For the first time since the formation of the six-member Monetary Policy Committee (MPC) in 2016, the Reserve Bank of India (RBI) has missed its inflation target in 2022. Thus, the RBI owed a detailed explanation to the government on this subject.

The RBI, through a press release dated October 27, 2022, had called for an additional meeting of the MPC on November 3, 2022, citing Section 45ZN of the Reserve Bank of India (RBI) Act 1934, Regulation 7 of the RBI MPC and Monetary Policy Process Regulation, 2016.

Section 45ZN describes the process RBI needs to follow in case it fails to achieve its inflation target.

Graph 1: CPI inflation – Actual v/s Projected

(Source: RBI Bulletin, October 2022; data as of the last three quarters)

Despite increasing its policy repo rate, the RBI has been consistently missing its own estimates on CPI inflation — the actual reading has been coming higher.

For September 2022, CPI inflation once again fastened to 7.41% from 7% in the previous month due to higher readings reported by food, fuel & light, clothing & footwear, health, transport & communication, and education. Thus, core inflation, which excludes food, fuel & light inflation, has also remained sticky (around 6.30%).CPI or retail inflation in India has stayed constantly above 6%-the upper end of RBI’s target-for the past three quarters.

Why is CPI inflation remaining elevated?

The RBI has observed that the key risks to the domestic inflation trajectory are emanating from…

-

High and protracted uncertainty surrounding the geopolitical conditions

-

Supply disruptions

-

Rising risk of recession in advanced economies

-

The risk of crop damage from excessive/unseasonal rains

-

Highly uncertain outlook for crude oil (due to geopolitical developments)

-

Appreciating USD

-

Elevated imported inflation pressures

-

Pass-through of input costs across manufacturing, services, and infrastructure firms

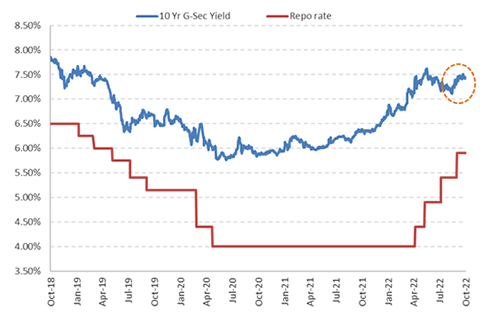

Graph 2: The 10-year benchmark yield has hardened

CPI Inflation data as of September 2022, Repo rate as of October 31, 2022

(Source: MOSPI, RBI, PersonalFN Research)

As a result, the 10-year benchmark G-sec yield has hardened by 55 basis points since April 2022, while the policy repo rate has been increased by 190 basis points to tame the inflation beast by the RBI.

Going forward, the yield curve will be shaped by how inflation moves, the magnitude of rate hikes, whether India can control its debt-to-GDP ratio, and fiscal deficit. In the near-term upward pressure on the benchmark, yield looks inevitable.

What happened at the additional MPC meeting?

As anticipated, the RBI didn’t follow the U.S. Federal Reserve’s (Fed’s) or the European Central Bank’s (ECB’s) footsteps at its unscheduled meeting. These central banks of the advanced economies had hiked the interest rates by 75 basis points a day or two before the MPC meeting.

The RBI MPC, in its meeting yesterday, mainly discussed and provided an ‘inflation report’ explaining the possible reasons to the government for failing to keep inflation within the 2-6% mandate and the corrective measures necessary to do so. The exact details of the letter or note sent to the government were not released to the media; it remained a bi-party communication, at least for now. The details of the report and the government’s response thereof would be known to the public only in the future.

That said, a series of past events, interviews of RBI officials, and minutes of meetings of MPC have enough hints as to what RBI might have said in the report.

At present, Russia’s invasion of Ukraine, the subsequent embargo on Russia’s energy exports by the western countries, and production cuts by the OPEC+ nations have collectively exacerbated the inflationary pressure, not just in India but even elsewhere. With chilling winters approaching the northern hemisphere, the developments in the energy markets will be crucial. China’s zero-covid-policy-induced-lockdowns resulted in supply chain disruptions, thereby making inflation more of a structural issue globally.

The situation in India doesn’t look as alarming, although the emerging data on inflation requires careful monitoring.

Will RBI continue to raise policy rates further?

The RBI is focusing on the withdrawal of its accommodative stance (which it took amid the COVID-19 pandemic) to ensure that inflation remains within the target going forward while supporting growth.

The minutes of the last bi-monthly monetary policy held in September 2022 state that the monetary policy would remain watchful and nimble, based on incoming data and evolving conditions — mainly inflation (while strengthening our macroeconomic fundamentals).

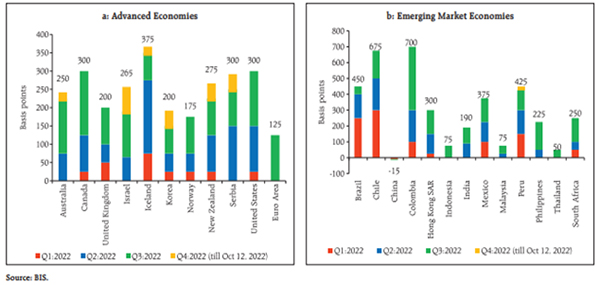

Graph 3: Synchronised monetary policy tightening by central banks

(Source: RBI Bulletin, October 2022)

In the west, given that the U.S. Federal Reserve, the European Central Bank (ECB), and the Bank of England (BOE) have all once again raised rates recently by 75 bps to tame multi-decade high inflation, it appears that RBI too may take similar actions. We might see a few more rate hikes in the current cycle of monetary tightening before central banks turn neutral. Markets are already accounting for a 35-50bps rate hike in December bi-monthly meeting.

The impact on debt mutual funds…

It appears that we are very much in an interest rate upcycle. If inflation continues to play a spoiler, central banks may not pause raising interest rates. The longer end of the yield curve, in such a scenario, may witness some volatility in the near term, thus impacting longer-maturity debt funds.

On the other hand, debt funds that invest in the short-maturity segment witness minimal mark-to-market impact as interest rates rise.

What strategy debt funds investors should follow going forward?

You will be better off deploying your hard-earned money at the shorter end of the maturity cover.

However, given that markets have already priced in an aggressive rate hike, you could gradually start looking at duration funds with a long-term view and take a calculated risk.

If you have a 2 to 3 years investment horizon, you may consider investing in a mix of safely managed Dynamic Bond Funds, Banking & PSU Debt Funds, and Corporate Bond Funds. However, it will be best to invest in these debt mutual funds in a staggered manner. You may consider setting aside some funds in a pure Liquid Fund and gradually scaling up your investments in medium to long-duration funds after every rate hike by RBI.

This way, you would be able to gradually build a long-term debt mutual fund portfolio as well as minimise the interest rate risk when the yields are trending upwards.

[Read: Is it the Right Time to Invest in Dynamic Bond Funds? Know Here…]

On the other hand, if your investment horizon is up to or less than a year and you want to be exposed to less risk, strictly stick to the best Liquid Funds with minimal or zero exposure to Certificate of Deposits (CDs) and CPs.

When you invest in debt mutual funds, remember that returns are not guaranteed. It is important to understand the various risk involved, viz. interest rate risk and credit risk, before selecting a debt mutual fund for your portfolio; avoid selecting schemes based on their recent performance.

To select the best debt mutual fund scheme/s within each category, check the following:

-

✔ The credit quality of the underlying securities

-

✔ The average maturity profile

-

✔ The historical performance

-

✔ The risk ratios

-

✔ The investment processes & systems at the fund house

And always align your investments in mutual funds with your risk profile, broad investment objective, financial goals, and the time in hand to achieve those goals.

This article first appeared on PersonalFN here

{kind=link}