Sundaram Asset Management Company Ltd. has received SEBI’s approval for the acquisition of Principal Asset Management Pvt. Ltd. Sundaram Asset Management Company had first announced the purchase of the asset management business of Principal in January 2021, and had received the approval of Competition Commission of India in April 2021.

As per the terms of agreement, Sundaram Asset Management Company (Sundaram AMC) will acquire the schemes managed by Principal Asset Management Pvt. Ltd (Principal AMC) and acquire 100% of the share capital of Principal Asset Management Pvt. Ltd., Principal Trustee Company Pvt. Limited, and Principal Retirement Advisors Pvt. Ltd.

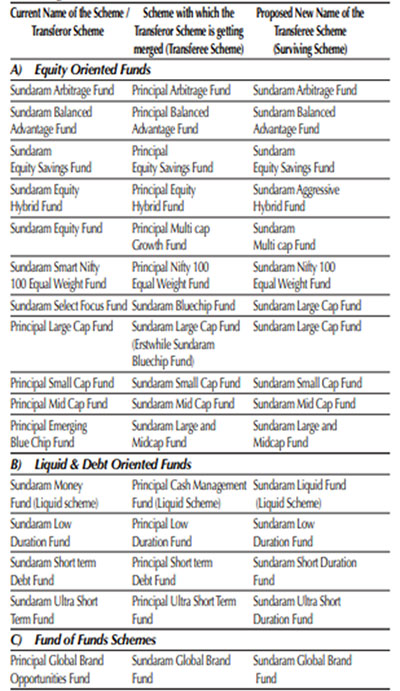

Accordingly, the schemes of Principal Mutual Fund will be transferred to and form part of Sundaram Mutual Fund. In order to avoid existence of similar schemes and to comply with the SEBI circular on scheme categorization, certain schemes of Sundaram Mutual Fund will be merged with the corresponding schemes of Principal Mutual Fund while a few schemes of Principal Mutual Fund will be merged with the corresponding schemes of Sundaram Mutual Fund (see Table 1 below).

Table 1: List of schemes that will be merged

(Source: Addenda – Sundaram Mutual Fund)

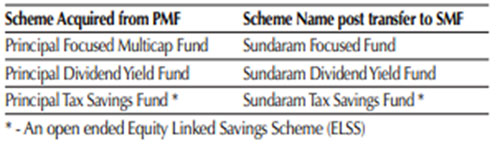

Meanwhile, the following schemes of Principal Mutual Fund will be taken over by Sundaram Mutual Fund and there will be no change in characteristic or features of the scheme except the name.

Table 2: Schemes that will be carried over by Sundaram Mutual Fund

(Source: Addenda – Sundaram Mutual Fund)

Why is Principal Mutual Fund exiting the asset management business?

In a press release, Mr Pedro Borda, Chief Operating Officer (COO), Principal International said, “As part of a systematic review of the company’s portfolio of businesses and global market dynamics, we’ve made the decision to exit the asset management business in India. As we transition the business, customers and distributors will remain our top priority. We believe they will benefit from Sundaram Asset Management’s larger mutual fund platform in this market.”

This will mark the exit of another foreign entity from mutual fund business in India. In the past few years, foreign entities like Morgan Stanley, ING, PineBridge, Deutsche, Goldman Sachs, JP Morgan, and Black Rock have sold their stake in the Indian asset management industry.

The acquisition will help Sundaram Asset Management Company to become a sizeable player in the Indian mutual fund industry. As on October 31, 2021, Sundaram Mutual Fund had Rs 33,577 crore in assets under management (AUM), whereas Principal Mutual Fund had an AUM of Rs 9,558 crore during the same period.

Commenting on the acquisition, Mr Sunil Subramaniam, Managing Director, Sundaram Asset Management Company said, “This transaction will strengthen our presence in the marketplace with the addition of a range of schemes with a good long term performance track record across the large and mid-cap segments. This will complement our business which has traditionally been weighted towards the mid- and small-cap segment.”

What should investors in Principal Mutual Fund do?

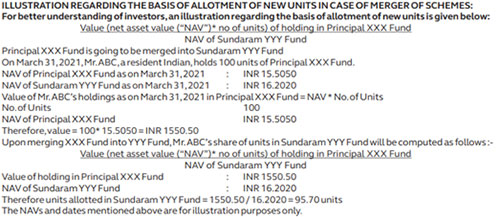

Unit holders of the Transferor Schemes will be allotted new units under the Transferee Schemes/Surviving Schemes and a fresh account statement reflecting the new units allotted will be sent to the unit holders.

Illustration: Allotment of units in case of merger of schemes

(Source: Press release – Principal Mutual Fund)

According to SEBI’s circular, merger of Transferor Scheme(s) with Transferee Scheme(s) is treated as a change in fundamental attributes of the Transferor Scheme(s). However, merger or consolidation is not seen as a change in fundamental attribute of the surviving scheme if there is no change in the fundamental attributes of the transferee scheme and if it does not change the features/ provision (in any manner) which would adversely affect the interest of the unit holders of the surviving scheme(s).

Consequently, unit holders in such schemes of Principal Mutual Fund that will undergo change in fundamental attributes have the option to redeem their investment in the scheme without any exit load at the prevailing NAV, within the notice period of 30 days.

Though there is an option to exit without any load, the proceeds from redemption are subject to capital gains tax depending on the holding period and type of scheme (equity, debt).

It is important to note that exiting is just an option and not a compulsion. If the Principal mutual fund scheme that you have invested in is performing well compared to its category peers and the benchmark index, and if there is no significant difference in the investment strategy/style or portfolio characterisitcs, then it makes sense to continue holding it.

That said, since most schemes of Sundaram Mutual Fund across equity and debt categories have not fared well on risk-reward parameters in the last couple of years, you need to keep a close watch on its performance post the merger.

However, if the merged scheme follows a more aggressive/conservative investment approach than the current scheme and is no longer in congruence with your risk profile, or if the investment objective of the merged scheme does not align with your own investment objective, you can consider exiting the scheme during the free exit load period.

Certain schemes of Sundaram Mutual Fund will also undergo significant changes in its fundamental attributes. For instance, Sundaram Select Focus, a Focused Fund will now be merged with Sundaram Bluechip Fund and will become a Large-cap fund.

But do not conclude that the merger of schemes will improve or deteriorate its performance. Instead, pay attention to the changes and practices put in place by Sundaram AMC post acquisition of Principal AMC and how prudently they manage your money.

To conclude

It is important to understand the investment philosophy of the fund house and investment processes they follow. Only process-driven fund houses can give you consistent performers over the long term.

Further, before taking any investment decisions evaluate your investment objective, risk appetite, and investment horizon to select the most suitable scheme that scores well on quantitative as well as qualitative parameters.

This article first appeared on PersonalFN here

{kind=link}