SEBI had recently prescribed a dual benchmarking structure for mutual funds to bring uniformity in benchmark of schemes within a particular category.

As per SEBI’s circular, the first-tier benchmark will reflect the category of the scheme viz. Large-cap, Mid-cap, Multi-cap, etc., while the second-tier benchmark will demonstrate the investment style/strategy of the fund manager within the category for instance, growth, value, or any other particular strategy within the broader category, etc. In the same circular, SEBI had asked the Association of Mutual Funds in India (AMFI) to release the list of benchmarks for each category.

Subsequently, AMFI has now notified the indices to be followed by the Asset Management Companies (AMCs) as Tier 1 benchmark. The second-tier benchmark is optional and can be decided by the AMC depending on the investment strategy/style of a particular scheme. All the benchmarks should necessarily be Total Return Indices (TRI) .

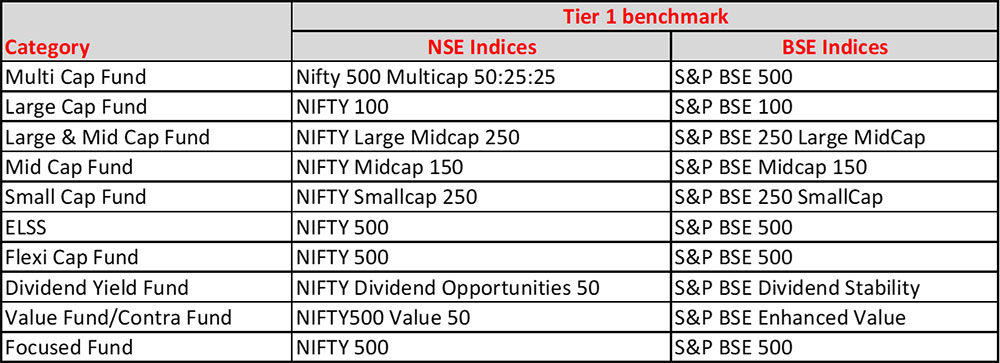

For equity funds, AMCs can choose from the NSE or S&P BSE indices, while for debt fund category the schemes can choose benchmark from the NSE, S&P BSE, or CRISIL indices. The Tier 1 benchmark for various equity mutual fund categories are as given below:

Table 1: List of benchmarks specified by AMFI for Equity Mutual Funds

(Source: AMFI)

Simply put, every Large-cap Mutual Fund scheme will have the broader large-cap market index such as Nifty 100 – TRI or S&P BSE 100 – TRI as their first-tier benchmark. The Large-cap scheme can decide the second-tier benchmark which they feel best represents their investment style/strategy. So, if a Large-cap fund invests only in top 50 large-cap stocks, it could have Nifty 50 – TRI as its second-tier benchmark or S&P BSE Sensex – TRI if it invests in the top 30 large-cap stocks.

Similarly, a Flexi Cap Fund can have Nifty 500 – TRI or S&P BSE 500 – TRI as Tier 1 index. Meanwhile, a Flexi Cap Fund investing predominantly in large-cap and mid-cap stocks may choose the Nifty 200 index or Nifty Large Midcap 250 index as second-tier benchmark to better reflect the risk-return profile of the scheme.

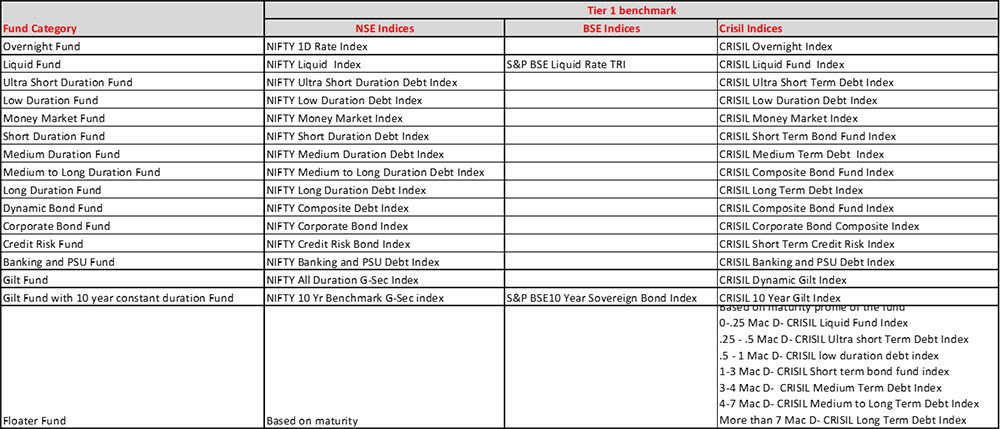

Likewise, for debt mutual fund category, all the funds in the Ultra Short Duration category will have Nifty Ultra Short Duration Debt Index or CRISIL Ultra Short Term Debt Index as first-tier benchmark. And if an Ultra Short duration scheme invests predominantly in AAA-rated securities it could have Nifty AAA Corporate Bond Index as the second-tier benchmark to indicate its investment strategy.

Table 2: List of benchmarks specified by AMFI for Debt Mutual Funds

(Source: AMFI)

For hybrid and solution-oriented schemes, there will be a single benchmark. It will be a broad market benchmark wherever available, or a customised benchmark will be created for schemes, which will then be applied across industry.

Table 3: List of benchmarks specified by AMFI for Hybrid Mutual Funds

(Source: AMFI)

Thematic/Sectoral schemes too will have a single benchmark because the characteristics of these schemes are already tapered according to the theme/sector. Similarly, Index Funds and ETFs will also have a single benchmark as these schemes replicate an underlying index.

For Fund of Fund schemes investing in a single fund, the benchmark of the underlying scheme will be used. However, in case of Fund of Fund scheme investing in multiple schemes, the broad market index will be applied.

The afore-mentioned framework will come into effect from January 01, 2022.

How will investors benefit from the new benchmarking norms for mutual fund schemes?

As you know, selecting the right scheme plays a key role in making your investment successful. SEBI’s new rule is a positive move that can make this crucial step easier for investors.

Since funds within a category invest in companies from the same universe of stocks, a common benchmark for all schemes makes sense even though the investment strategy/style may differ from scheme to scheme.

Consider this, there are various schemes in the Small-cap fund category. Some schemes are benchmarked against the Nifty Smallcap 250 – TRI index while others have Nifty Smallcap 100 – TRI as their benchmark. These indices have generated an absolute return of 64.5% and 61.3%, respectively, in the last one year.

Now, let us assume that two schemes Fund A and Fund B are benchmarked against the Nifty Smallcap 250 – TRI index and Nifty Smallcap 100 – TRI, respectively. Both the schemes have generated returns of 68% each during the same period. But since Fund A is benchmarked against Nifty Smallcap 250 – TRI index it has an outperformance of 3.5 percentage points over its benchmark, while Fund B has generated an alpha of around 6.5 percentage points.

Thus, the outperformance of a particular scheme can differ significantly based on the performance of the index it is benchmarked against, making it look better or worse compared to its peers. Therefore, it may not be fair to compare two or more schemes based on the difference in returns that they have generated over their respective benchmarks. The common Tier 1 benchmark aims to address the anomaly of uneven performance comparison.

A common first-tier benchmark can give investors a realistic picture of the performance of schemes within a particular category. Additionally, it will facilitate comparison of alpha generated by the schemes over a period. On the other hand, the optional second-tier benchmark will give an idea about the investment strategy/style as well as the asset allocation that the scheme will follow. It can also be used to make deeper analysis of the scheme’s performance relative to another scheme following similar strategy/style.

Therefore, SEBI’s move can potentially make it easier for retail investors to compare and select suitable schemes within a category.

This article first appeared on PersonalFN here

{kind=link}