Debt mutual funds are schemes that predominantly invest in fixed-income generating instruments such as corporate bonds, government bonds, certificates of deposits, treasury bills, etc. These funds aim to provide diversification and stable returns as they are less volatile compared to equity mutual funds.

The prevailing interest rate environment is one of the most crucial factors that affect the performance of a debt mutual fund. Apart from this, the credit quality and the maturity of the underlying securities in the portfolio can impact their returns.

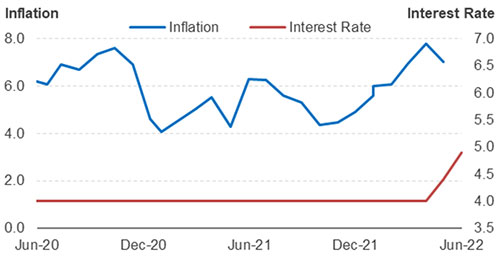

Currently, we are witnessing a rising interest rate scenario as central banks across the globe, including India, have been raising policy rates aggressively to control spiralling inflation.

In India, the CPI inflation has breached the RBI’s upper tolerance limit for the fifth straight month, mainly because of higher food and fuel inflation.

Graph 1: CPI inflation versus Repo Policy Rate

Repo policy rate as of June 2022, CPI inflation as of May 2022

(Source: RBI, MOSPI)

Even in the US, retail inflation hit a 40-year high of 8.6% in May 2022, causing the Federal Reserve (US Fed) to take a hawkish approach.

In May 2022, the US Federal Reserve hiked rates by 50 bps and another 75bps in mid-June (the biggest hike since 1994). Further, it decided to raise the target range for the federal funds rate to 1.50% to 1.75% while announcing that further rate hikes look inevitable.

The RBI has also raised policy rates by a cumulative 90 bps in the last two months. And in the last monetary policy, it has decided to remain focused on the withdrawal of the accommodative stance.

Table 1: RBI Monetary Policy Actions

| Month | Repo Policy Rate | Policy Action (Basis points) | Policy Stance |

| Feb-19 | 6.25% | -25 | Neutral |

| Apr-19 | 6.00% | -25 | Neutral |

| Jun-19 | 5.75% | -25 | Accommodative |

| Aug-19 | 5.40% | -35 | Accommodative |

| Oct-19 | 5.15% | -25 | Accommodative |

| Dec-19 | 5.15% | Status quo | Accommodative |

| Feb-20 | 5.15% | Status quo | Accommodative |

| Mar-2020 (an exceptional off-cycle meeting) | 4.40% | -75 | Accommodative |

| May-2020 (an exceptional 2nd off-cycle meeting) | 4.00% | -40 | Accommodative |

| Aug-20 | 4.00% | Status quo | Accommodative |

| Oct-20 | 4.00% | Status quo | Accommodative |

| Dec-20 | 4.00% | Status quo | Accommodative |

| Feb-20 | 4.00% | Status quo | Accommodative |

| Apr-21 | 4.00% | Status quo | Accommodative |

| Jun-21 | 4.00% | Status quo | Accommodative |

| Aug-21 | 4.00% | Status quo | Accommodative |

| Oct-21 | 4.00% | Status quo | Accommodative |

| Dec-21 | 4.00% | Status quo | Accommodative |

| Feb-22 | 4.00% | Status quo | Accommodative |

| Apr-22 | 4.00% | Status quo | Accommodative |

| May-2022 (Off-cycle meeting) | 4.40% | 40 | Accommodative |

| Jun-22 | 4.90% | 50 | Turned focus on withdrawal of accommodative stance |

Data as of June 08, 2022

(Source: RBI Monetary Policy Statements)

While the cut in excise duty and VAT on fuel prices announced by the government will ease price pressures to an extent in the coming months, RBI expects inflation to remain elevated till the end of the current calendar year. Accordingly, economists expect RBI to continue to announce further hikes in the repo rate of about 50-60 bps in the current calendar year.

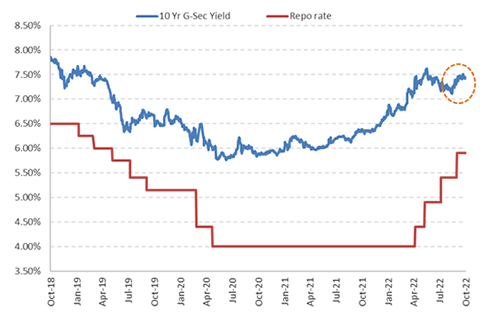

The impact of inflationary pressure is reflected in bond yields. India’s 10-year benchmark bond yield crossed 7.50% after RBI announced an interest rate hike in June, though it has softened a bit since then. The yields can rise higher as central banks announce further rate hikes.

Moreover, factors such as increased government borrowings, higher debt-to-GDP ratio, weak rupee, and overall economic uncertainty could push the benchmark bond yield further. So far this year it has climbed over 100 bps, the fastest pace since the year 2008.

Graph 2: The 10-year benchmark yield has hardened

Data as of June 27, 2022

(Source: Investing.com, PersonalFN Research)

With yields hardening, the interest rates on fixed income instruments also have moved up. In this situation, it is a good idea to revisit your asset allocation and optimise your exposure to debt funds.

Remember that debt funds are not risk-free. There are various risks associated with debt fund investment, such as interest rate risk, credit risk, and re-investment risk.

As you may know, interest rates and bond prices are inversely related. A surge in yield impacts bond prices negatively. As a result, the net asset value (NAV) of debt mutual funds, especially long duration funds, also declines.

When interest rates rise, funds focusing on longer duration instruments that have an average maturity typically in a range of 5 to 10 years are highly vulnerable to interest rate risk. These funds could witness high volatility in the near term. On the other hand, debt mutual funds that invest in short-term securities gain in a rising interest rate environment as they witness minimal mark-to-market impact.

Therefore, you will be better off deploying your hard-earned money in shorter duration debt mutual funds.

Given the current circumstances, it would be prudent to avoid selecting the ‘best debt mutual funds’ based on their past performance. The sub-categories and schemes that performed well in the past not necessarily will do well in the future. Instead, pay attention to your risk profile and time horizon when investing in debt funds.

If you are an investor with a low-risk appetite (conservative investors) and your time horizon is less than a year, opt for short term debt funds such as Liquid Funds.

On the other hand, if you are a moderate risk taker and have an investment horizon of 2 to 3 years, you may consider Banking & PSU Debt Funds with a maturity of up to 3 years. You can also consider adding safely managed Corporate Bond Funds that hold exposure to top-rated debt instruments, provided you do not mind taking slightly higher risk.

Also, as far as possible, invest in funds following an accrual strategy, i.e. holding the underlying debt instruments until maturity rather than engaging in yield hunting and taking a high risk.

To make your job simpler, we at PersonalFN have identified some of the best-performing schemes in the aforementioned sub-categories of debt mutual funds.

Table 2: Top 5 best debt mutual funds to invest in 2022

| Scheme Name | Category | Returns (Absolute (%) | Returns (CAGR %) | |

| 6 Months | 1 Year | 3 Years | ||

| Parag Parikh Liquid Fund | Liquid | 1.8 | 3.5 | 3.9 |

| Quantum Liquid Fund | Liquid | 1.8 | 3.5 | 3.8 |

| IDFC Banking & PSU Debt Fund | Banking and PSU Fund | 1.1 | 3.2 | 7.3 |

| Axis Banking & PSU Debt Fund | Banking and PSU Fund | 1.5 | 3.5 | 6.9 |

| Aditya Birla SL Corp Bond Fund | Corporate Bond | 0.7 | 2.9 | 7.1 |

| Crisil Liquid Fund Index | 2.0 | 3.8 | 4.5 | |

| Crisil Short Term Bond Fund Index | 0.3 | 2.8 | 6.6 | |

Data as of June 27, 2022

Direct Plan – Growth Option considered.

Past performance is not indicative of future returns.

(Source: ACE MF, PersonalFN Research)

These schemes have a proven track record of performance, respectable portfolio characteristics, and are from fund houses following robust systems and investment processes. More importantly, these schemes do not compromise on credit quality to generate higher returns.

For instance, Parag Parikh Liquid Fund held 91.9% of its portfolio in sovereign-rated instruments, 1.4% in CDs and CPs, and the balance in cash and equivalents, as of May 31, 2022. Quantum Liquid Fund also lays high emphasis on safety, investing predominantly in high-rated Government and Quasi-Government securities, and resists holding any exposure to instruments issued by private entities.

Similarly, IDFC Banking & PSU Debt Fund allocated 86.7% of its assets to the high-quality securities issued by PSUs, Banks, and PFIs, with another 9.7% in government securities, as of 31 May 2022. Likewise, Axis Banking & PSU Debt Fund portfolio is primarily exposed to top-rated bonds issued by Banks and PFIs, along with significant exposure to PSU bonds.

Even Aditya Birla SL Corp Bond Fund, a fund that predominantly invests in debt securities issued by private sector players, has been following a conservative approach. As of May 31, 2022, it held 63.2% of its assets in AAA-rated corporate debt instruments and 28.7% in government securities. It had 5% exposure of just 5% to securities rated below ‘AAA’ and no exposure to securities rated below ‘AA’.

Always remember, when you invest in debt funds, your primary aim should be preservation of capital; returns come secondary. To select the best debt mutual fund, it is important to assess the following parameters:

-

The credit quality of the underlying securities

-

The average maturity profile

-

The historical performance

-

The risk ratios

-

The investment processes & systems at the fund house

Lastly, remember that though debt mutual funds are relatively stable compared to equity mutual funds, the returns are not guaranteed. However, if you choose schemes carefully, they can offer you opportunities for effective diversification and asset allocation.

This article first appeared on PersonalFN here

{kind=link}