The global economy has been facing a lot of uncertainty, with concerns about a potential recession looming large, the Russia-Ukraine war, geopolitical tensions, pandemic, climate events, and persistently troublesome inflation. Consequently, the Indian equity market and equity mutual fund returns have witnessed high volatility off late.

While the Indian economy has shown resilience and remains a bright spot among major global economies, investors should not be complacent, as India cannot be completely decoupled from a global slowdown. Thus, the year 2023 may not be an easy year for wealth creation, particularly for equities, and investors should be prepared for volatility and potential market corrections in the interim. Therefore, avoid skewing your portfolio irrationally to equities looking at past returns or the success stories of some other equity investors.

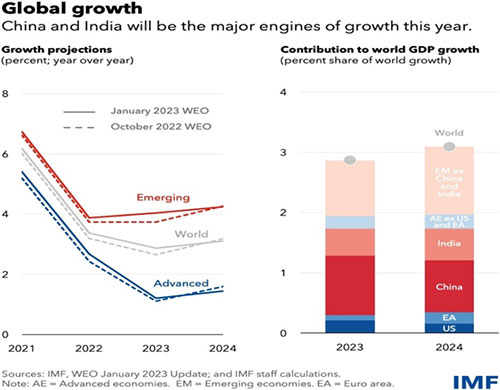

IMF’s projection of global economic growth

(Source: IMF)

Following the right mutual fund asset allocation strategy is a prudent way to minimise the risk and ride out global uncertainty. Asset allocation is an investment strategy that balances the risk-reward trade-off by diversifying investment across different asset classes such as equity, debt, and gold.

Different types of mutual funds invest in different securities, such as stocks, bonds, commodities, etc., depending on their investment mandate. Accordingly, every mutual fund category has a distinct risk-return characteristic.

So, when you invest across different categories of mutual funds that invest in different asset classes and follow different investment strategies & style, the impact of any sharp negative movement in one asset class/strategy/style is usually mitigated by the likely rise in other.

Even within categories, certain sub-categories and schemes are more sensitive to certain risks, while some are exposed to others. For instance, under equity mutual funds, a Mid Cap Fund is more likely to face sharp volatility in the interim if the equity markets correct compared to Large Cap Funds; nevertheless, they are likely to generate higher returns over the long run.

As an investor, it is important that you follow the right investment allocation and carefully allocate money across different categories and sub-categories of mutual funds by evaluating your financial needs and circumstances. This will help you achieve your target comfortably without attracting undue risks.

Performance across asset classes differs every year

*Data as of April 13, 2023

(Source: ACE MF)

Why Asset Allocation is important?

1) Prevents irrational behaviour

A disciplined approach is important for achieving goals through mutual funds. If asset allocation is done optimally as per your risk appetite, financial goals, and investment horizon, it may help eliminate irrational behaviour such as greed and fear during phases of global uncertainty, which otherwise could harm the growth prospects of your investment.

2) Earns stable returns across market conditions

Equity mutual funds have high return potential, but they are also susceptible to high volatility. This risk can be balanced out if you invest in other asset classes. Investment in debt mutual fund acts as a cushion against market volatility by offering sort of stable returns, while gold fund acts as a portfolio diversifier and a hedge against inflation.

3) Stay on the right track to the goal

Asset allocation allows you to align your investment with your financial goals. Equity mutual funds are suitable for long-term goals, whereas debt mutual funds are suitable for short-term goals and for building an emergency corpus. By including a mix of equity, debt, and other asset classes, you create a balanced mutual fund portfolio to meet your various short-term and long-term needs.

How to decide what is the best-suited Asset Allocation?

To decide the best and the most suitable asset allocation that aligns with your financial needs, you need to pay attention to the following factors:

a) Financial Goals

The financial goal you wish to achieve is an important step that helps you determine the best-suited asset allocation. An investment without a specific goal is just like driving a car without a destination in mind. Your goals should be quantifiable and measurable. Based on your goals, you will be able to arrive at the amount to be invested, the expected rate of returns, and the most suitable mutual fund category that will help you achieve each of these goals.

[Read: How to Set Achievable Financial Goals And Plan to Achieve Them]

b) Risk Profile

Different types of investment carry different risk-reward profiles. It is important to understand the risks related to each of the investment avenues and pick the one that aligns with your risk tolerance levels. You can consider high-risk instruments such as equity mutual funds if you have a high-risk profile to handle market volatility. Do note that your age, financial circumstances, the life stage you are in, etc., can affect your ability to take risks.

[Read: 5 Things to Consider While Evaluating Your Risk Appetite]

c) Investment Horizon

Your investment horizon is the time period for which you will hold on to your investment before selling it. A long-term investment horizon allows you to follow an aggressive investment approach, as you have enough time to recover from any short-term losses and sharp fluctuations. On the other hand, if you have a short-term investment horizon, you should opt for relatively stable asset classes and investment avenues therein (such as debt mutual fund) to reduce the impact of market volatility.

Here is an indicative allocation of how individuals belonging to risk profiles can achieve optimal asset allocation through mutual funds:

| Category | Aggressive | Moderately Aggressive | Moderate | Moderately Conservative | Conservative |

| Equity Mutual Fund | 90%-100% | 75%-80% | 60%-70% | 40%-50% | 20%-30% |

| Debt Mutual Fund | 0%-5% | 10%-15% | 20%-30% | 40%-50% | 70%-80% |

| Gold Fund | 0%-5% | 5%-10% | 5%-10% | 5%-10% | 0%-5% |

(For illustration purposes only)

If you already have an asset allocation plan, stick to it regardless of the global uncertainty. If you don’t, start off by setting aside 12 months of emergency corpus in safe avenues such as Liquid Fund. Invest the remaining corpus across equity mutual funds, debt mutual funds, and gold funds, depending on your investment objective, risk appetite, and investment horizon.

The equity portion can consist of a Large Cap Fund, Large & Midcap Fund, Flexi Cap Fund, Value Fund, and Mid Cap Fund that will offer you the benefit of diversification across market caps, strategies, and investment styles. Decide the allocation on each of these after considering your risk profile and investment objective. For instance, if you are averse to very high risk, allocate more towards relatively stable sub-categories such as Large Cap Fund and Flexi Cap Fund while limiting allocation to highly volatile sub-categories such as Mid Cap Fund. Given the volatile nature of the equity market, it is advisable to stagger your investment instead via SIP mode instead of investing a lump sum amount.

The debt portion can be diversified across Liquid Funds, Corporate Bond Funds, and Banking & PSU Debt Funds. Remember that debt funds are not risk-free, so ensure that you select the most suitable scheme after understanding the underlying risk. For investment in gold, prefer to invest via Gold Funds or Gold ETFs instead of holding physical gold.

This asset allocation strategy could potentially offer your portfolio the correct mix of stability, growth, and protection.

This article first appeared on PersonalFN here

{kind=link}