The year 2022 has been a difficult year for global equity markets. With the risk-off trade largely playing out all around the year, major global equity indices struggled. But despite the challenging situation, particularly in the first half of 2022 (with COVID-19 cases, Russia’s invasion of Ukraine, the supply chain disruptions, inflation spiralling, and then central banks indulging in monetary tightening), the Indian markets did exceptionally well on a relative basis. In fact, India was one of the few large markets that posted positive returns in 2022.

Table 1: India outperformed its global peers in 2022

| Index | % Change in 2021 | % Change in 2022* |

| Bovespa | -11.9 | 0.2 |

| CAC 40 | 28.9 | -7.0 |

| DAX | 15.8 | -9.9 |

| FTSE 100 | 14.3 | 0.8 |

| Hang Seng | -14.1 | -16.8 |

| Jakarta Composite | 10.1 | 2.3 |

| Nikkei 225 | 4.9 | -3.3 |

| RTS Index | 15.0 | -31.8 |

| S&P 500 | 26.9 | -16.3 |

| S&P BSE SENSEX | 22.0 | 7.3 |

| Shanghai Composite | 4.8 | -12.7 |

*Data as of 13th December 2022

(ACE MF, PersonalFN Research)

The major reasons behind India’s outperformance are:

-

– Significant ease in COVID-19 restrictions thus promoting economic activity (Thanks to a higher –inoculation rate and reduced number of new cases)

-

– Reforms consciously being implemented by the government

-

– Sizeable Foreign Direct Investments (FDI) investments made in India

-

– Companies growing organically and inorganically

-

– Encouraging growth in the topline and bottomline of companies

-

– Buoyant core sector growth (due to higher public and private sector capex spending)

-

– A health credit offtake (at 17.2% in September 2022 v/s 7.0% a year ago)

-

– And the fact that India is currently one the fastest growing major economies of the world with a demographic dividend.

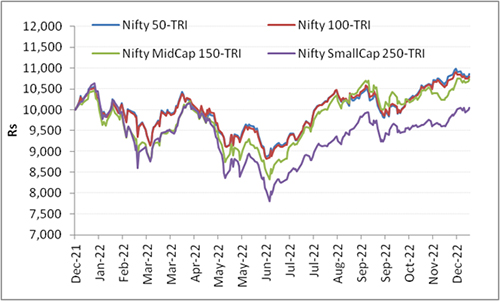

Graph: Leading indices bounced back sharply in H2CY22

Base = Rs 10,000

Data as of 13th December 2022

(ACE MF, PersonalFN Research)

As a result, the leading indices bounced back sharply after June 2022, and with that, the Passive Funds stood to benefit not just in terms of returns but even inflows. The Assets Under Management (AUM) of index funds and other Exchange Traded Funds (ETFs), barring Gold ETFs, as a percentage of the total AUM of open-ended funds, jumped from 11.6% in December 2021 to 15.6% in November 2022, according to AMFI (Association of Mutual Funds in India) data. Moreover, the scheme counts of index funds and ETFs barring gold ETFs also increased from 173 in December 2021 to 283 in November 2022

However, at a time when Passive Funds have been attracting investors, Active Funds seem to have struggled badly.

At PersonalFN we evaluated the performance of 258 actively managed equity schemes spanning across eleven sub-categories. We also analysed 153 Passive Funds to make a fair comparison. And our findings might surprise many of you…

Table 2: Performance of Active Funds and Passive Funds in 2022

| Category | Absolute (%) | CAGR (%) | % of schemes outperformed relative to benchmark index | Risk-Ratios | |||||

| 6 Months | YTD | 3 Years | 5 Years | On YTD Returns | 3-yr Returns | Std. Dev | Sharpe | Sortino | |

| All Active Funds | |||||||||

| Large Cap Fund | 18.8 | 6.0 | 16.1 | 12.5 | 23 | 29 | 20.77 | 0.17 | 0.27 |

| Large & Mid Cap Fund | 19.9 | 5.9 | 20.2 | 13.0 | 35 | 31 | 22.82 | 0.21 | 0.32 |

| Flexi Cap Fund | 18.7 | 4.3 | 18.5 | 13.0 | 21 | 30 | 20.48 | 0.19 | 0.31 |

| Multi Cap Fund | 21.1 | 8.5 | 22.5 | 14.8 | 47 | 47 | 18.47 | 0.26 | 0.31 |

| Focused Fund | 18.8 | 5.4 | 18.3 | 12.3 | 35 | 38 | 20.88 | 0.21 | 0.34 |

| Mid Cap Fund | 20.5 | 6.8 | 25.4 | 13.7 | 34 | 34 | 20.87 | 0.21 | 0.32 |

| Small cap Fund | 20.0 | 5.3 | 33.7 | 14.6 | 79 | 71 | 25.81 | 0.29 | 0.45 |

| Value Fund | 21.3 | 9.9 | 20.9 | 11.4 | 53 | 47 | 22.12 | 0.18 | 0.28 |

| Contra Funds | 22.1 | 12.1 | 24.5 | 15.1 | 67 | 67 | 23.18 | 0.25 | 0.37 |

| Dividend Yield Fund | 17.2 | 6.7 | 21.6 | 12.2 | 44 | 56 | 19.66 | 0.24 | 0.39 |

| ELSS Fund | 19.3 | 6.1 | 18.5 | 12.2 | 37 | 34 | 22.36 | 0.18 | 0.27 |

| All Index Funds | |||||||||

| S&P BSE Sensex Index Funds | 18.8 | 8.4 | 16.0 | 14.5 | – | – | 21.79 | 0.16 | 0.24 |

| Nifty 50 Index Funds | 18.4 | 7.3 | 16.7 | 13.6 | – | – | 21.45 | 0.16 | 0.26 |

| Nifty 50 Equal Weight Index Funds | 19.3 | 10.1 | – | – | – | – | 16.53 | 0.12 | 0.24 |

| Nifty 100 Index Funds | 17.6 | 4.7 | 16.5 | – | – | – | 18.40 | 0.10 | 0.17 |

| NIFTY 100 Equal Weight Index Funds | 16.6 | 5.1 | 17.2 | 10.5 | – | – | 21.23 | 0.13 | 0.21 |

| Nifty Next 50 Index Funds | 19.1 | 4.3 | 16.3 | 8.6 | – | – | 20.09 | 0.11 | 0.19 |

| NIFTY Large Mid Cap 250 Index Funds | 20.1 | 7.2 | – | – | – | – | 19.07 | 0.04 | 0.08 |

| Nifty Midcap 150 Index Funds | 20.1 | 6.8 | 26.1 | – | – | – | 15.23 | 0.14 | 0.20 |

| Nifty Smallcap 50 Index Funds | 15.0 | – | – | – | – | – | 25.20 | -0.21 | -0.30 |

| Smallcap 250 Index Funds | 19.7 | -0.2 | 27.8 | – | – | – | 19.72 | 0.63 | 0.75 |

| Nifty 500 Index Funds | 19.0 | 6.9 | 18.2 | – | – | – | 22.91 | 0.19 | 0.27 |

| Benchmark Indices | – | – | |||||||

| S&P BSE SENSEX – TRI | 19.0 | 8.7 | 16.4 | 14.9 | – | – | 22.77 | 0.17 | 0.25 |

| NIFTY 50 – TRI | 18.7 | 8.6 | 16.8 | 14.2 | – | – | 22.78 | 0.17 | 0.26 |

| NIFTY50 Equal Weight – TRI | 19.8 | 10.8 | 21.9 | 13.1 | – | – | 23.36 | 0.22 | 0.33 |

| NIFTY 100 – TRI | 18.6 | 7.9 | 16.8 | 13.5 | – | – | 22.65 | 0.17 | 0.25 |

| Nifty100 Equal Weight – TRI | 17.1 | 5.6 | 18.9 | 10.5 | – | – | 23.41 | 0.18 | 0.28 |

| NIFTY NEXT 50 – TRI | 19.3 | 4.7 | 17.0 | 9.3 | – | – | 23.33 | 0.16 | 0.24 |

| Nifty Midcap 50 – TRI | 23.2 | 8.3 | 26.1 | 13.0 | – | – | 28.62 | 0.23 | 0.36 |

| Nifty Midcap 150 – TRI | 22.2 | 7.3 | 26.4 | 13.3 | – | – | 25.91 | 0.25 | 0.37 |

| NIFTY LargeMidcap 250 – TRI | 20.4 | 7.7 | 21.6 | 13.5 | – | – | 23.83 | 0.22 | 0.31 |

| Nifty Smallcap 250 – TRI | 20.1 | 0.5 | 28.9 | 8.8 | – | – | 30.48 | 0.25 | 0.36 |

| NIFTY 500 – TRI | 19.3 | 7.3 | 18.9 | 13.1 | – | – | 23.18 | 0.19 | 0.28 |

*Performance as of 13th December 2022. Category average returns are considered for the respective sub-categories. Returns are Point to Point and in %, calculated using the Direct Plan-Growth option

Outperformance within passively managed schemes hasn’t been considered since that’s not their objective

Past performance is not an indicator of future returns. Speak to your investment advisor for further assistance before investing. Mutual Fund investments are subject to market risks. Read all scheme-related documents carefully.

(Source: ACE MF, PersonalFN Research)

Amongst the actively managed mutual fund schemes, the Smallcap Funds and Value Funds have outperformed their respective benchmark indices on YTD return as well as a 3-year return basis. Out of 24 Smallcap Funds, 19 on a Year-to-Date (YTD) basis and 17 on a 3-year basis generated superior returns vis-a-vis their benchmarks.

Bank of India Small Cap Fund, Canara Robeco Small Cap Fund, Quant Small Cap Fund and Nippon India Small Cap Fund were amongst the few schemes that by far outperformed on YTD returns as well as 3-year returns.

Amongst the Value Funds, ICICI Prudential Value Discovery Fund and HDFC Capital Builder Value Fund outshone their benchmark indices.

Many of the outperforming Active Funds maintained balanced exposure to growth and value stocks and many of them participated in PSU and defence sector rallies. Their nimble approach helped them capitalise on opportunities under volatile market conditions.

However, barring some Smallcap Funds, Contra Funds and Value Funds, all other sub-categories of Active Equity Funds have disappointed investors (especially Largecap Funds), and not even half the schemes could outperform their respective benchmark indices.

Why did Active Funds, especially the Largecap Funds underperformed on YTD as well on 3-year returns?

Well, leaving aside a few exceptions, the index-heavy stocks didn’t fare well in 2022. In other words, the rally was driven by a handful of stocks. The heavyweight IT stocks, which were the frontrunners in 2021, disappointed in 2022. So, the actively managed equity funds that failed to reduce their exposure to heavyweight IT companies within a few months of 2022, took a beating later.

Similarly, the merger-bound HDFC twins — HDFC Ltd and HDFC Bank — also remained under pressure (after a short rally post the merger announcement). On the other hand, some of the PSU banks and other private banks fared exceptionally better. Also, many mutual funds missed rallies in FMCG companies such as ITC.

Plus, some mutual funds barring a few Adani stocks, preferred to sit out of the other companies in the Adani pack. Hence, all in all, those Active Equity funds that owned the performing stocks of 2022 in the portfolio fared better, while those that didn’t, lagged on returns.

The top-5 Nifty-50 stocks have a weightage of 41% in the index, of which Reliance alone accounts for more than 10%. As you might be aware, mutual funds usually prune down their single stock exposure if it crosses above 10% even on account of appreciation. Thus, all these factors together resulted in a noticeable underperformance of largecap funds.

Only a handful of largecap funds-ICICI Prudential Bluechip Fund, Baroda BNP Paribas Large Cap Fund and Nippon India Large Cap Fund outperformed their respective benchmark indices on YTD as well as 3-year returns.

Flexicap Funds have also performed equally poorly in 2022 so far. Apart from stock-specific rallies in largecaps, contrasting market conditions in H2CY22 vs in H1CY22 seem to have affected their performance. Just 7 out of 33 schemes generated better returns than the benchmark on a YTD basis and 10 schemes managed to beat the benchmark on a 3-year return criterion. Quant Flexi Cap Fund, HDFC Flexi Cap Fund and Franklin India Flexi Cap Fund remained clear outperformers in the category.

The other sub-categories of actively managed equity mutual fund schemes also put up a lacklustre show with about 3 funds out of every 5 underperforming.

Our analysis of scheme-specific outperformance revealed even more crucial information. The mutual fund houses that remained cautious of valuations, refrained from the last year’s frenzy in tech stocks and took a selective exposure to Initial Public Offerings (IPOs), and more importantly, participated in sectors/companies that demonstrated better on-ground performance in 2022, did better.

On the other hand, the underperforming funds seem to have left too much to their fate and failed to show agility. So the takeaway point is, not all actively managed equity funds are alpha generators.

How should you approach the equity markets in 2023?

It’s noteworthy that the history of the Indian equity market stands testimony to the fact that after negative events such as the downturn of 2002, the U.S. subprime mortgage crisis of 2008-09, the Dubai debt debacle of 2009-10, and later the debt crisis in Greece, the slowdown in China in 2016, and the crash at the onset of the COVID-19 pandemic in 2020; the Indian equity markets have well trounced supported by buying activity from investors. A good thing this time is that there is positive participation from retail and domestic investors-and Indian equity markets are not just dependent on foreign flows.

Active Funds or Passive Funds — Which Ones Should Invest in 2023?

Passive Funds might continue to gain popularity in 2023 on the backdrop of challenging market conditions. Equity-oriented Passive Funds that offer you low-cost options to generate index-like returns may have a role to play in your portfolio. But that doesn’t mean you should completely avoid actively managed equity funds.

[Read: 7 Best Mutual Funds to Invest in 2023]

If your investment objective is wealth creation, want to generate alpha returns (i.e. outperform the benchmark index) want to beat inflation, have a high-risk appetite, have long-term financial goals to address, and have a sufficient time horizon (at least 5 years) before the envisioned goals befall, investing in some the best-diversified equity funds in line with your asset allocation model would be sensible. But you need to follow a prudent approach to build a portfolio of actively managed equity mutual funds.

To invest in actively managed equity-oriented mutual funds at this juncture, I recommend following the Core & Satellite approach, a time-tested investment strategy followed by some of the most successful equity investors.

The term ‘Core’ applies to the more stable, long-term holdings of the portfolio, while the term ‘Satellite’ applies to the strategic portion that would help push up the overall returns of the portfolio across market conditions.

The ‘Core’ holding should comprise around 65-70% of your equity mutual fund portfolio and consist of a Large-cap Fund, Flexi-cap Fund, and a Value Fund/Contra Fund. Whereas the ‘Satellite’ holdings of the portfolio can be around 30-35%, comprising a Mid-cap Fund, a Large & Mid-cap Fund, and an Aggressive Hybrid Fund.

When you construct a Core & Satellite portfolio of equity mutual funds, make sure you do not end up over-diversifying the portfolio. Select no more than 7 to 8 best equity schemes.

This article first appeared on PersonalFN here

{kind=link}