Over the past few years Credit Risk Funds have been making headlines for all the wrong reasons. It started with one of India’s leading infrastructure and Finance companies, IL&FS, defaulting on paying interest to its bond holders in September 2018. In the next 2-3 months, rating agencies downgraded the AAA rated debt instruments of IL&FS to D. Many such events of defaults and/or downgrades regularly came to light throughout the year 2019. This included debt papers of well known entities such as, DHFL, Reliance ADAG, Yes Bank, Essel group, among others.

[Read: Why Investing In Debt Mutual Funds Turning Riskier]

Since debt mutual funds held allocation to the debt papers issued by these entities, they were forced to mark down the value of the securities. According to a data compiled by CRISIL, the impact of defaults on debt mutual funds was Rs 17,719 crore between July 2018 and February 2020.

The defaults impacted almost every debt mutual fund category including safe avenues like Liquid Funds. Credit Risk Funds were the worst affected since they invest predominantly in below highest rated instruments (below AAA rated instruments).

The onset of the COVID-19 pandemic in early 2020 triggered illiquidity in the debt market and further escalated the turmoil in the debt mutual fund segment, especially those schemes that held low-rated securities. The Franklin Templeton Mutual Fund fiasco is a harsh reminder of the trouble that brewed in the debt segment. As you may be aware, the AMC had wound up six of its debt schemes (including credit risk fund) citing the overall stress in the credit market and tight liquidity in the debt.

Another fund in the credit risk category, BOI AXA Credit Risk Fund, lost around 50% of its value during the same period as the fund house marked down its various debt securities.

Since then investors have turned wary of the credit risk category. Consequently, the category has witnessed massive outflows between May 2020 and April 2021.

Experts expected that the COVID-19-induced lockdown would likely dent the profitability of corporates and weaken the economic growth. As a result, this would impact the ability of corporates to service debt leading to rising instances of defaults and downgrades, particularly in credit risk funds.

However, the liquidity in the debt market has improved significantly in the past one year. On the back of this several credit risk funds have generated double-digit returns.

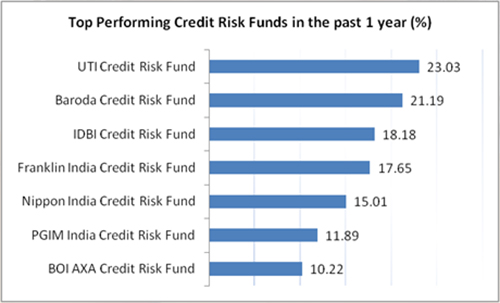

Graph 1: Credit Risk Funds turn top performers in the last one year

Data as on October 28, 2021

(Source: ACE MF)

The following combination of factors led to the improvement in debt market liquidity and credit profile of many issuers and thereby reduced the risk in the portfolios of many credit risk funds:

- The RBI was quick to announce various measures to infuse liquidity and support the economic growth amid the pandemic crisis. The following were among the measures that prevented the credit crisis from deepening:- Loan moratorium and one-time restructuring of loan- Relaxation of default recognition norms- Emergency Credit Guarantee Scheme- Long Term Repo Operations and Targeted Long Term Repo Operations

- The economy is better placed than it was in the last year, since most economic activities are now back to pre-COVID levels. After the devastating effects of the first and second wave of COVID-19 pandemic, GDP growth has turned positive from December 2020 quarter. The growth measures announced by the government amid the pandemic, easing of lockdown restrictions, decline in daily COVID-19 cases, acceleration in vaccination drive, are likely to boost the economic growth as well as profitability of corporates in the coming quarters.

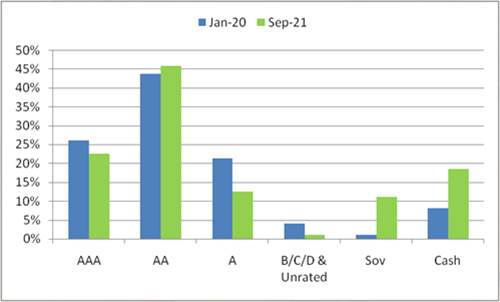

- Fund managers of Credit Risk Funds too have turned cautious and have upped their exposure to safer instruments such as sovereign rated government securities and cash (see graph below). They have moved from instruments rated A, B, C, D, and unrated securities to relatively safer AA segment. Notably, SEBI had asked credit risk funds to hold at least 10% of their net assets in liquid assets, including cash and government securities.

Graph 2: Fund managers of Credit Risk Funds are turning cautious

Data as on September 30, 2021

(Source: ACE MF)

Should you invest in Credit Risk Funds?

The improvement in economic activities and growth in corporate earnings bode well for credit risk funds. Improvements in credit profile of issuing companies could provide credit risk funds with more investment opportunities.

However, the events related to entities such as IL&FS and DHFL have shown us that even high-rated instruments can default. The risk intensifies further if a scheme holds higher allocation to moderate to low rated instruments. Certain low-rated issuers may find it difficult to improve their balance sheets even if the economy as a whole is witnessing sanguine growth.

It is important to note that very few funds in the credit risk category have shown consistency in performance. Moreover, at times the rewards were not attractive enough to justify the high risk that this category undertakes.

Table: Very few funds in Credit Risk Funds have shown consistency in performance

| Scheme Name | Absolute (%) | CAGR (%) | ||

| 1 Year | 2 Years | 3 Years | 5 Years | |

| HDFC Credit Risk Debt Fund | 8.69 | 9.80 | 9.76 | 8.47 |

| ICICI Pru Credit Risk Fund | 7.63 | 9.27 | 9.52 | 8.73 |

| IDFC Credit Risk Fund | 5.98 | 7.20 | 8.26 | — |

| Kotak Credit Risk Fund | 7.35 | 7.50 | 8.44 | 7.87 |

| SBI Credit Risk Fund | 6.45 | 8.10 | 8.13 | 7.77 |

| Axis Credit Risk Fund | 7.75 | 8.56 | 7.74 | 7.60 |

| Aditya Birla SL Credit Risk Fund | 8.73 | 7.30 | 7.25 | 7.59 |

| Category Average – Credit Risk Fund | 10.87 | 4.78 | 3.78 | 4.73 |

| Category Average – Banking & PSU Debt Fund | 4.32 | 7.45 | 8.67 | 7.68 |

| Category Average – Corporate Bond Fund | 4.57 | 7.77 | 8.67 | 7.58 |

Data as on October 28, 2021

Direct plan – Growth option considered

(Source: ACE MF)

As you can see in the table above, that various schemes in debt mutual fund categories such as Banking & PSU Debt Fund and Corporate Bond Fund have performed consistently well over the longer time horizon. Moreover, these funds have achieved superior returns without exposing the portfolio to higher risk.

Investors, who prefer safety of capital should completely avoid investing in credit risk funds because this category is prone to high volatility. If you are an aggressive investor then too you should avoid making credit risk funds part of the core portion of your fixed income portfolio.

Consider relatively safer categories such as Gilt Fund, Banking & PSU Debt Fund, Corporate Bond Fund, Dynamic Bond Fund, and Liquid Fund for your debt mutual fund portfolio. Allocate assets in these categories depending on your risk profile and investment horizon.

Also assess the following factors to pick the best schemes within each category:

- The portfolio characteristics of the debt schemes

- The average maturity profile

- The corpus & expense ratio of the scheme

- The rolling returns

- The risk ratios

- The interest rate cycle

- The investment processes & systems at the fund house

This article first appeared on PersonalFN here

{kind=link}