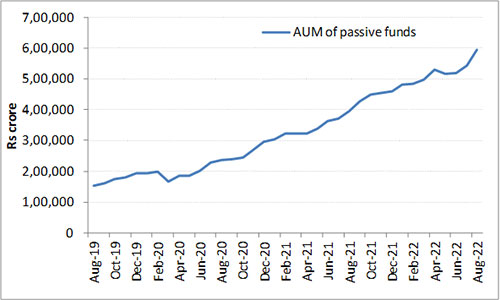

The popularity of passive funds in India has been on the rise. The Assets Under Management (AUM) of passive funds, including gold ETFs, have jumped nearly four times over the last three years—from just Rs 1.5 lakh crore in August 2019 to Rs 5.9 lakh crore in August 2022.

Graph 1: The Rising AUM of Passive Funds

Data as of August 31, 2022

(Source: AMFI, PersonalFN Research)

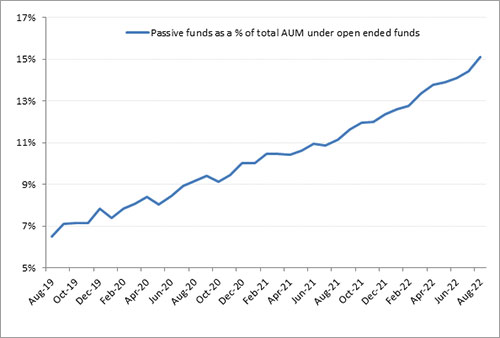

But absolute numbers may not reflect an accurate picture. Thus, before we discuss the potential reasons for such a massive jump in the AUM of passive funds, let’s understand where they stand in relative terms (as a percentage of AUM of open-ended funds).

Chart 2: Passive funds are gaining prominence…

Data as of August 31, 2022

(Source: AMFI, PersonalFN Research)

Graph 2 depicts that the AUM of passive funds as a percentage of the total AUM of all open-ended funds has jumped from 7% in August 2019 to 15% in August 2022. That confirms that passive funds are on a song, gaining all the attention of Indian investors.

However, in the global context, they are still in an early stage of progress. For instance, passive funds account for nearly 16% of the total market cap of companies listed in the U.S. In India, the AUM of passive funds still forms only about 2% of India’s total listed market capitalisation.

Nonetheless, the rapid growth of passive funds-whether through Index Funds or Exchange Traded Funds (ETFs)-is a positive and an early indicator of maturing markets.

For those of you who aren’t aware of passive funds, they are a type of mutual fund that simply mimic their benchmark indices without any intention to generate alpha. That said, it still offers diversification through exposure to a range of securities across sectors within the respective index.

In other words, passive funds generate returns that are in line with their respective benchmark index at best but can’t outperform them under ideal conditions. This is because passive funds aren’t actively managed. The fund manager passively manages the portfolio by seeking to replicate the underlying benchmark, thereby reducing the fund manager’s involvement or any behavioural biases.

Further, the expense ratios of passive funds are extremely competitive compared to active funds, where the day-to-day involvement of the fund manager in handling the scheme is high. Also, their risk quotient is better: they aren’t exposed to risks associated with being overweight or underweight in a particular sector/theme/security.

Passive funds come in different genres—Index Funds, Exchange Traded Funds (ETFs), speciality-based index funds/ETFs, and Fund-of-Funds investing in index funds/ETFs.

Moreover, they can be distinguished by their target asset classes. For instance, gold ETFs aim to track the movement of gold prices. Whereas an ETF based on the Nifty 50 will primarily align itself with the Nifty 50 index, and so on.

So why do investors prefer passive funds and settle for average performance rather than going with active funds, which hold the potential to outperform their benchmark index?

Many of you might conclude that the underperformance of active funds against their respective benchmarks could be the primary reason for investors to chase passive funds. Well, to an extent it’s true but not entirely.

The table below depicts, broadly, how various categories of mutual funds fared over various time periods. Barring large-cap funds, all other categories have convincingly outpaced equity-oriented passive funds.

Table: Passive funds vs. active funds – how have they fared?

| Category Average | Returns (Absolute %) | Returns (CAGR %) | |||

| 1 Year | 2 Years | 3 Years | 5 Years | 7 Years | |

| Small-cap Fund | 12.4 | 46.2 | 35.0 | 16.1 | 18.0 |

| Mid Cap Fund | 10.4 | 38.3 | 28.8 | 14.8 | 16.2 |

| Contra Funds | 11.6 | 36.0 | 25.7 | 15.3 | 16.4 |

| Multi Cap Fund | 8.3 | 36.1 | 25.0 | 15.3 | 15.7 |

| Large & Mid Cap | 7.2 | 32.4 | 22.9 | 13.1 | 15.0 |

| Dividend Yield | 7.8 | 31.3 | 22.3 | 12.0 | 14.0 |

| Value Fund | 8.0 | 33.0 | 21.9 | 11.2 | 14.0 |

| Flexi Cap Fund | 5.4 | 29.4 | 21.4 | 12.9 | 14.3 |

| Focused Fund | 5.4 | 28.6 | 21.1 | 12.8 | 14.7 |

| Index Funds – Nifty Next 50 | 5.3 | 28.2 | 19.7 | 9.5 | 13.2 |

| Index Funds – Nifty | 3.7 | 26.6 | 18.9 | 13.1 | 13.5 |

| Large Cap Funds | 3.9 | 26.3 | 18.8 | 12.0 | 13.2 |

| Index Funds – Sensex | 4.1 | 25.2 | 18.3 | 14.2 | 13.8 |

| NIFTY 50 – TRI | 4.7 | 26.7 | 19.2 | 13.6 | 14.1 |

| NIFTY 100 – TRI | 5.2 | 27.2 | 19.5 | 13.2 | 14.1 |

| Nifty Midcap 150 – TRI | 12.1 | 39.4 | 29.5 | 14.8 | 17.7 |

| Nifty Smallcap 250 – TRI | 6.5 | 42.3 | 29.2 | 9.9 | 14.0 |

| NIFTY 500 – TRI | 6.4 | 29.9 | 21.5 | 13.2 | 14.6 |

Data as of September 12, 2022

(Source: ACE MF, PersonalFN Research)

What are the reasons for inflows in passive funds?

At PersonalFN, we dug deeper to know the key reasons behind the success of passive funds.

Reason #1: EPFO has been the main driver behind the growth of passive funds

Our scheme-level AUM analysis revealed the primary reason. SBI Nifty 50 ETF, SBI S&P BSE Sensex ETF, UTI Nifty 50 ETF, and UTI S&P BSE Sensex ETF together accounted for 51% (Or Rs 2.82 lakh crore) of the total AUM under equity-oriented passive funds as of August 31, 2022. Nearly 75%-80% of the AUM in aforesaid schemes has come from the Employees’ Provident Fund Organisation (EPFO). EPFO has around 6 crore subscribers and manages an AUM of nearly Rs 15 lakh crore. It invests 15% of its AUM in equity markets through the ETF route.

EPFO is taking the safest available route to invest up to 15% of the retirement savings of its subscribers in equity markets. Index ETFs are cost efficient (For example, the SBI Nifty 50 ETF has an expense ratio of 0.07%) and eliminate the risks of underperformance associated with active fund management.

The growth of passive funds hasn’t come at the expense of active funds.

Reason #2: Jump in the retail Demat accounts is at play

During the coronavirus pandemic, India’s financial services sector received a booster dose of digitalisation, resulting in a massive surge in new demat accounts. From just 4 crore during pre-pandemic times, total demat accounts in India have climbed to 10 crore today.

To prioritise passive investing, mutual funds started developing a variety of themes and new investment strategies in the passive space. Several New Fund Offers (NFOs) of Index Funds, ETFs, and speciality Index Funds/ETFs were launched — and even now, fund houses are launching passive funds amidst volatile market conditions.

Reason #3: Change in SEBI norms for passive funds, making them an entry-level proposition

The minimum subscription to invest in passive funds is affordable. This has resulted in passive funds formally finding their way into the portfolios of many retail investors in recent years. Nowadays, passive funds are promoted as entry-level products. They are easy to sell, especially without any help from intermediaries. If fund houses manage to keep their fund expenses under check and match the performance of their benchmarks without much tracking error, passive funds don’t need much convincing.

International experience tells us the same story. In the U.S., even a fund house such as Fidelity, which dominated the space of active funds for decades, has launched zero-cost index ETFs as entry-level products.

What is the future of passive funds?

Formalisation of employment, i.e., more people joining organisations coming under the purview of PF rules, will continue to drive the AUM growth of passive funds.

Moreover, as the Indian markets mature over the years and mutual fund houses launch more innovative products based on passive strategies, passive funds might witness impressive growth. Passive strategies are likely to offer more portfolio diversification avenues to Indian investors.

That said, active investing might still remains the growth driver for the Indian mutual fund industry, at least for another decade. This is because the mindset or expectations of most investors is not just to clock returns in line with the respective benchmark index but also to outperform, i.e., generate alpha, which may enable beating inflation better and accomplishing the envisioned financial goals sooner.

So, should you consider investing in active funds or passive funds?

For a novice investor who does not possess the knowledge on how to choose amongst actively managed mutual fund schemes, or simply expects the benchmark returns, then ‘Passive mutual Funds’ may be a worthwhile choice.

But if you are looking to beat the benchmark index and potential earn better real returns (also known as inflation-adjusted returns), an active fund is certainly a better choice. Active investing is still relevant in this day and age of intensified volatility and macroeconomic risk alongside geopolitical uncertainty. A fund manager of a worthy well-diversified open-ended equity fund that follows robust investment processes and systems may help mitigate the downside risk better compared to the broader benchmark index. Over the long-term, it is the active funds that have rewarded investors better compared to passive funds.

What matter is how you select mutual fund schemes for your portfolio. You must diversify the portfolio across sub-categories and investment styles, assess a host of quantitative and qualitative parameters to select mutual funds, avoid giving much importance to short-term performance, avoid timing the market, preferably take the SIP route, focus on time in the market, your asset allocation, besides consider your risk profile, broader investment objective, financial goals and time in hand to achieve those goals.

[Read: Steps to Build a Passive-only Portfolio for Risk-averse Investors]

If you want to make the most of available investment options, carefully build a mutual fund portfolio of both active and passive funds.

This article first appeared on PersonalFN here

{kind=link}