In an unscheduled but long-anticipated move, the RBI announced a hike in interest rates. On May 04, 2022, RBI’s Monetary Policy Committee (MPC) decided to raise the repo rate by 40 basis points (bps) to 4.40%, the first hike in nearly four years. Further, it has decided to increase the Cash Reserve Ratio (CRR) by 50 bps to 4.5% to reduce liquidity in the system.

Before we proceed to how these developments will have an impact on your debt mutual fund investments, first let us look at the reason behind RBI’s rate hike…

The RBI had reduced policy rates in the last couple of years to support economic growth amidst the COVID-19 pandemic. However, with inflation rising at an alarming pace in India and globally, the central bank shifted its focus from growth to curbing inflation in its April MPC meeting.

Notably, the CPI inflation had breached RBI’s upper tolerance limit of 6% for the third time in a row in March 2022. The inflation reading for March 2022came in at 6.95%, the highest in nearly one and a half years.

RBI is of the view that the rising inflationary pressure may not ebb any time soon. It will continue to remain at elevated levels in the coming months due to COVID-related restrictions as well as the ongoing Russia-Ukraine war.

Since elevated inflation levels can prove to be detrimental to economic growth and financial stability, the RBI decided to hike repo rate while maintaining the accommodative stance. Other major global central banks have already announced rate hikes and measures to reduce liquidity in the system due to surging inflation.

Economists expect RBI to continue to announce further hikes in the repo rate and gradually reach the pre-pandemic level of 5.15% by March 2023. This suggests that RBI could further hike the interest rate by 75 bps or more in the current financial year.

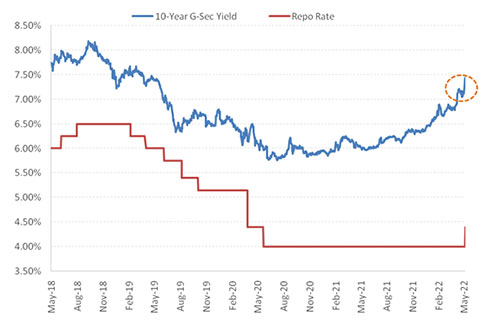

The 10-year bond yield, which had been steadily rising in the recent months, inched up to 7.4% after RBI’s announcement. As you may be aware, bond prices and yields are inversely related. A surge in yield impacts bond prices negatively, thus causing a loss to the investors’ value. As a result, the net asset value (NAV) of debt mutual funds, especially long duration funds, also declines.

Graph: The 10-year benchmark yield remained at an elevated level

Data as of May 06, 2022

(Source: Investing.com, PersonalFN Research)

What should be your debt mutual fund investment strategy now?

Considering the current rising interest rate scenario, debt mutual fund investors need to tread with caution.

When interest rates rise, debt mutual funds that invest in short-term securities gain. Funds that invest in the short maturity segment witness minimal mark to market impact when interest rates rise.

On the other hand, funds focusing on longer duration instruments that have an average maturity typically in a range of 5 to 10 years are highly vulnerable to interest rate risk. These funds could witness high volatility in the near term. Therefore, you will be better off deploying your hard-earned money in shorter duration debt mutual funds such as Liquid Fund.

[Read: 3 Best Liquid Mutual Funds to Invest in 2022]

Table: How have debt mutual funds performed?

| Average category returns | 1 month (%) | 1 year (%) |

| Banking and PSU Fund | -0.90 | 2.85 |

| Corporate Bond | -2.02 | 2.50 |

| Dynamic Bond | -1.08 | 2.93 |

| Gilt Fund with 10 year constant duration | -2.90 | -2.13 |

| Liquid | 0.26 | 3.45 |

| Medium to Long Duration | -1.46 | 1.98 |

| Ultra Short Duration | 0.04 | 4.09 |

Past performance is not an indicator for future returns

Data as on May 06, 2022. Direct plan – Growth option considered

(Source: ACE MF, PersonalFN Research)

In the last one year, short-term debt categories such as Liquid Fund and Ultra Short Duration Fund have generated better returns compared to long duration categories such as Gilt Fund with 10-year constant duration.

The lower residual maturity helps the fund to follow an accrual strategy where it can earn from coupon payments and roll over the assets on maturity. The accrual strategy also helps reduce the mark-to-market impact in a rising interest rate scenario.

If you have a long-term investment horizon, you can consider investing in a mix of safely managed Dynamic Bond Funds, Banking & PSU Debt Funds, and Corporate Bond Funds. However, it will be best to invest in these debt mutual funds in a staggered manner. You may consider setting aside some funds in a pure Liquid Fund and gradually scale up your investments in medium to long duration funds after every rate hike by RBI.

This way, you will be able to gradually build a long-term debt mutual fund portfolio as well as minimise the interest rate risk when the yields are trending upwards.

When you invest in debt mutual funds, remember that returns are not guaranteed. It is important to understand the various risk involved, viz. interest rate risk and credit risk, before selecting a debt mutual fund for your portfolio; avoid selecting schemes based on their recent performance.

Assess the following factors to pick the best schemes within each category:

- The credit quality of the underlying securities

- The average maturity profile

- The historical performance

- The risk ratios

- The investment processes & systems at the fund house

Ensure that you invest only in debt mutual fund schemes that align with your financial goals, risk profile, and investment horizon.

This article first appeared on PersonalFN here

{kind=link}