Globally, we are in a QT (Quantitative Tightening) phase. Between March 2022 and July 2022, the U.S. Federal Reserve (Fed) hiked interest rates by 225 bps (basis points).

Interestingly, the U.S. Fed was extremely gradual with its rate hikes during the last QT cycle. Fed took three years (from 2015 to 2018) to hike policy rates by 225 bps in the previous cycle. But this time, the rate hikes have come on the backdrop of a record high inflation and overheating of the U.S. economy.

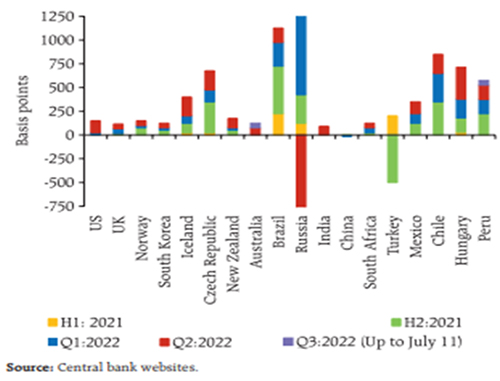

Graph 1: Rate Actions of Central Banks of Select Countries since 2021

(Source: RBI Bulletin, July 2022)

It’s not just the U.S. Fed that has turned hawkish in its monetary policy actions. Many other major central banks around the world, have raised rates remarkably ramping up their fight against inflation. Speaking about the timing of response, some central banks have proactively raised rates, while a few have been behind the curve.

In the Emerging market economies, India witnessing high inflation and envisaging the spillover effects of the policy actions in the west, aligned its monetary policy actions well.

So far, the RBI has increased the policy rates by good 140 bps, thus effectively placing the repo rate currently at 5.40%.

Further, the RBI’s six-member Monetary Policy Committee (MPC) has decided to remain focused on the withdrawal of accommodation to ensure that inflation remains within the target going forward while supporting growth. These decisions are in consonance with the objective of achieving the medium-term target for CPI inflation of 4% within a band of +/- 2% while supporting growth.

The RBI expects the full-year inflation projection for FY23 at 6.7% (with Q2 at 7.1%; Q3 at 6.4%; and Q4 at 5.8%, and risks evenly balanced). This is based on the assumption of a normal monsoon in 2022 and that the average crude oil price (Indian basket) would be around US$ 105/barrel. Any deviation in the actual performance of these two variables remains an upside threat to inflation.

Also, the key risk to the inflation trajectory according to the RBI are:

-

– Spillover from the geopolitical shocks

-

– The appreciation in the U.S. Dollar, resulting in imported inflation

-

– Cost pressures from output prices across the manufacturing and services sectors

It’s noteworthy that cooking gas prices have shot up 30% over the last 1 year and such steep hikes can often make inflation structural and enduring.

Although the food and metal prices have started coming off from their peak in the international markets, they still remain elevated as compared to their pre-covid levels.

For the first quarter of the next fiscal year i.e. 2023-24, the RBI has projected CPI inflation to be at 5.0%.

Where are we in the interest rate cycle?

No two interest rate cycles look identical but how far rates can go up in a cycle primary depends on three factors: 1) how low the rates in the previous cycle went, 2) the trajectory of inflation, and 3) the overall growth trends.

For instance, in the aftermath of the global financial crisis of 2008, policy rates in India nosedived from 9% in July 2008 to 4.75% in April 2009. As the global economy recovered in 2010, policy rates started going up steadily from March 2010 onwards. By October 2011, the repo rate jumped to 8.5%–an aggregate increase of 375 bps.

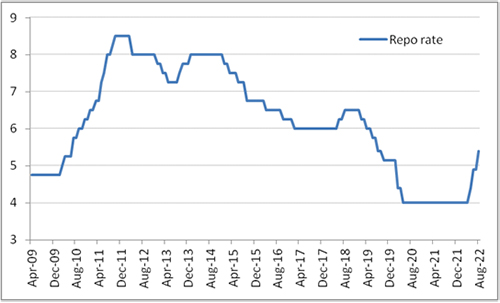

About a decade later, i.e. in April 2020 policy rates hit the rock bottom of 4% on the onset of the COVID-19 pandemic. At present, the policy rates stand at 5.4% and the yield on 10-year G-sec yield is hovering at around 7.30%.

Graph 2: RBI policy rate movement over the years

Data as of August 2022

(Source: RBI, PersonalFN Research)

At the press conference post monetary policy action meeting held earlier this month, the RBI Governor refrained from offering any future guidance on policy rates. However, it is clear from the withdrawal of the accommodative policy stance, that controlling inflation will be the primary policy objective going forward.

It is evident that we are interest rate upward cycle. However, given the fact that very recently inflation is off from its peak, RBI may reduce the pace of interest rate hikes in the upcoming rounds of MPC meetings. That said, the policy repo rate may go up by another 35 to 60 bps in the current calendar year (before shifting to an extended pause), going by the expectations of most economists.

Which type of debt funds should you invest in now?

In a rising interest rate scenario, it makes sense for investors to look at the shorter end of the yield curve. This is because the short maturity segment witnesses a minimal mark-to-market impact when interest rates rise.

On the other hand, funds focusing on longer duration instruments that have an average maturity typically in a range of 5 to 10 years are highly vulnerable to interest rate risk. These funds may witness high volatility in the near term.

Therefore, you will be better off deploying your hard-earned money in shorter-duration debt mutual funds such as pure Liquid Funds.

[Read: 3 Best Liquid Mutual Funds to Invest in 2022]

For a period less than or up to a year, you consider investing in Parag Parikh Liquid Fund or Quantum Liquid Fund in the liquid fund category for the said short-term time horizon. These are some of the top performers*. Parag Parikh Liquid Fund held 90.9% of its portfolio in sovereign-rated instruments, 1.4% in CDs and CPs, and the balance in cash and equivalents, as of July 31, 2022.

Quantum Liquid Fund also lays high emphasis on safety, investing predominantly in high-rated Government and Quasi-Government securities, and resists holding any exposure to instruments issued by private entities.

If you have a long-term investment horizon, you may consider investing in a mix of safely managed Banking & PSU Debt Funds, and Corporate Bond Funds.

If you are a moderate risk taker and have an investment horizon of 2 to 3 years, you may consider Banking & PSU Debt Funds such as IDFC Banking & PSU Debt Fund and Axis Banking & PSU Debt Fund. These are some of the best-performers* in the Banking and PSU Debt Fund category.

IDFC Banking & PSU Debt Fund allocated 85.4% of its assets to the high-quality securities issued by PSUs, Banks, and PFIs, with another 9.1% in government securities, as of July 31, 2022. Likewise, Axis Banking & PSU Debt Fund portfolio is primarily exposed to top-rated bonds issued by Banks and PFIs, along with significant exposure to PSU bonds.

You can also consider adding safely managed Corporate Bond Funds such as Aditya Birla SL Corporate Bond Fund, — one of the top-performers* — that holds exposure to top-rated debt instruments, provided you do not mind taking slightly higher risk. The fund predominantly invests in debt securities issued by private sector players but has been following a conservative approach. As of July 31, 2022, it held 62.4% of its assets in AAA-rated corporate debt instruments and 29.2% in government securities. It had just 4.2% exposure to securities rated below ‘AAA’ and no exposure to securities rated below ‘AA’.

*Please note, the aforementioned top performing funds in the respective categories are as per past returns and are NOT a recommendation. Past performance is not an indicator of future returns. Speak to your investment advisor for further assistance before investing. Mutual Fund investments are subject to market risks. Read all scheme-related documents carefully.

It may be wise to invest in these debt mutual funds in a staggered manner. You may want to set aside some funds in a pure Liquid Fund and gradually scale up your investments in medium to long-duration funds after every rate hike by RBI. This way, you will be able to gradually build a sensible debt mutual fund portfolio, which minimises the interest rate risk when the yields are trending upwards.

Always, assess your risk appetite and investment time horizon while investing in debt funds. And prefer the safety of principal over returns. Remember, investing in debt funds, is not risk-free.

Happy Investing!

This article first appeared on PersonalFN here