Finance Minister Nirmala Sitharaman today, February 01, 2023, presented the Union Budget 2023-24, the last full budget of the Modi 2.0 government before India sets off for the Lok Sabha election in May 2024. With national polls nearing, some market experts expected the Union Budget announcements to be populist ones aimed at converting votes.

However, just like last year, the Union Budget announcements this year focused on pro-growth measures with a special boost to the infrastructure and inclusive development. This is in line with the government’s plan to make India a $5 trillion economy by FY 2024-25.

Notably, the government does not have much fiscal space to deliver a populist budget due to high borrowings, elevated inflation, and plans to stay on track towards fiscal consolidation.

That said, the Union Budget did announce some major changes pertaining to personal finance and income tax to provide relief to salaried individuals.

1) New income tax slab and rates

The Finance Minister Ms.Nirmala Sitharaman has announced major changes in the income tax for the salaried class. Currently, those with income of up to 5 lakh do not pay any income tax. Now the government has proposed to increase the rebate to 7 lakh, meaning those with a salary of up to 7 lakh do not have to pay any income tax.

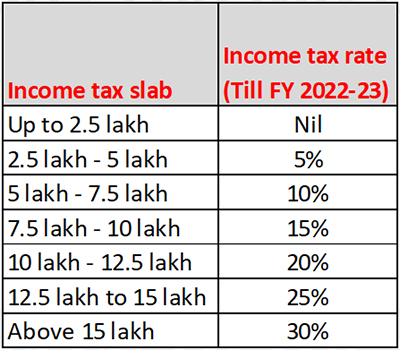

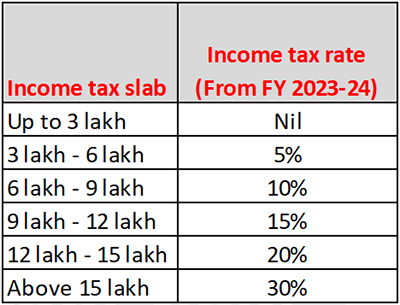

The government has also announced changes in income tax rates for individuals opting for the new tax regime. See the table below for the comparison of income tax rates under the new tax regime till FY 2022-23 and the rates applicable from FY 2023-24.

Income tax rates under the new tax regime

|  |

Furthermore, the government has extended the benefit of standard deduction to salaried individuals and pensioners in the new tax regime. With this, those with an income of Rs 15.5 lakh or more will benefit by an additional Rs 52,500 in terms of tax saving.

The Finance Minister also announced that the new tax regime would be the default tax regime, but tax payers will have the option to opt for the old tax regime.

2) Reduction in a surcharge

The Finance Minister has reduced the highest surcharge levied on income tax to 25% from 37% under the new tax regime. This will effectively reduce the tax rate on income above Rs 2 crore to 39% from the current 42.7%.

3) Mahila Samman Saving Certificate

The government will introduce a new one-time small saving scheme for women called ‘Mahila Samman Bachat Patra’ or ‘Mahila Samman Saving Certificate’. This deposit facility will be available for a 2-year period, up to March 2025, earning a fixed interest rate of 7.5% with a partial withdrawal option. The maximum amount that can be deposited under this is Rs 2 lakh.

4) Higher deposit limit

The Finance Minister has proposed enhancing the maximum deposit limit for Senior Citizen Saving Scheme (SCSS) from Rs 15 lakh to Rs 30 lakh. Similarly, the maximum deposit limit for the Monthly Income Plan has been raised from Rs 4.5 lakh to Rs 9 lakh, and from Rs 9 lakh to Rs 15 lakh the in case of a joint account.

5) Boost to MSMEs

Micro enterprises with a turnover of up to Rs 2 crore and certain professionals with a turnover of up to Rs 50 lakh can avail of the benefit of presumptive taxation i.e. they will be exempt from maintaining books of accounts. For tax-payers whose cash receipts are not more than 5%, the government has proposed enhanced limit of Rs 3 crore and 75 lakh, respectively.

6) Tax on high-value insurance proceeds

The Finance Minister has proposed to tax income from insurance policies having premium above Rs 5 lakh in a year. This will be applicable to policies sold after April 01, 2023. The income will be exempt if it is received upon the death of the insured person.

7) Other personal finance proposals

- TDS rate on the tax portion of EPF withdrawals in non-PAN cases will be reduced from 30% to 20%

- The government has increased the limit for exemption on leave encashment on retirement of non-government salaried employees from Rs 3 lakh to 25 lakh.

- Deduction from capital gains on investment in residential house under Section 54 and 54F will be capped at Rs 10 crore to deter the huge claims made by high-net-worth assesses under these provisions.

- The government will establish an integrated IT portal for investors to reclaim unclaimed shares and dividends from the Investor Education & Protection Fund Authority with ease.

Overall, in terms of personal finance the announcements in the Union Budget 2023-24 brought some tax relief for the common man, especially those looking to opt for the new tax regime. However, certain expectations of the common man such as affordable health insurance, higher deduction on home loan interest, and LTCG exemption on equities were overlooked by the government.

This article first appeared on PersonalFN here

{kind=link}