The Reserve Bank of India (RBI) for the second successive time, kept the policy repo rate under the Liquidity Adjustment Facility (LAF) unchanged at 6.50% in its June 2023 bi-monthly monetary policy 2023-24 meeting. All six members of the MPC voted in favour of this decision.

Consequently, the Standing Deposit Facility (SDF) rate — which absorbs excess liquidity — remained unchanged at 6.25% and the marginal standing facility (MSF) rate (which is a window for banks to borrow from the RBI in an emergency, when inter-bank liquidity dries up) and the Bank Rate (at which RBI lends money to commercial banks for short-term loans) at 6.75%.

This monetary policy action was in line with market expectations, given that inflation is moderating within the comfort range of the central bank and domestic macroeconomic fundamentals are strengthening. “We have made good progress in containing inflation, supporting growth and maintaining financial and external sector stability. Despite three years of global turmoil, India’s growth has bounced back and headline CPI inflation is easing. This confluence of factors gives us the confidence that our policies are on the right track,” said RBI Governor Shaktikanta Das in his statement.

However, what is a bit surprising was that a majority of MPC committee members (5 out of 6) voted in favour of maintaining the policy stance, i.e., “to remain focused on the withdrawal of accommodation to ensure that inflation progressively aligns with the target, while supporting growth.”

Table: RBI Monetary Policy Actions and Stance

| Month | Repo Policy Rate | Policy Action (Basis points) |

Monetary Policy Stance |

| Feb-2019 | 6.25% | -25 | Neutral |

| Apr-2019 | 6.00% | -25 | Neutral |

| Jun-2019 | 5.75% | -25 | Accommodative |

| Aug-2019 | 5.40% | -35 | Accommodative |

| Oct-2019 | 5.15% | -25 | Accommodative |

| Dec-2019 | 5.15% | Status quo | Accommodative |

| Feb-2020 | 5.15% | Status quo | Accommodative |

| Mar-2020 (an exceptional off-cycle meeting) | 4.40% | -75 | Accommodative |

| May-2020 (an exceptional 2nd off-cycle meeting) | 4.00% | -40 | Accommodative |

| Aug-2020 | 4.00% | Status quo | Accommodative |

| Oct-2020 | 4.00% | Status quo | Accommodative |

| Dec-2020 | 4.00% | Status quo | Accommodative |

| Feb-2020 | 4.00% | Status quo | Accommodative |

| April-2021 | 4.00% | Status quo | Accommodative |

| June-2021 | 4.00% | Status quo | Accommodative |

| Aug-2021 | 4.00% | Status quo | Accommodative |

| Oct-2021 | 4.00% | Status quo | Accommodative |

| Dec-2021 | 4.00% | Status quo | Accommodative |

| Feb-2022 | 4.00% | Status quo | Accommodative |

| Apr-2022 | 4.00% | Status quo | Accommodative |

| May-2022 (Off-cycle meeting) | 4.40% | +40 | Accommodative |

| June-2022 | 4.90% | +50 | Focus on withdrawal of Accommodative stance |

| Aug-2022 | 5.40% | +50 | Focus on withdrawal of Accommodative stance |

| Sep-2022 | 5.90% | +50 | Focus on withdrawal of Accommodative stance |

| Dec-2022 | 6.25% | +35 | Focus on withdrawal of Accommodative stance |

| Feb-2023 | 6.50% | +25 | Focus on withdrawal of Accommodative stance |

| Apr-2023 | 6.50% | Status quo | Focus on withdrawal of Accommodative stance |

| May-2023 | 6.50% | Status quo | Focus on withdrawal of Accommodative stance |

Data as of June 8, 2023

(Source: RBI Monetary Policy Statements, Data collated by PersonalFN Research)

It was expected the RBI would tone down the monetary policy stance to an extent, on the back of a large favourable base effect and success achieved in taming inflation. But RBI Governor stated that since CPI inflation remains above the medium target of 4.0% (within a band of +/- 2.0%), and being within the tolerance band is not enough, the stance of the policy also was left unchanged.

Even though CPI inflation in April 2023 fell to 4.7% (an 18-month low) in April 2023 due to lower food inflation, fuel & light inflation, and core inflation (which excludes food, fuel and light inflation) also dipped, the RBI observed risk to the headline inflation trajectory emanating from…

- Milk prices due to supply shortfalls and higher fodder costs

- The spatial and temporal distribution of monsoon on the prospects of agricultural production

- Uncertain outlook for crude oil prices

- Hardening in input costs and output prices (according to the early results from the Reserve Bank’s surveys for manufacturing, services, and infrastructure firms polled)

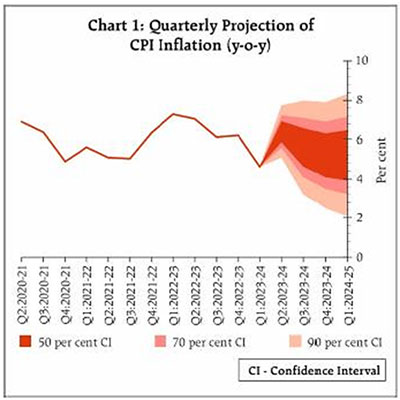

Still, considering these factors and assuming a normal monsoon this year, the RBI projected CPI inflation at 5.1% in 2023-24 (with Q1 at 4.6%, Q2 at 5.2%, Q3 at 5.4% and Q4 at 5.2%) with the risks evenly balanced, a tad lower than 5.2% projected in it April 2023 monetary meeting.

Graph: RBI’s quarterly projection of CPI Inflation

Data as of June 8, 2023

(Source: RBI 2nd bi-monthly Monetary Policy Statement 2023-24)

The cumulative rate hike of 250 basis points undertaken by the MPC is transmitting through the economy and its fuller impact should keep inflationary pressures contained in the coming months, according to the RBI. The headline CPI inflation is projected to decline in 2023-24 from its level in 2022-23 but would still be above the target, warranting continuous vigil. And in this regard, the progress of the monsoon is critical stated the central bank.

Hence, the monetary policy RBI monetary policy resolution stated that it would need to be carefully calibrated for alignment of CPI inflation with the target. It will continue keeping a close vigil on the evolving inflation and growth outlook.

Speaking about the growth outlook, the RBI is of the view that higher rabi crop production in 2022-23, the expected normal monsoon, and the sustained buoyancy in services should support private consumption and overall economic activity in the current year. The government’s thrust on capital expenditure, moderation in commodity prices, and robust credit growth are expected to nurture investment activity. However, weak external demand, geoeconomic fragmentation, and protracted geopolitical tensions are some of the risks to the growth outlook. Taking all these factors into consideration, the RBI has projected real GDP growth for 2023-24 at 6.5% (Q1 at 8.0%, Q2 at 6.5%, Q3 at 6.0%, and Q4 at 5.7%) with risks evenly balanced.

What should be your strategy to invest in debt mutual funds now?

Although the RBI has chosen to remain focused on the withdrawal of accommodation to ensure that inflation progressively aligns with the target, while supporting growth, it appears that we are near the peak of the interest rate upcycle. Thus, it would be an opportune time now to invest in longer-duration debt mutual funds whereby you benefit from higher yield and unlock the capital growth.

Typically, one can consider Medium to Long Duration Debt Funds, Long Duration Funds, Gilt Funds, and Dynamic Bond Funds in the current interest rate cycle by assuming slightly higher risk and keeping a time horizon of 2 to 3 years or more.

For those who can’t afford to take slightly high risk and/or the investment horizon is very short-to-short (a few days, weeks or a few months), Overnight Funds, Liquid Funds, Ultra Short Duration Funds, and/or Money Market Funds could be considered. Don’t just invest in debt mutual funds randomly, and don’t be discouraged by the new tax rule, wherein the capital gains on selling debt mutual funds units, irrespective of Short Term Capital Gain (STCG) or Long Term Capital Gain (LTCG) will be taxed at the marginal rate of taxation, i.e. as per one’s income-tax slab.

[Read: Does it Make Sense to SIP in Debt Mutual Funds?]

Even now debt funds have an edge over bank fixed deposits as regards returns are concerned. To make the best choice among the plethora of schemes available within the respective sub-categories of debt funds, all one must do is evaluate a host of quantitative and qualitative parameters such as the following:

- The credentials and experience of the fund management team

- The AUM and expense ratio of the scheme

- The portfolio characteristics (who are the issuers, the sector they belong to, the type of debt papers held, the ratings of the respective debt papers, etc.)

- The maturity profile of the fund

- Returns across time periods (3 months, 6 months, 1 year, 2 years, 3 years, and so on)

- The risk ratios (Standard Deviation, Sharpe Ratio, Sortino Ratio, etc.)

- The current interest rate cycle

- The performance across interest rate cycles

Plus, it would be better to understand the investment ideologies, processes, and systems followed at the mutual fund house.

In the evaluation process, if the mutual fund house lacks a robust risk management framework and depends excessively on ratings assigned by credit rating agencies, the fund manager compromises on the quality of the portfolio, chases yields, and plays down on the liquidity aspects of the portfolio, one should be concerned.

Want to know which are the Best Debt Mutual Funds to Invest in 2023? Click here.

Avoid picking debt mutual fund schemes looking at just the past returns, as they are in no way indicative of the future performance of the scheme.

Be a thoughtful investor and follow a holistic approach to make the best choice among the debt mutual fund schemes.

Happy Investing!

This article first appeared on PersonalFN here

{kind=link}