The Indian banking system is undergoing a big transformation lately. The talks of a bad bank have raised hopes that India might finally come out of the vicious circle of Non-Performing Assets (NPAs). Moreover, the government’s objective to make India a USD 5 trillion economy is also expected to provide the impetus to the capex cycle. This leaves India’s banking and financial services sector in a sweet spot with the potential fall in NPAs and resumption of credit growth.

This brings us to the question: Should you invest in the best performing banking and financial services sector funds to capitalize on this opportunity?

First, let’ see how big the opportunity is…

The proposed National Asset Reconstruction Company Limited (NARCL) may help the Indian economy reboot its banking system. The NARCL would enable banks to free up capital, boost profits and raise further capital to strengthen their financial position.

The NARCL is also expected to resolve the existing bad assets worth Rs 2 lakh crore, which are in excess of Rs 500 crore each. In phase I, NARCL is expected to mop up Rs 90,000 crore of fully-provisioned bad debts and in the subsequent phase, banks can transfer even the assets with lower provisions. This, in turn, may infuse at least Rs 30,000 crore in the banking system.

The NARCL will do nearly 85% acquisitions against Security Receipts (SRs). Any rigorous recovery on this component may give further upside to the overall collections of the banks. The government has provided a 5-year guarantee of Rs 30,600 crore.

However, Finance Minister Ms Nirmala Sitharam, while addressing the 74th Annual General Meeting of the Indian Banking Association (IBA), recently clarified that the NARCL is not a “bad bank” as in the case in the United States, because it is purely bank driven. She further added saying, “The government will closely work together with IBA and they would be able to restructure and sell the NPAs. In other words, the Indian Debt Resolution Company Ltd. (IDRCL) would serve as the assessment management company for the NARCL.

It’s noteworthy that the quality of banking assets, especially amongst the large corporate segment, has not deteriorated further in the recent past despite the two waves of the COVID-19 pandemic. The delinquencies have mainly come from the retail and Micro, Small, and Medium Enterprises (MSMEs), which have been impacted the most amid the pandemic.

Nevertheless, as the economy has started opening up, the collections as reported by some of the biggest retail and housing finance companies lenders have started picking up. India Ratings has forecasted a stable outlook for Indian banks in FY22 with an estimation of 8.9% credit growth in the current fiscal.

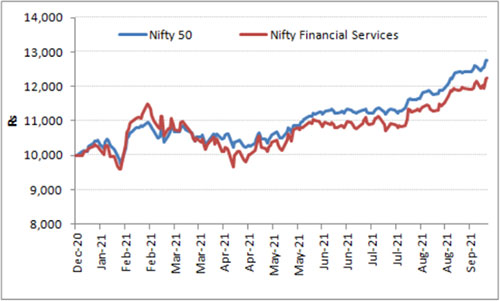

As you might be aware, financials have underperformed leading market indices on a Year-to-Date (YTD) basis. As depicted by the graph below an investment of Rs 10,000 each in Nifty 50 and Nifty Financial Services would have fetched 27.7% and 22.5% returns, respectively, on a Year-to-Date (YTD) basis.

Although the financial services sector has been a laggard in the present market rally (see graph below), it is expected to catch up fast. Indian banks have managed to raise significant capital during the pandemic, which offers more visibility about the turnaround of the sector post-pandemic.

Graph: Nifty Financial Services (YTD) v/s Nifty 50

Data as of September 24, 2021

Base: Rs 10,000

(Source: NSE India, PerosnalFN Research)

The weight of financial stocks in Nifty 50 and Nifty 500 is 37.6% and 31.3% respectively as of August 31, 2021. As far as the Nifty Financial Services Index is concerned, obviously, it is extremely skewed. For instance, HDFC Ltd. and HDFC Bank which together account for 10.8% in the Nifty 500 index, comprise 40.6% in the Nifty Financial Services Index. The top 5 holdings of the index make up over 73% of Nifty Financial Services.

With more non-lending financial services companies getting listed on the exchanges, including the insurance companies and brokerage houses, more constituents are getting added to the index. And interestingly, the outperformance of Nifty Financial Services over the Nifty Bank in the past 1 year indicates that a few Non-Banking Financial Companies (NBFCs) and non-lending financial institutions have fared better than the traditional ones. The returns generated by banking and financial services funds further support these findings.

Table: Performance of Banking and Financial Services Sector Funds

| Scheme Name | Returns (%) | ||||

| Absolute | CAGR | ||||

| 1 Year | 2 Years | 3 Years | 5 Years | 7 Years | |

| Sundaram Fin Serv Opp Fund | 82.3 | 18.4 | 20.8 | 14.6 | 14.9 |

| Tata Banking & Financial Services Fund | 71.9 | 17.1 | 20.5 | 17.0 | – |

| Invesco India Financial Services Fund | 73.6 | 18.4 | 19.5 | 16.8 | 17.8 |

| SBI Banking & Financial Services Fund | 74.4 | 18.3 | 19.4 | 17.6 | |

| Taurus Banking & Fin Serv Fund | 75.2 | 15.4 | 18.6 | 15.3 | 13.6 |

| Aditya Birla SL Banking & Financial Services Fund | 91.2 | 18.4 | 17.0 | 13.8 | 17.8 |

| ICICI Pru Banking & Fin Serv Fund | 84.0 | 16.2 | 16.8 | 14.4 | 16.7 |

| Baroda Banking & Fin Serv Fund | 70.5 | 12.3 | 16.2 | 12.3 | 12.6 |

| IDBI Banking & Financial Services Fund | 74.0 | 14.6 | 14.4 | – | – |

| LIC MF Banking & Financial Services Fund | 67.6 | 11.1 | 14.3 | 7.8 | – |

| Nippon India Banking & Financial Services Fund | 94.7 | 14.8 | 13.4 | 12.6 | 13.7 |

| UTI Banking and Financial Services Fund | 85.0 | 12.1 | 12.0 | 10.3 | 12.2 |

| Nifty Financial Services – TRI | 84.7 | 18.3 | 21.6 | 18.4 | 17.2 |

| NIFTY BANK – TRI | 85.6 | 12.1 | 15.1 | 14.1 | 13.9 |

Data as of September 24, 2021

Direct Plan and Growth Option are considered. Returns expressed are point-to-point.

(Source: ACE MF, PersonalFN Research)

Mutual fund schemes such as Baroda Banking & Financial Services Fund, Tata Banking & Financial Services Fund, and LIC MF Banking & Financial Services Fund, to name a few, have underperformed over in the recent rally. They have allocated a comparatively higher corpus to leading private sector banks that have underperformed broader markets.

Against that, top performers such as Nippon India Banking & Financial Services Fund, Aditya Birla SL Banking & Financial Services Fund, and ICICI Prudential Banking & Fin Services Fund invested aggressively in NBFCs, insurance companies, and investment infrastructure companies among others that that proved multi-baggers in the market rally.

That being said, over the longer periods, funds having concentrated exposure to private-sector lenders have outperformed.

So, should you invest in banking and financial services sector funds at this juncture?

The banking and Financial Service sector will, of course, be the key engine for India’s economic growth. But the NARCL and bad bank per se would not really help reduce NPAs; all it would do is masquerade it. Delinquency will continue to be reported, though it would be transferred to the NARCL from the books of banks. And it is also possible that with this arrangement, banks may indulge in impetuous lending to show better credit growth. You see, credit growth is healthy for the economy when it comes with minimal NPA problems. The actual reduction in NPA happens when the bank recovers the money lent with interest thereon. While there is a government guarantee, it is only up to Rs 30,600 crore.

In my view, it would be better to avoid taking exposure to Banking & Financial Services Sector Funds. While the Reserve Bank of India (RBI) in its Financial Stability Report (FSR), released in July 2021, foresees less stress compared to its previous estimate in the FSR released in January, in reality, the stress on the banking system could be more if banks lend recklessly.

As per the RBI, under a baseline projection, assuming GDP grows at 9.5% in FY22, the gross Non-Performing Assets (NPAs) of the banking sector could rise to 9.8% in March 2022 against 7.5% in March 2021. Under medium stress scenario where GDP growth is 6.5%, the gross NPAs of the banking sector could rise to 10.4%; while in case of severe stress, assuming the GDP growth is 0.9%, gross NPAs may rise to 11.2%.

Here’s a worthwhile investment strategy to follow…

Considering the present market conditions, you would be better off realigning your portfolio to ensure that the risk is well-adjusted according to your risk appetite while you endeavour to earn appealing returns to achieve your investment objectives and envisioned financial goals.

I recommend following a time-tested Core & Satellite Approach. It is an investment strategy pursued by some of the most successful equity investors across the world to build an equity portfolio.

The term ‘Core’ applies to the more stable, long-term holdings of the portfolio, while the term ‘Satellite’ applies to the strategic portion that would help push up the overall returns of the portfolio across market conditions. The ‘Core’ holding should comprise around 65%-70% of your equity mutual fund portfolio and consist of a Large-cap Fund, Flexi-cap Fund, and Value Fund/Contra Fund. The ‘Satellite’ holdings of the portfolio can be around 30%-35%, comprising of Mid-cap Funds and an Aggressive Hybrid Fund.

By wisely selecting among the best equity mutual fund schemes, structuring your portfolio, and then timely reviewing the Core and Satellite portions and the holdings therein, you would be able to add stability to the portfolio and strategically boosting your portfolio returns at the same time.

UTI Flexi Cap Fund (earlier known as UTI Equity Fund, and one of the oldest in the Indian mutual fund industry) is one such scheme that has displayed a commendable performance track record by holding a flexible portfolio across market capitalisations (large-cap, mid-cap, and small-caps) and sectors. It also provides you with the opportunity to participate in the potential upside of the banking and financial services sector without exposing you to the concentration risk.

As per the portfolio as of August 31, 2021, Bajaj Finance, HDFC Bank, HDFC Ltd., and Kotak Mahindra Bank feature in the top-10 holdings of UTI Flexi Cap Fund which collectively comprised 20.5% of the portfolio. In total, Banking and Financial stocks account for 24.7% of the portfolio of UTI Flexi Cap Fund as of August 31, 2021.

These portfolio traits of UTI Flexi Cap Fund suggest that the fund manager is betting predominantly on the private-sector lenders and there too restricting to the names which, according to the market’s interpretation, have a proven track record of good corporate governance. Importantly, these are index stocks; thus, these would reflect the potential upside in the financial sector.

Nonetheless, it appears that the fund manager has taken a conscious call of being underweight on financials since the weight of the sector in UTI Flexi Cap Fund is lower than that in Nifty 500.

When you have such a scheme in your portfolio you need not take any unwarranted risk with sector funds.

When building a portfolio of equity funds with the ‘Core & Satellite’ Approach, here are some fundamental rules to follow:

- Consider funds that have a strong track record of at least 5 years and those that have been amongst the top performers in their respective categories.

- The schemes should be diversified across investment styles and fund management.

- Ensure that each selected scheme abides with its stated objectives, indicated asset allocation, and investment style.

- You should not only invest across investment styles (such as growth and value), but also across fund houses.

- The mutual fund schemes should be managed by experienced and competent fund managers and belong to fund houses that have well-defined investment systems and processes in place.

- Not more than two schemes managed by the same fund manager should be included in the portfolio.

- Not more than two schemes from the same fund house shall be included in the portfolio.

- Each scheme that is to be included in the portfolio should have seen an outperformance over at least three market cycles.

- You should restrict the count of mutual fund schemes in your portfolio to seven.

Considering the Indian equity markets are at an all-time high, I suggest opting for the Systematic Investment Plan (SIP) route while taking the ‘Core and Satellite’ approach to invest in the best equity mutual fund schemes.

If you follow the ‘Core and Satellite’ approach prudently, it can accrue the following benefits:

- Facilitates optimal diversification with the best equity mutual fund schemes

- Reduces the need to frequently churn your entire portfolio

- Reduces the risk to your portfolio

- Enables you to benefit from a variety of investment styles and strategies

- Creates wealth while cushioning the downside

- Holds the potential to outperform the market

The Core & Satellite investment strategy may work for you in 2021 and beyond.

That said, consider your risk profile, broader investment objective, financial goals, and time in hand to accomplish the envisioned financial goals. This will help you align your investment well and make a prudent investment decision.

Happy Investing!

This article first appeared on PersonalFN here

{kind=link}