased, and stock markets have corrected. The currencies of emerging market economies (EMEs) are depreciating, and capital flows are erratic.

The Monetary Policy Report for October 2023 states that although there was optimism about the tightening cycle coming to an early end during the months of April through July 2023, global equity markets later corrected due to predictions that policy rates would remain higher for longer.

Government bond yields decreased from their trough at the end of March 2023, but money market rates remained mostly range-bound. In the quarter ending September 2023, India’s 10-year G-sec yield traded practically flat and ranged between 7.06% and 7.25%.

Mutual fund experts stated that although the RBI has opted for a status quo policy, investors should proceed cautiously.

Repo rate status quo: Will debt mutual fund investments be affected?

Debt mutual fund schemes primarily invest in fixed-income instruments such as treasury bills, government securities, corporate bonds, and money market instruments. Returns from debt mutual funds are influenced by various factors including, interest rates, inflation, currency fluctuations, current account deficit etc.

Interest rates determine the price movement of the bonds and are inversely propotional to it. Any change in interest rates for that matter, leads to a subsequent change in the yield of the fixed income securities and also has an impact on the NAV of the debt mutual funds. The NAVs of the debt funds rise if the interest rates start to fall and vice versa.

[Read: Why You Should Hold Debt Mutual Funds in Your Portfolio]

However, the benchmark rate has inched up since the RBI mentioned in its bi-monthly monetary policy statement from October 2023 that it would sell government bonds through the Open Market Operation (OMO) mechanism to control systemic liquidity.

The yield differential between long-term bonds and the repo rate is anticipated to narrow as monetary policy becomes more stable. However, that is still largely dependent on how CPI inflation changes.

At the current juncture, it would be an opportune time to invest in longer-duration debt mutual funds with a medium-term view of 3 to 5 years so that you can take advantage of higher yields and unlock capital growth.

Moreover, it is prudent to make these investments gradually. Consider investing in shorter-maturity debt funds if you have a shorter investment horizon, as they are less affected by mark-to-market changes when interest rates rise.

Overnight Funds, Liquid Funds, Ultra Short Duration Funds, and/or Money Market Funds may be an option for investors who cannot afford to take a minor increase in risk or whose investment horizon is very short (a few days, weeks, or months).

Having said that, bear in mind debt funds often carry some risk; therefore, prioritise the stability of the investment capital over returns. Avoid making investments in debt funds that seek yield in order to increase returns.

Additionally, the capital gains on selling debt mutual fund units, regardless of whether they are short-term or long-term, will henceforth be taxed at the marginal rate of taxation or according to the taxpayer’s income-tax bracket. Don’t be discouraged, even debt mutual funds currently have an edge over bank fixed deposits in terms of returns.

[Read: Debt Mutual Funds are Now at Par with Fixed Deposits for Taxation]

To conclude…

While the RBI’s policy rate stability demonstrates its confidence in the economy, its underlying hawkish posture signals RBI’s vigilance against inflation. Thus, even while the near-term outlook is favourable, companies and investors should be on the lookout for wider macroeconomic indicators and future policy changes.

As a result, one should be prepared to deal with interest rate changes in the days ahead, as the RBI may raise or lower the repo rate as necessary during the next policy review. Talking about mutual funds, one should always choose funds that are in line with their risk profile, investment horizon and goals.

This article first appeared on PersonalFN here

{kind=link}