The capital market regulator, SEBI in its board meeting held in March 2023, had taken a major decision to set up a Corporate Debt Market Development Fund (CDMDF), that shall serve as a Backstop Facility for specified debt mutual funds during market dislocations, i.e., in times of stress and, in general, enhance liquidity in the secondary market. This decision was taken perhaps as a learning out of the IL&FS and DHFL fallout, and after Franklin Templeton Mutual Fund shut six of its debt mutual fund schemes abruptly amid the COVID-19 pandemic.

What is a Backstop Facility for Debt Mutual Funds?

Well, it is a facility wherein an entity shall buy out illiquid investment-grade corporate bonds from debt mutual funds in times of severe stress in the debt market. So, if there is heavy redemption pressure or rating downgrade and mutual funds find it challenging to sell their debt instruments, particularly the low-rated ones (instruments below AAA rating) due to risk aversion among buyers, the Backstop Facility could be used.

With the Backstop Facility, an entity acting as a buyer, mutual fund houses will be able to readily sell their securities and generate enough liquidity to meet redemption requests. Thus it shall preclude debt-oriented mutual funds from selling good quality instruments due to compulsion, resulting in higher allocation to low-rated, illiquid instruments in the portfolio.

SEBI has now come up with a framework for the Backstop Facility for Debt Mutual Funds

Last week, on July 27, 2023, SEBI released the framework to be followed by the Corporate Debt Market Development Fund (CDMDF) and finance minister, Ms. Nirmala Sitharaman announced the launch of this Backstop Facility for debt mutual funds.

CDMDF would be set up as an Alternative Investment Fund (AIF) in the form of a Trust under SEBI (Alternative Investment Funds) Regulations, 2012 (AIF Regulations).

CDMDF shall be launched as a closed-ended scheme with an initial tenure of 15 years from the date of its initial closing. It will be sponsored and managed by SBI Funds Management Ltd., the Asset Management Company of SBI Mutual Fund (SBI AMC), which is a ‘Deemed Government Company’ under the Companies Act, 2013, as it is owned and controlled directly or indirectly by the Government.

The CDMDF would be required to comply with the Guarantee Scheme for Corporate Debt (GSCD) as notified by the Ministry of Finance. The Trust/Fund to manage the scheme is called the Guarantee Fund for Corporate Debt (GFCD).

GFCD is a Trust Fund formed by the Department of Economic Affairs (DEA), Ministry of Finance, Government of India and shall be managed by National Credit Guarantee Trustee Company Ltd. (NCGTC), a wholly owned company of the Department of Financial Services (DFS), Ministry of Finance, Government of India.

Hence, there is a 100% guarantee against the debt raised by CDMDF. The guarantee shall cover debt raised, along with interest accrued and other bank charges thereon, and shall not exceed Rs 30,000 crore.

What type of securities will CDMDF invest in?

As per SEBI’s framework, CDMDF shall deal in the following securities during normal times:

- Low-duration Government Securities

- Treasury bills

- Tri-party Repo on G-sec

- Guaranteed corporate bond repo with a maturity not exceeding 7 days.

The long-term rating of issuers shall be considered for the money market instruments. However, if there is no long-term rating available for the same issuer, then based on credit rating mapping of Credit Rating Agencies (CRA)s between short-term and long-term ratings, the most conservative long-term rating shall be taken for a given short-term rating.

You see, dealing in the above liquid instruments shall make sure enough liquidity is available for CDMDF and instil confidence among the market participants.

Does the Corporate Debt Market Development Fund have an expense ratio?

Yes, like any other fund, the Corporate Debt Market Development Fund (CDMDF) will also have an expense ratio.

As per SEBI’s framework, the fees and expense ratio of the fund will be as follows:

During Normal times: 0.15% + tax of the Portfolio Value is charged on a daily pro-rata basis.

During Market stress: 0.20% + tax of the Portfolio Value charged on a daily pro-rata basis.

Note, “Portfolio Value” here means the aggregate amount of portfolio of investments including cash balance without netting off of leverage undertaken by the Fund.

How will the NAV of the Corporate Debt Market Development Fund be computed?

As per the framework, CDMDF is expected to follow a fair pricing model. The following indicative factors would be followed while determining the purchase price of debt securities.

- Valuation policies prescribed for Mutual Funds (based on the principles of fair valuation).

- Previous day’s valuation of securities by valuation agencies before the date of Purchase.

- Average 10 days valuation prior to the start of market dislocation.

- The mark-up in yield over the previous day may be limited to arrive at the floor price. For example, it may be 25/50/75 basis point (bps) over AA/Below AA securities respectively.

- Consideration of Spread over benchmark/ spread over sovereign yields.

- Qualitative factors that may have a bearing on arriving at a fair price.

Furthermore, the investment framework states:

- CDMDF would buy securities from the secondary market of only investment grade, listed and having residual maturity of up to 5 years.

- CDMDF shall not buy any unlisted, below investment grade or defaulted debt securities or securities in respect of which there is a material possibility of default or adverse credit news or views. The rationale for the same shall be documented.

- Purchase of securities to be done as per the above fair pricing guidelines to be adjusted if considered appropriate by the investment manager for liquidity risk, interest rate risk, and credit risk. Buying/trading to be at a fair price but not at a distressed price.

- Selling at breakeven/profit as the market stabilizes, to reduce borrowing as soon as possible.

- Valuation of the portfolio shall be governed by existing norms on valuation under the Mutual Fund regulatory framework.

SEBI has asked AMFI to specify the detailed guidelines for the purchase of securities by CDMF in consultation with SEBI. Stock exchanges are expected to provide a separate window to purchase as per AMFI-issued guidelines within three months from July 27, 2023.

A Balasubramanian, the Chairman of AMFI (as well as the Managing Director and CEO of Aditya Birla Sun Life Mutual Fund), speaking to the media said the contribution made by mutual fund players (for Backstop Facility) is close to Rs 3,300 crore. “Those (fund houses) that are running fixed income schemes will contribute a portion of the scheme. In addition, each AMC will contribute to the capital from their balance sheets,” he said.

Corporate Debt Market Development Fund to follow Loss Waterfall Accounting

Loss waterfall accounting is the system used for pooled investments –CDMDF in this case. It is done in the pecking order of the allocation to the respective instrument.

According to SEBI, the following shall be the approach for reflection of the waterfall in the NAV of units of CDMDF.

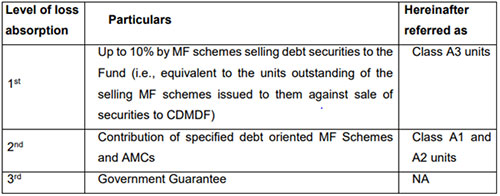

There shall be three classes of units to be allotted by CDMDF, which shall be as follows:

- Class A1 and Class B units shall be allotted to AMCs and Sponsor/IM respectively (against a one-time contribution of 0.02% of AUM of specified debt schemes and Sponsor/IM commitment). Class A1 units and Class B units should be treated at par and referred to as Class A1 units only.

- Class A2 units shall be allotted to specified debt schemes (contributing 0.25% of AUM of specified debt schemes)

- Class A3 units shall be allotted to Mutual Fund schemes selling debt securities to the Fund (where 10% of the consideration is in the form of units of CDMDF, called A3 units)

Daily NAV should reflect the fair value of each unit class including the effect of differential treatment of A3 unit class.

The loss waterfall based on the CDMDF framework is as follows:

(Source: SEBI)

Moreover, as per the regulations, the following eight-point process is expected to be followed:

- All profits/losses/income/gains/expenses are to be apportioned to A1 and A2 unit classes in the ratio of their AUM during normal times.

- A3 units are to be allotted at the same NAV as that of A1 & A2 at the time of the opening of market dislocation.

- All profits/losses/income/gains/expenses (including the cost of leverage) are to be apportioned to all the 3 class of units during the market dislocation and subsequently till A3 units exits (i.e A1/A2/A3), except that the NAV of A1 and A2 should not drop below their opening NAV (opening NAV at the time of market dislocation). Since A1 and A2 units are to be protected at their opening NAV to that extent the excess/unabsorbed loss/expense would be debited to only A3 unit class. This would mean the NAV of A3 units could drop below the NAV of A1&A2

- Any subsequent profits/gains/income will be first credited to the A3 unit class to the extent that they come back at par with A1 & A2 NAV, and then the balance to be apportioned to all the three unit classes.

- A3 units will not get any exit till there is an outstanding portfolio from market dislocation and leverage is completely paid.

- Any subsequent allotment of A3 units would be at the same NAV as that of the existing A3 units (if they exist), otherwise at opening NAV of A1 and A2. There will be only one class/bucket of A3 units irrespective of whether they were issued in a subsequent tranche of purchase during a particular phase of market dislocation or were issued during another phase of market dislocation. Therefore, any adjustment for loss/expense will be carried out to the entire bucket of A3 units irrespective of when they were allotted.

- There will not be any segregation of portfolio linking to different phases or tranches of purchase during the market dislocation, the entire portfolio will be one common pool, both during the normal times or during the market dislocation including if there is any security that exists from normal times and is continued during the market dislocation.

- The accounting of A3 and certain adjustments of NAV may require manual workings by the fund accountant and will not be completely system driven. Such manual workings can be subject to a second check by the concurrent auditor.

Disclosure of NAV of Corporate Debt Market Development Fund

Like any other fund, CDMDF should disclose its NAV. The NAV will be disclosed by 9:30 PM on all business days on the website of its Investment Manager and AMFI. And for times when CDMDF would have exposure to corporate debt, such NAV would be required to be disclosed by 11 PM on all business days.

How will investors benefit from this Backstop Facility?

Well, in times of extreme stress or credit risk, the Backstop Facility in the form of CDMDF would ensure debt mutual funds do not have to sell their quality underlying portfolio to meet redemption pressures or due to rating downgrades and address the liquidity needs. For investors, it shall nearly eliminate the risk of fund houses abruptly shutting their debt-oriented mutual fund schemes.

That being said, make investors should debt mutual funds carefully considering the portfolio characteristics, the type of debt papers held, the ratings of the respective debt papers, the average maturity profile, etc. and not just the returns.

Also, understand the investment ideologies, processes, and systems. If the mutual fund house lacks a robust risk management framework and depends excessively on ratings assigned by credit rating agencies, the fund manager compromises on the quality of the portfolio, chases yields, and plays down on the liquidity aspects of the portfolio, investors should be concerned.

[Read: 5 Best Debt Mutual Funds to Invest in 2023]

Besides, it would do well to consider the current interest rate scenario and invest in congruence with your personal risk profile, investment objective, liquidity needs, and time horizon.

Happy Investing!

This article first appeared on PersonalFN here

{kind=link}