We are less than 6 months away from the end of financial year 2021-22. This means it is high time that you start focusing on your tax saving plans if you haven’t done so already. Depending upon your financial goals, risk appetite and investment time horizon, you can invest in various tax saving instruments such as Public Provident Fund (PPF), National Saving Certificate (NSC), Tax Saver Bank FD, Equity-linked Saving Scheme (ELSS), etc.

Among the various tax saving options available, tax saving mutual fund or ELSS is an efficient tax saving investment avenue that stands out from the rest. ELSS offers investors the dual advantage of tax saving benefit as well as the long term growth potential of equities. This is why ELSS has gained immense popularity among tax payers in the last decade. However, the category has lost some shine in the last one year.

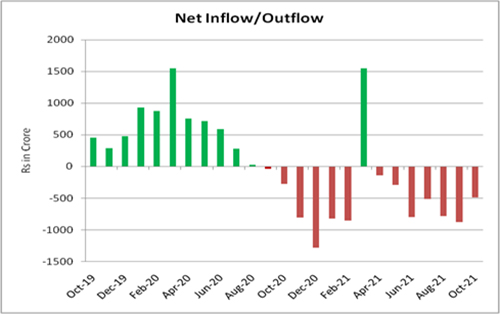

Barring the month of March 2021 (the last month to invest in tax saving instruments for a financial year) the category has witnessed constant outflows in every month since September 2020. So far in the current calendar year, the category has witnessed net outflows of Rs 3,985 crore. The trend is in contrast to previous years when the category grew in popularity and witnessed steady inflows in most of the months.

Graph: Investors shy away from ELSS

Data as of October 31, 2021

(Source: AMFI)

What are the reasons for net outflows in the ELSS category?

- The Indian equity market scaled record highs during the year. Since ELSS come with a mandatory lock-in period of 3 years, investors are probably wary of locking in their funds at market peak due to the likely correction in the near future.

- Some ELSS investors who have completed the lock-in period took the advantage of swift recovery in equity markets and booking profits at all-time highs, thus leading to outflows in the category.

- The new income tax regime allows tax payers to avail of the benefit of lower income tax rate. However, if they opt for the new low tax regime they have to forego certain deductions and exemptions available on some investments and expenses. Accordingly, individuals who have opted for the new tax regime no longer need tax saving investments such as ELSS.

- Underperformance of certain ELSS compared to the benchmark in the last couple of years could also be a reason for outflows in the category.

- As uncertainties regarding the pandemic still prevails, causing volatility in the equity market, conservative investors are compelled to look at safer avenues such as PPF and Tax Saver Bank FD for their tax saving needs despite lower returns.

Should you invest in ELSS for your tax saving needs?

ELSS offers you the dual advantage of tax saving benefit and the growth potential of equities, a feature that most other tax saving options do not boast of. Moreover, the lock-in period of ELSS is the shortest compared to other tax saving instruments such as PPF, NSC, Tax Saver Bank FD, etc. The lock-in period allows you to maintain a disciplined approach and stay invested for a long term, which is essential to gain the maximum benefit of the growth potential of equities.

Table: ELSS have successfully created wealth for investors over the long term

| Scheme Name | Absolute (%) | CAGR (%) | |||

| 1 Year | 2 Years | 3 Years | 5 Years | 7 Years | |

| Quant Tax Plan | 83.01 | 54.41 | 36.98 | 27.08 | 23.64 |

| BOI AXA Tax Advantage Fund | 47.92 | 36.28 | 28.90 | 22.81 | 16.94 |

| Mirae Asset Tax Saver Fund | 43.35 | 29.30 | 25.22 | 23.24 | — |

| Canara Rob Equity Tax Saver Fund | 44.34 | 31.28 | 25.16 | 21.23 | 15.01 |

| DSP Tax Saver Fund | 44.28 | 25.30 | 22.70 | 17.98 | 15.56 |

| Union Long Term Equity Fund | 44.17 | 27.95 | 22.60 | 17.09 | 11.51 |

| UTI LT Equity Fund (Tax Saving) | 42.77 | 27.97 | 22.56 | 17.80 | 13.59 |

| JM Tax Gain Fund | 40.97 | 25.84 | 22.54 | 19.97 | 15.26 |

| Kotak Tax Saver Fund | 41.98 | 25.47 | 22.25 | 18.24 | 15.00 |

| Axis Long Term Equity Fund | 34.72 | 24.21 | 22.21 | 20.05 | 15.86 |

| Category average | 40.37 | 24.08 | 19.46 | 16.95 | 13.40 |

| NIFTY 50 – TRI | 32.64 | 20.23 | 18.39 | 17.40 | 11.84 |

| NIFTY 200 – TRI | 36.63 | 22.26 | 18.61 | 17.26 | 12.50 |

| NIFTY 500 – TRI | 39.23 | 23.98 | 19.33 | 17.48 | 12.87 |

Data as on November 26, 2021

(Source; ACE MF)

As you can see in the table above, long term performance record of many ELSS is healthy which makes it a worthy avenue for tax planning. Now, while past performance is not indicative for future returns, it displays the high return potential of investing in ELSS and equity as an asset class, in general.

Considering that the long term growth prospects of the Indian equity market looks positive, ELSS can be a suitable choice for your tax saving needs as well as to earn inflation-beating returns in the long run. However, ensure that you set a realistic return expectation from your ELSS investment.

If you are a conservative investor you can consider large-cap oriented ELSS instead of funds that follow a multi-cap approach. Investors with moderate to high risk profile can consider investing in multiple ELSS schemes (but not more than 2-3 schemes) having different investment strategy/style to get the benefit of adequate diversification. But do note that Section 80C of the Income Tax Act allows maximum deduction of up to Rs 1.5 lakh in a financial year.

Notably, the equity market has witnessed some consolidation in the last few weeks due to which most key indices are down by over 7% from its peak. This correction offers an opportunity for long term aggressive investors to invest in ELSS for tax saving purpose.

But remember that ELSS carry a lock-in period of three years. Thus, if you decide on a not-so-worthy fund, you will have to bear the cost of underperformance for the entire period. Therefore, it is important that you choose ELSS for your portfolio carefully. On the other hand, if your ELSS is performing well, you can consider holding it beyond the lock-in period to benefit from the higher returns and let your wealth grow leaps and bounds.

Why you should not wait till March to invest in ELSS?

Often investors wait till March i.e. the end of the financial year to make investments for their tax saving needs. But in my view, tax saving is an important financial goal that needs prudent planning. If you delay investing in ELSS till the last minute you may end up investing in a not-so-worthy and/or unsuitable ELSS scheme.

On the other hand, if you start investing well before the deadline you will have ample time to evaluate the schemes on various quantitative and qualitative parameters and choose the one with the most consistent track record. Moreover, starting early will save you from the burden of last minute cash outflow and you will be able to invest smaller amount gradually via SIP route.

Investing well in time also allows you to avoid/overcome any transactional/technical glitches. Besides, if you are a first time investor, the KYC process, bank mandate, cheque clearance, as well as the allocation of mutual fund units to your account may take time, and you may end up potentially missing the March 31 deadline.

Thus, it is important that you avoid investing in an adhoc manner and plan your tax saving exercise prudently to avoid regretting your decision later.

This article first appeared on PersonalFN here

{kind=link}