The recent sharp ups and downs witnessed in the Indian equity market have made investors jittery, especially those who have recently started their investment journey. The S&P BSE Sensex has declined by nearly 3,000 points (or about 4.8%) in the last one month, while the broader S&P BSE 500 index is down by around 5.5%, absolute. From its lifetime high of October 2021, the respective indices have dropped by about an absolute 6.4% and 7.4%.

The impact of the volatile market has been seen across Equity mutual fund categories. Among diversified equity schemes, Small-cap Funds were the worst hit while Large-cap Funds, Flexi-cap Funds, and Mid-cap Funds fared relatively better.

The higher volatility in the equity market is expected to continue over the course of the year due to various headwinds at play. Does it mean it is time to redeem your mutual funds or should you step-up your SIP contribution to gain from the lower costs?

To decide how to proceed with the SIP investment now, we need to first understand the reason for heightened volatility in the equity market…

1) Geopolitical tensions

Equity markets globally witnessed selloff amid the threat of war between Russia and Ukraine. Investors feared that possible economic and other sanctions against Russia by the US could disrupt exports of crude oil from one of the world’s top producers. Brent crude oil inched towards USD 100 per barrel, the highest level in more than seven years, raising concerns that it will dent corporate profitability and worsen the macroeconomic situation.

2) US Fed rate hike

US Inflation accelerated to a 40-year high of 7.5%. This could cause a spillover effect in the domestic market, as India is a net importer. Commodities like fuel, raw materials, and other goods could be affected by the increase in US inflation as these are imported. The high inflation reading also led to speculations that the US Federal Reserve could signal an immediate interest rate hike and halt its bond-buying programme, which could make emerging markets like India less attractive.

3) FII selling

Since the beginning of October 2021, FIIs have net sold to the tune of Rs 47,000 crore. This is due to a combination of factors such as high equity valuations, monetary policy measures by central banks like the US Federal Reserve, Bank of England, etc., strengthening of the dollar, and rising inflation. When interest rates rise, the profitability of corporate can shrink, and therefore, FIIs are pulling money out since valuations are high across various segments. It will take sustainable earnings growth and economic revival to regain their confidence in the Indian equity market.

Going ahead, fear of new Covid-19 variants and the resultant supply chain disruption, pace of economic growth, expensive equity market valuations, high inflation, liquidity tightening and normalisation of policy rates, earnings growth, etc. will keep the market volatile. Thus, 2022 is the year to be extra cautious about your mutual fund investments.

[Read: Mutual Fund Investment Strategy You Can Follow to Counter Equity Market Volatility]

That said, volatility is the very nature of the equity market; it is important to note that the market may not always be quick to bounce back after a correction. It is how we use market volatility to our advantage, perceive the situation sensibly, and devise an efficient strategy that decides our investment success.

The best way to sail through market volatility is to invest via SIP. If the market volatility continues or if the market corrects further from the present level, the inbuilt rupee-cost averaging feature of SIPs would take care of the intermittent volatility, more units will be added on during the corrective phase of the equity markets, and when it begins to ascend again, this strategy will compound your wealth.

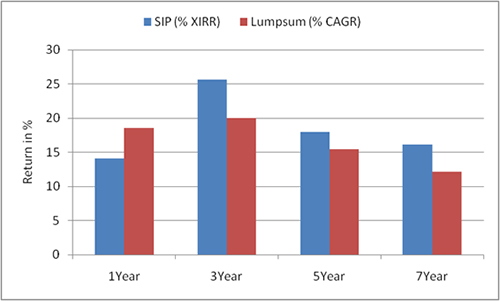

Graph: SIPs have worked better as opposed to a lump sum over longer time frames

Data as of February 17, 2022

Returns based on investment in Nifty 500 – TRI

(Source: ACE MF, PersonalFN Research)

Keep in mind, if the markets correct further and your SIP investment delivers disappointing returns, do not panic or be dismayed. As we can see in the graph above, SIPs can reward you over the long run. In fact, you can harness market volatility as an opportunity to step-up SIP and add more units at lower costs, which will aid in creating wealth over the long term.

Here are the benefits of stepping-up your SIP:

1) Facilitates building a bigger corpus

Volatile markets provide an opportunity to boost your investment to create wealth over the long term. By stepping up your SIP instalment, it adds to the power of compounding, and the potential return enables you to build a bigger corpus to accomplish your future financial goals. If you wish for a handsome amount in your hand at the end of 10, 15, or 20 years, increase your monthly SIP instalment year-after-year. Even a small increase now can make a big difference in the long term.

2) Counters inflation

Earning an effective real rate of return, or to put it simply, return adjusted for inflation, is an important factor to be considered while investing. Earning a higher real return helps you achieve your financial goals comfortably by countering inflation, which otherwise erodes the purchasing power of your hard-earned money. Since inflation increases every year, the amount that seems substantial today will not have the same value a few years down the line. By increasing your monthly contribution every year, step-up SIP leads to an overall increase in wealth, which in turn helps you to beat inflation.

3) Achieve the envisioned goals faster

By increasing your contribution every year, you would be able to achieve your goals faster than expected. For example, by increasing your SIP by 20% every year, you may be able to plan an early retirement. However, this will also depend on conditions like, by how much you decide to step up your SIP instalment, the type of schemes that you choose, and the amount you require to fulfil your goal.

4) Ensures focused planning

Instead of investing in new mutual fund schemes to take advantage of the market correction, you can consider stepping-up SIP in the schemes in your existing portfolio that may be doing well. This makes it easier to manage and monitor the progress of your portfolio which is necessary to maximize wealth.

The table below explains how different levels of a percentage hike in monthly SIP year-after-year will grow your wealth over 10 years, considering a starting monthly SIP instalment of Rs 5,000 in the first year and assuming an annual rate of return of 12%.

Table: How increasing SIP instalment every year enriches the power of compounding…

| % increase in SIP | Amount Invested (in Rs) | Corpus at the end of 10 year (in Rs) |

| 0 | 6,00,000 | 11,61,695 |

| 5 | 7,54,674 | 13,93,471 |

| 10 | 9,56,245 | 16,87,163 |

| 15 | 12,18,223 | 20,59,364 |

| 20 | 15,57,521 | 25,30,663 |

(Note: For illustration purpose only)

As we can see in the table above, if you hike the SIP contributions even by 5% or 10%, the amount at the end of tenure will be significantly higher. And if uncertainty strikes and you are undergoing financial stress, you have the option to pause SIP for a maximum period of three months. By using such options, you will not only continue to earn returns on your accumulated funds but also restart the SIP investments at a later date.

Now that you have learned the importance of stepping-up your SIP, it is important to note the following points to get the best out of your investment:

- Select schemes that align with your financial goals, risk profile, and investment objective

- Invest the right amount by quantifying your goals and assessing the time horizon before the goal befalls

- Invest regularly irrespective of the market conditions until your goal is achieved

[Read: How to Select Top Equity Mutual Funds for Your Portfolio]

Note that the equity market witnesses various events throughout the year. Most of these events do not have any long-term impact on the indices. Therefore, when the markets turn volatile do not make the mistake of discontinuing or redeeming your investments. Your SIP investment can always reward you with superior returns in the long run. The graph above is a proof of it.

It is important to have a long-term investment horizon of five to seven years or more, even if you are investing via a SIP. During certain periods SIP returns maybe a few percentage points lower compared to a lumpsum investment, but over a period it will still be sufficient to meet your financial goals.

That said, if you are nearing your goal horizon, gradually reduce exposure in equity mutual funds to invest in a more stable and less risky investment avenue, such as debt mutual funds and bank deposits.

This article first appeared on PersonalFN here

{kind=link}