One of the crucial steps while managing your mutual fund portfolio is to timely check its overall health. Even if you have invested in some of the best mutual fund schemes (of the respective categories and sub-categories), a ‘buy-and-forget’ approach cannot be followed. Given that mutual fund investments are subject to market risk, the best-performing schemes of today need not be top performers of the future. Remember, past performance is in no way indicative of future returns. If you don’t keep an eye on your mutual fund investments, it could derail the path to wealth creation.

Moreover, there may be situations in life that could warrant analysing and reviewing your mutual fund portfolio, viz. changes in financial circumstances, goals, milestones (such as a change in relationship status, birth of a child, wedding in the family, demise of a family member, etc.), progressing age, tax status, and contingencies, as they usually alter one’s risk-taking ability.

A timely analysis and review of the mutual fund portfolio makes sure that your investments are on track and in line with your financial situation, risk profile, investment objectives, financial goals, and the time in hand to achieve those goals.

[Read: Why a Year-end Mutual Fund Portfolio Review Makes Sense]

Currently, the volatility in the Indian equity markets has intensified due to a slew of macroeconomic challenges, such as the ongoing Russia-Ukraine conflict, elevated inflation, policy rate hikes by major central banks, higher borrowing rates, a weak Indian Rupee against the U.S. Dollar, the ripple effect of bank failures in the U.S., and the potential impact of all this on economic growth.

Such a scenario could weigh down on corporate earnings plus end up upsetting business and consumer confidence, among other things. To mitigate the potential risk involved, following a sensible asset allocation is necessary.

[Read: What Should Be Your Mutual Fund Asset Allocation Strategy Amid Rising Global Uncertainty]

So, here are a few factors to consider while analysing and reviewing your Mutual Fund Portfolio:

-

Assess whether your asset allocation is right

Even if the mutual fund schemes in your portfolio may be the best-performing ones and there isn't a need to make any deliberate adjustments to the portfolio constituents, given that markets are near their lifetime high, the asset allocation of your portfolio may have changed thus bringing in a deviation in the asset mix (of equity, debt, and gold) that is best suited for you.

Do note, asset allocation is the cornerstone of investing and must be followed always. When investing in mutual funds, your asset allocation must correspond with your age, financial situation, risk profile, financial goal/s and investment horizon. You may consider reallocating your investments if the current asset mix is unsuitable.

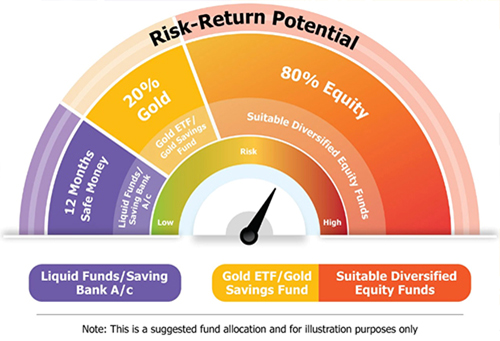

Broadly, if risk appetite is high and the time to achieve the financial goals is more than 3 years, a 12-20-80 asset allocation model could be suitable. Herein 12 months of regular monthly expenses (including EMIs on loans) could be parked into a Liquid Fund (to take care of exigencies), 20% to gold (which usually has an inverse correlation with equities), and 80% (the growth portion) in suitable diversified equity funds. Such an asset mix could offer stability, growth, and protection.

But if you feel you require personalised advice, then consider reaching out to a SEBI-registered investment adviser who could customise the asset allocation for you.

-

Check if your mutual portfolio aligns with your goals

You may have been thoughtful and devised a prudent investment strategy at the start, but it's possible that over time, your priorities may have changed, the financial situation is different, possibly a milestone event, age, among a host of other things.

As a result, your risk-return expectations may have changed, which thus makes it necessary to take a relook at your portfolio comprehensively to realign it once again. You may have to trim exposure to equities if the risk profile has changed to low to balance the risk-return trade-off.

[Read: Are You Setting Your Risk-Return Expectations Right While Investing in Mutual Funds?]

-

Gauge the portfolio characteristics of your mutual fund portfolio to avoid undue risks

The mutual fund portfolio must be analysed for AMC-wise concentration, category and sub-category-wise weightage, and exposure to sectors (and quality of papers in the case of debt mutual funds). This shall help you assess if your mutual fund portfolio is well-diversified across fund houses, investment styles, market capitalisations, sectors, and quality of debt papers.

Besides, care needs to be taken not to over-diversify the mutual fund portfolio with too many schemes, as it may make it challenging to manage it and possibly reduce the portfolio returns. Remember the adage: Too much of anything is good for nothing.

"Wide diversification is only required when investors don't know what they are doing," says legendary investor Warren Buffett.

Ideally, you should avoid holding more than 10 to 12 mutual fund schemes in your portfolio.

[Read: Holding Too Many Mutual Funds? Here's How You Can Reduce the Number of Schemes in Your Portfolio]

-

Examine whether mutual fund schemes are consistently underperforming

Other than the asset mix, the performance of your mutual portfolio is hinged on how the various schemes from the respective categories and sub-categories perform.

To create optimal returns, you need to detect the red flag (if any) and eliminate consistently underperforming mutual fund schemes that may harm the health of your portfolio. In the culling process, enough time needs to be given for mutual fund schemes to prove their worth — in the case of equity mutual funds, at least 3 years — otherwise, it would amount to trading and not investing. Investing involves building an optimally diversified portfolio of assets and staying with it through market ups and downs to potentially earn fruitful results over the long term. Mutual funds are an investment vehicle and not meant for trading.

[Read: Do You Invest in Mutual Funds with the Mind of a Trader?]

While timing your entry and exit in equity mutual funds may appear as an easy way to sail through the volatile nature of the market, in reality, it is not and could prove detrimental to your health and wealth. If your portfolio is temporarily underperforming when market sentiment turns sour, you should not panic, as short-term underperformance caused due to market turbulence can be ignored.

For mutual fund schemes that have been consistent underperformers, you could consider redeeming and switching to the worthy ones. The selection for the alternative schemes must be done through a rigorous selection process evaluating a host of quantitative and qualitative parameters, plus keeping in mind your risk profile, investment objectives, and financial goals.

-

Study if portfolio rebalancing is necessary

If the portfolio has high exposure to equities, which are high-risk-high-return investments, but one's risk tolerance level has reduced to moderate or conservative, and/or is less than three years away from the envisioned financial goal/s; one could consider rebalancing the portfolio and shifting to relatively low-risk investments such as debt to avoid a slump in portfolio returns. As mentioned earlier, rebalancing of the portfolio is necessary if a remarkable deviation is observed against the original asset allocation meant for one's mutual fund portfolio due to a sharp movement in any asset class.

Keep in mind that analysing your mutual fund portfolio periodically by following a prudent approach would not only help you check the health of your portfolio but ensure your long-term financial well-being. Thus, ideally, review your mutual fund portfolio bi-annually or annually, depending on your needs and the prevailing market conditions.

Happy Investing!

This article first appeared on PersonalFN here

{kind=link}