Mutual funds, over the last few years, have now become a popular investment avenue for novice as well as seasoned investors. Thanks to AMFI’s Mutual funds Sahi Hai campaign for this. However, investors often find themselves in a quandary as to how to pick or choose the best mutual fund — because, a fact is, not all mutual funds schemes are sahi hai or befitting for you.

You see, we all have certain broad investment objectives and financial goals to fulfil, viz. buying a dream house, a car, providing the best education to children, building a respectable retirement corpus, etc.). It is important to align your investments with the broad investment objective and financial goals for it to prove meaningful, rather than making ad hoc decisions or simply going by what friends, family, relatives, neighbours or colleagues say and/or do with their investments. Building an investment portfolio is an individualistic exercise; there is no one-size-fits-all approach.

One needs to consider his/her age, risk profile (very aggressive, aggressive, moderately aggressive, moderately conservative, or conservative), financial goals, and the time in hand to achieve those envisioned goals to make suitable choices.

Image 1: Allocation to mutual fund schemes as per risk profile

(For illustration purposes only)

Avoid simply investing in any and every mutual fund scheme based on the historical returns, which is in no way indicative of the scheme would perform in the future.

To choose among a plethora of mutual fund schemes across categories and sub-categories, the best mutual fund schemes for 2023 and beyond, you need to evaluate a host of quantitative and qualitative parameters.

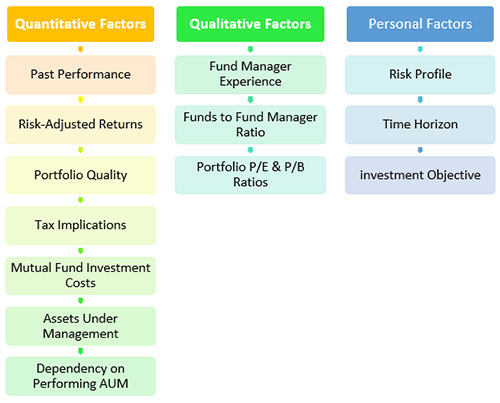

Image 2: Factor to consider to choose the best mutual funds

(For illustration purposes only)

Here’s how to go about choosing mutual funds for your investment portfolio.

-

1. Past Performance Track Record:

When making mutual fund investments, ensure that you do not give undue over-importance to this aspect. Past performance is no indicator of future returns.

Having said that, when you consider the past performance over a longer period, it shows that the fund has gone through multiple market cycles and how it has fared. This performance should be compared to other mutual fund schemes of the respective category and sub-category relative to the benchmark index rather than considered in isolation. The returns of the mutual fund scheme should be compared with the returns over various periods like 1 year, 2 years, 3 years, 5 years, and so on, and across market phases (bull and bear). A majority of mutual funds will perform well in a bull market because all stocks rally when there is euphoria. But the true test is in a bear market, which separates the men from the boys. Therefore one should consider how the mutual fund scheme has fared in the bear market phases as well.

The funds that are managed well usually are able to ride the market volatility smoothly and generate market-beating returns over a longer period. Whereas, if the fund has not performed well in any of the market cycles, it would show underperform and might not turn out to be a good investment.

-

2. Risk Reward Ratios:

Mutual Funds are market-linked investment instruments. The returns generated are subject to market risk. When investing in mutual funds, it is important to evaluate the level of risk it has exposed its investors to. The risk is denoted by the Standard Deviation. Standard Deviation is directly proportional to the overall volatility of the scheme’s returns compared to its average. Higher the Standard Deviation, the higher the risk and vice versa. A Standard Deviation of the scheme must be evaluated over 3 years (for equity-oriented mutual funds), which is a fair time frame to understand the risk.

It is essential for a mutual fund scheme to keep risk under control and adequately compensate investors on a risk-adjusted basis. Sharpe Ratio is a commonly used measure to compare risk-adjusted returns of two or more funds within a category. This ratio shows how much return an investor is earning in correlation to the level of risk being undertaken. It’s calculated by taking the difference between the returns of the investment and the risk-free return, divided by the Standard Deviation of the asset. Note, the higher the Sharpe Ratio, the better the fund’s ability to reward investors with higher risk-adjusted returns.

The other important risk-reward ratio is the Sortino Ratio. This ratio helps to understand a fund’s ability to contain the downside risk, especially during depressed market conditions. It considers only downside deviation for calculating the risk instead of the total volatility of the portfolio. The downside risk denotes returns that fall below a minimum threshold, such as risk-free returns and/or negative returns. The Sortino Ratio is calculated by taking the difference between the returns of the investment and the risk-free return, divided by downside deviation only. Thus it reflects the ability of the mutual fund scheme in managing the downside risk. The higher the Sortino Ratio, the better the fund’s potential of earning higher returns by not taking unwarranted risks.

The Treynor Ratio helps to understand the excess returns earned per unit for a given level of systemic risk. The systemic risk is measured by the Beta of the fund. The Beta of a mutual fund scheme is its volatility relative to its benchmark index. If the Beta is greater than 1, it means the fund is more volatile than the benchmark, less than 1 then it is said to be less volatile than the benchmark, and if equal to 1 then almost equally volatile as the benchmark index. Treynor Ratio is calculated by taking the difference between the returns of the investment and the risk-free return, divided by the Beta of the mutual fund scheme. Checking the Treynor Ratio helps in understanding if the adequately compensating investors vis-a-vis the systemic risk. The higher the Treynor Ratio, the better it is.

Watch this video:

You see, most of these ratios are readily available in the factsheet pages and screeners for you to make a prudent choice of schemes that adequately compensate on a risk-adjusted basis.

-

3. Portfolio Quality And Characteristics:

The future performance of any mutual fund scheme largely depends upon its underlying portfolio. If the underlying portfolio is of good quality, is managed well with conviction, and is favoured by market conditions, it would generate wealth for investors.

When choosing a diversified equity mutual fund scheme, one should ensure that the fund manager has spread the corpus across stocks from different sectors to make it a diversified portfolio and maintains a reasonable churning. In this regard, you must look at the top-10 stock holdings (ideally, the fund should not have more than 50-55% exposure to top 10 holdings), top 5 sectors (ideally should not be more than 40% exposure), and the portfolio turnover ratio (which measures the number of times stocks are bought and sold by the fund manager).

In the case of debt funds, the average maturity, modified duration, and credit quality of debt papers are aspects of the portfolio one must assess by studying the factsheets carefully.

-

4. Investment Philosophy, Processes & Systems, And Credibility of the Fund Management Team:

Other than the returns, risk ratios, and portfolio characteristics, it would do well to understand the investment philosophy, the forte of a fund house in managing an asset class, and the investment processes and systems. These are important aspects when choosing mutual fund schemes for your investment portfolio. Every fund house has an investment philosophy that leads their investment decisions. If the investment ideologies do not match with yours, it may not be apt for you and ultimately disappoint.

If the fund house has a distinct investment philosophy and sound investment processes and systems to drive performance, in the long run, this could be beneficial instead of solely on the stock-picking skill and convictions of the fund manager.

Similarly, the credentials of the fund management team are also crucial. Check for the educational background, the fund manager’s experience, and the number of schemes managed by him/her. Ideally, a fund manager should not be handling more than 4 to 5 schemes, otherwise, it could weigh on the performance of schemes under his watch. Thus, besides the scheme you are considering for investment, also check how the other schemes managed by the respective fund manager have fared across time frames and market phases.

-

5. Asset under Management:

The Asset Under Management (AUM) of a mutual fund scheme is the composite market value of its underlying assets. In simple words, it indicates the total size of the fund and the people who have invested in it.

However, one should not invest in a scheme just because it has a high AUM. It has no relationship with the kind of returns a fund could generate. In other words, high returns do not guarantee high returns.

In the case of small-cap equity mutual funds, a high AUM can make it challenging for the fund manager to manage the portfolio as entering and exiting the less liquid small-sized companies will become difficult. In fact, for this reason, at the market high, some fund houses have stopped accepting fresh investments in their small-cap mutual fund schemes.

[Read: Why are Mutual Fund Houses Pausing or Limiting Investments in Small Cap Funds]

A high AUM can be favourable to liquid and debt funds as the fund becomes less vulnerable to redemption pressure from a chunk of investors.

Ultimately, be it whichever scheme and irrespective of its AUM, the fund house must be an efficient asset manager and not just an asset gatherer. In this respect, it is important to evaluate the proportion of AUM actually performing.

-

6. Expense Ratio

The Expense Ratio is nothing but the costs that are levied on the mutual fund scheme (by the fund house) as a percentage of its daily net assets. The costs incurred by the fund house on their schemes are investment management fees, brokerage on buying and selling securities, registrar & transfer fees, custodian fees, legal fees, audit fees, sales & marketing/advertising expenses, administrative expenses, and so on. These costs are levied on the mutual fund scheme as a percentage of its daily net assets and are referred to as the Total Expense Ratio (TER). There are guidelines on the maximum TER a fund house can levy on its actively managed mutual fund schemes (equity-oriented and debt-oriented) and the passively managed mutual fund schemes. The TER is charged to the NAV of the scheme. If a mutual fund scheme is charging a high Expense Ratio, it could weigh on the performance of the scheme. But it does not mean that a fund with a lower Expense Ratio is always better. Each scheme follows its own investment strategy and style, which you, the investor, need to recognise.

-

7. Investment Mandate And Investment Objective:

Every mutual fund scheme, depending on the category and sub-category, has a distinct investment mandate. Depending on that, the scheme allocates its assets and the investment objective it set out. It is important to choose schemes that are in congruence with your investment objectives, financial goals and time horizon. Therefore make it a point to read the Scheme Information Document (SID) carefully before investing in any mutual fund scheme.

[Read: How to Invest in Mutual Funds]

Watch this video:

If you have any difficulties in choosing among suitable and best mutual fund schemes, seek the services of a SEBI-registered investment adviser.

Once you have suitable and among the best mutual fund schemes in the investment portfolio, ensure you are giving enough time for money to grow and keeping risk-return expectations realistic.

And finally, make it a point to timely review your investment portfolio (bi-annually or annually) so that you are on track to accomplish the envisioned financial goals.

Happy Investing!

This article first appeared on PersonalFN here

{kind=link}