The year 2021, has been eventful, yet an exciting year for the capital markets. A variety of factors coxswained the direction of the markets.

At the outset, it looked like 2021 would be a year of a strong global recovery as coronavirus infections receded. However, the second wave proved fatal for many countries, including India. Learning a lesson from this, the vaccination drive was fast-tracked by many nations. India as well, after the initial hiccups (vaccine shortage and uneven distribution) did exceptionally well in inoculating its people (administered over 138 crore doses so far).

Despite the pandemic, the Indian economy did reasonably well in the calendar year 2021: grew 1.6%, 20.1%, and 8.4% respectively in the March, June, and September quarters. This was owing to the favourable base effect of last year, pent-up demand, normal monsoon, pick-up in manufacturing, and overall improvement in economic activity after many of the restrictions and localised lockdowns were lifted in view of receding cases of COVID-19.

The Reserve Bank of India (RBI), kept its policy rates low and continued with its accommodative stance as long as necessary to revive and sustain growth on a durable basis plus to mitigate the impact of COVID-19 on the economy. This monetary policy action, despite the inflationary pressure persisting (due to higher commodity prices, mainly food and fuel, plus the core inflation that includes the non-food and non-fuel component), proved supportive. Disruption of global supply chains was also a cause for inflation.

Other than the above, the following were some of the important factors that had bearing on the financial markets in 2021:

- Rapid digitalisation amid the pandemic.

- Buzzing IPO market.

- A slew of New Fund Offers were being launched.

- The growing popularity of cryptocurrencies (due to crushes and crashes).

- A flare-up in the U.S. Treasury yields.

- Comfortable liquidity conditions (due to the helicopter money policy adopted by central banks in the developed world).

- A sudden change in the policy stance with the unwinding of stimulus by the U.S. Federal Reserve (Fed), and then the European Central Bank (ECB) too indicating the same towards the end of the year.

- Cooling economic activity in China on account of real estate debacles and government crackdowns on tech companies.

- And the very recent one, the resurgence in coronavirus infections around the world due to the virulent ‘Omicron’ variant.

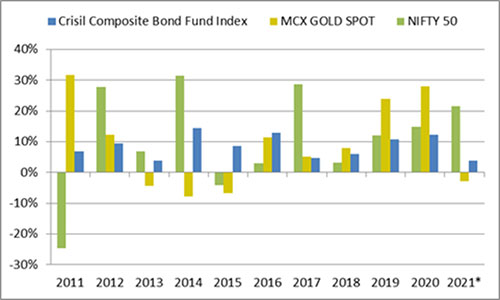

Graph: Year-on-Year performance of Equity, Debt, and Gold

Data as of December 17, 2021

(Source: ACE MF, PersonalFN Research)

Among the asset classes, equities did remarkably well – in fact, better than the previous calendar year. The smaller companies, in particular, i.e. the mid-caps and small-caps did exceptionally well in 2021, compared to their large-cap counterparts, despite the recent sharp correction witnessed towards the end of the year.

This was because, investors remained upbeat on the high-beta and high growth smaller companies that were beaten down, and which they perceived would do well in the long-term as we walk out of the COVID-19 pandemic.

Information and Technology (IT), healthcare, metals, energy, realty, and financials, were among the top-performing sectors of 2021. Auto & auto ancillaries, hospitality, media & entertainment, ship-building, and paper were among the worst-performing sectors that disappointed investors.

How did equity mutual funds fare?

Small-cap Funds, Mid-cap Funds, and Multi-cap Funds outperformed the other diversified equity sub- categories. Since the risk-on trades dominated throughout the year, the Large-cap Funds underperformed.

Table 1: Small-cap Funds Generated Big Returns in 2021

| Category | YTD Return (%) |

| Small cap Fund | 60.6 |

| Mid Cap Fund | 43.1 |

| Multi Cap Fund | 41.0 |

| Dividend Yield | 36.4 |

| Large & Mid Cap Fund | 36.0 |

| Contra Fund | 35.0 |

| Value Fund | 34.2 |

| Flexi Cap Fund | 30.2 |

| Focused Fund | 30.0 |

| Large Cap Fund | 24.7 |

| NIFTY 50 – TRI | 22.9 |

| NIFTY 500 – TRI | 28.7 |

Category average returns considered (Absolute)

Data as of December 17, 2021

(Source: ACE MF, PersonalFN Research)

That being said, the performance of equity mutual fund schemes wasn’t uniform and some of the popular Small-cap Funds seemed to lag. For instance, Quant Small Cap Fund, Principal Small Cap Fund generated 86.0% and 72.3% returns respectively. Whereas, the ones such as DSP Small Cap Fund, IDFC Emerging Businesses Fund, and SBI Small Cap Fund generated 55.6%, 48.8%, and 46.4% Year-To-Date (YTD) returns, respectively as of December 17, 2021.

Similarly, even in the Large-cap Fund category, the outperforming funds on a YTD basis were not top-rated ones. Amongst them, Nippon India Large Cap Fund and Invesco India Large Cap Fund stood out with their 31.3% and 31.6% returns respectively. Whereas, some of the most popular Large-cap schemes have underperformed miserably. For instance, the Axis Bluechip Fund generated 19.6% returns on a YTD basis (as of December 17, 2021).

Unlike the yesteryears, the stock market rally was broad-based in 2021, and thus the top-down investing as well as the bottom approach seems to have done well. Those taking concentrated positions in a few quality names or in frontline stocks or those with overweight positions in certain financial and FMCG stocks, which did not move very well underperformed irrespective of their subcategory.

How did debt mutual funds fare?

Speaking of debt mutual funds, as the RBI continued its accommodative policy stance to support growth and kept policy rates unchanged; debt funds looked unattractive this year. Barring a few exceptions, a majority of debt fund sub-categories clocked returns comparable to overnight rates or the repo rate.

Table 2: Unexciting Year for Debt Mutual Funds

| Category | YTD Return (%) |

| Medium Duration Fund | 12.7 |

| Low Duration Fund | 10.5 |

| Corporate Bond Fund | 9.5 |

| Credit Risk Fund | 6.7 |

| Short Duration Fund | 5.2 |

| Ultra Short Duration Fund | 4.1 |

| Banking and PSU Fund | 3.9 |

| Dynamic Bond Fund | 3.7 |

| Money Market Fund | 3.6 |

| Short & Mid Term Fund | 3.2 |

| Overnight Fund | 3.1 |

| Liquid Fund | 2.9 |

| Gilt Fund with 10-year constant duration | 2.4 |

| Medium to Long Duration | 2.3 |

| Long Duration | 1.9 |

| Crisil Composite Bond Fund Index | 3.8 |

| Crisil 10 Yr Gilt Index | 1.5 |

| Crisil 1 Yr T-Bill Index | 3.4 |

Category average returns considered (Absolute)

Data as of December 17, 2021

(Source: ACE MF, PersonalFN Research)

Among the Low Duration Funds, if you leave aside the gains on the segregated portfolio of Tata Treasury Advantage Fund and that of a troubled scheme, Franklin India Low Duration Fund; the returns generated by a majority of other Low Duration Funds have been in low single-digits. The median returns generated by Low Duration Funds is just 3.9% (as of December 17, 2021)

Similar is the case with Medium Duration Funds. So, do not just plainly look at the category average returns. Delving deeper reveals that the median returns of Medium Duration Funds are just 5.7% (as of December 17, 2021).

In the case of Corporate Bond Funds too, the median return has been just 4.0%. Only Nippon India Corporate Bond Fund has clocked an absolute return of 5.10%.

The Credit Risk Funds which made a comeback in 2021 are not different either. Their outperformance seems to be largely on account of recovery in segregated portfolios and favourable upgrades to downgrades ratio. During the April-September 2021 period, Crisil upgraded 488 companies. The downgrades were restricted only to 165 entities. UTI Credit Risk Fund, Baroda Credit Risk Fund, and Franklin India Credit Risk Fund generated 22.1%, 19.9%, and 14.0% YTD returns respectively, (as of December 17, 2021) reflecting a good recovery in their troubled portfolios.

How has Gold performed in 2021?

Amidst a period of risk-on and the crush for cryptocurrencies, the previous yellow metal — gold — lost some sheen. On a YTD basis, gold clocked -2.8% absolute returns as per the MCX data (as of December 17, 2021). The reasons for this were ample liquidity, resilient greenback, encouraging GDP growth rate numbers reported by most countries in the last few quarters, receding cases of COVID-19, and a better inoculation rate.

But then, recognising the possible uncertainty to global growth from the virulent Omicron variant (classified as the “variant of concern” and high-risk by the World Health Organisation, since it is 6 times more transmissible than the Delta variant), certain smart investors did look up to gold as a safe haven, a store of value, a hedge, and/or a portfolio diversifier.

What to expect in 2022 and the investment strategy to follow:

Mainly backed by gush liquidity, the Indian equity markets scaled a lifetime high quickly than anticipated and much ahead of the fundamentals. But now against the backdrop of the virulent Omicron variant, volatility is expected to intensify; you may witness a rollercoaster ride.

The threats from the new variant, Omicron, aren’t still known completely. However, as things stand today, the new variant is said to be causing milder symptoms and fewer hospitalisations. That said, it does not mean the world can afford to throw caution out of the window. Those who have already taken their vaccines are also contracting the Omicron variant, going by the media reports. The current COVID-19 vaccines do not seem to work very effectively against the Omicron variant.

“If we look at the scale of spread in the UK and if there is a similar outbreak in India, then given our population, there will be 14 lakh cases every day,” said Dr. VK Paul, the COVID-19 task force chief and member of the Niti Aayog. After the holiday season and the state assembly plus municipal elections conclude, the third wave of Omicron replacing the delta variant cannot be ruled out. The magnitude of the third wave cannot be determined at present; it all depends on the ability of the virus to escape the natural immunity and shield offered by the vaccine.

To curb the spread of infections, if the government reinstates restrictions and localised lockdowns, it could weigh down on economic activity and GDP growth. The RBI, the World Bank, International Monetary Fund (IMF), and noted economists too have cited that the future pandemic trends still hold the key to global recovery. According to IMF, the global GDP projection for 2021 has been 5.9%, and that for 2022 stands at 4.9% as per its World Economic Outlook, October 2021.

The uncertainties related to the economic recovery and inflationary pressure might keep the global markets under pressure in the forthcoming year. The corporate earnings, which have shown an encouraging trend in the last few quarters, may also be impacted for certain companies within the respective sectors.

Do not get swayed by the unrealistic corporate earnings estimates. Do not get caught in the earnings trap (where often the near-term estimates are being toned down while the future earnings estimates are unreasonably increased). It would be incorrect to live under the impression that earnings would improve in a linear manner quarter-on-quarter. You see, the sustainability of earnings growth remains to be closely watched in light of the potential impact of the Omicron variant on the economy and the operating costs.

Be wise and take note of the famous quote: “Be fearful when others are greedy and greedy when others are fearful”, by the legendary investor, Mr Warren Buffett.

The valuations in the Indian equity markets have turned relatively expensive after a swift recovery from March 2020 low. Even though the markets have corrected around 10% since the lifetime high, valuations still look frothy; they aren’t cheap in any way. The margin of safety appears to be narrow and does not seem very comfortable enough compared to the last year. Therefore, it is advisable to approach the Indian equities sensibly.

What you require to do is follow a time-tested strategy, known as the Core & Satellite Investment Strategy, pursued by some of the most successful equity investors across the world to build an equity portfolio.

The term ‘Core’ applies to the more stable, long-term holdings of the portfolio, while the term ‘Satellite’ applies to the strategic portion that would help push up the overall returns of the portfolio, across market conditions.

By wisely structuring and timely reviewing the Core and Satellite portions and the holdings therein, you would be able to add stability to the portfolio while strategically boosting your portfolio returns at the same time.

The ‘Core’ holding should comprise around 65-70% of your equity mutual fund portfolio and consist of a Large-cap Fund, Flexi-cap Fund, and Value Fund/Contra Fund. Whereas the ‘Satellite’ holdings of the portfolio can be around 30-35% comprising of a Mid-cap Fund and an Aggressive Hybrid Fund.

To add equity mutual fund schemes to your investment portfolio based on the Core & Satellite strategy, here are a few fundamental rules to follow:

- Consider funds that have a strong track record of at least 5 years and have been amongst the top performers in their respective categories.

- The schemes should be diversified across investment styles and fund management.

- Ensure that each selected scheme abides with its stated objectives, indicated asset allocation, and investment style.

- You should not only invest across investment styles (such as growth and value) but also across fund houses.

- The mutual fund schemes should be managed by experienced and competent fund managers and belong to fund houses that have well-defined investment systems and processes in place.

- Not more than five schemes managed by the same fund manager should be included in the portfolio.

- Not more than two schemes from the same fund house shall be included in the portfolio.

- Each scheme that is to be included in the portfolio should have seen an outperformance over at least three market cycles.

- You should restrict the count of total mutual fund schemes in your portfolio to seven.

Given the looming uncertainty, I suggest opting for the Systematic Investment Plan (SIP) route while you build the portfolio of equity-oriented mutual fund schemes following the ‘Core and Satellite’ approach.

If you correctly follow the ‘Core & Satellite’ approach while investing in equity mutual funds, here are the six key benefits it will adduce:

- Facilitate optimal diversification among equity mutual fund schemes.

- Reduce the need to frequently churn your entire portfolio.

- Reduce the risk to your portfolio.

- Enable you to benefit from a variety of investment styles and strategies.

- Create wealth cushioning the downside.

- Help you potentially outperform the market.

Note, the Core & Satellite investment strategy may work for you in 2022 and beyond.

As regards investing in debt mutual funds is concerned, first note that investing in debt funds, in general, is not risk-free.

The RBI currently has decided to wait for growth signals to be solidly entrenched while remaining watchful of the inflation dynamics. So, it appears that policy normalisation in India would not begin anytime soon. Having said that, it appears that the present interest rate cycle has bottomed out. A few central banks such as the Bank of England (BOE), Brazil, Mexico, and Russia have already begun to raise policy rates.

At the current juncture, as an investment strategy, it would be wise to approach the shorter end of the maturity yield curve. You’ll be better off deploying your hard-earned money in shorter duration debt mutual funds. But approach even short-term debt funds with your eyes wide open by paying attention to the portfolio characteristics and quality of the scheme. Stay away from debt mutual fund schemes that have exposure to low-rated securities in the hunt for yield amidst a time when the credit risk has intensified. Stick to debt mutual funds where the fund manager does not chase yields by taking higher credit risk but instead focuses on government and quasi-government securities. If you have an investment horizon of around 2-3 years and are a moderate risk-taker, consider investing in the best Banking & PSU Debt Funds.

For a period of up to or less than a year, you may consider investing in the best Liquid Funds. And if you have a very short-term time horizon (a week to a couple of months), you may invest in overnight funds.

Alternatively, if you prefer to keep your capital safe, opt for bank fixed deposits, but choose the bank carefully.

As far as the gold as an asset class is concerned, approach it as an effective portfolio diversifier, a hedge, and a haven against the backdrop of an uncertain investment environment. The uncertainty brought by the virulent Omicron variant, risk to the inflation trajectory, intensified stock market volatility, high debt-to-GDP around the world, and geopolitical risks, make a case for investing in gold. However, if the U.S. Federal Reserve and the ECB, increase interest rates going forward, that may limit the returns from gold.

Nevertheless, it makes sense to tactically allocate to gold and hold it as a portfolio diversifier. Allocating around 10-15% of your entire investment portfolio to gold and holding it with a long-term investment horizon (of over 5 years), by assuming moderately high risk, will be a smart and sensible thing to do. Instead of buying physical gold, consider investing in gold ‘the smart way’ through gold Exchange Traded Funds (ETFs) or gold savings funds or Sovereign Gold Schemes.

Furthermore, given that the pandemic is not over yet, hold optimal cash in the bank and/or a Liquid Fund or an Overnight Fund for your emergency needs.

Happy Investing!

This article first appeared on PersonalFN here

{kind=link}