Are you taking unwarranted risks to generate superior returns on your mutual fund portfolio?

Don’t ignore this question unless you are 100% sure that you are not.

Risks and returns go hand in hand. Any mutual fund scheme that fetches you high returns can, potentially, exposes you to high risks as well. Sectoral and Thematic Funds for instance.

They help you take a focused exposure to a particular sector or theme that is benefiting or is likely to benefit from the overall macroeconomic and business environment. But since investing in Sectoral and Thematic Funds primarily involves a top-down investment approach, the time at which you enter and exit play a crucial role in deciding your investment success.

And according to me, this is the biggest risk associated with Sectoral and Thematic Funds, because no one has really succeeded in timing the markets consistently for a very long time. At PersonalFN, we discourage investors from timing the market.

According to the data published by the Association of Mutual Funds in India (AMFI) on March 31, 2020, the total Assets Under Management (AUM) of Sectoral and Thematic Funds was Rs 49,844 crore. And by July 31, 2021, the AUM of Sectoral and Thematic Funds swelled to Rs 1,23,936 crore.

As of July 31, 2021, 10.5% of total equity AUM was in Sectoral and Thematic Funds. The AUM of these funds was greater than that of value funds, focused funds, multi-cap funds, dividend yield funds, and large & mid-cap funds, individually. The folio count of Sectoral and Thematic funds increased to 90.50 lakh as of July 2021 from 65.30 lakh March last year. Sectoral and Thematic funds comprised just around 6% of the total equity AUM in March 2020.

What changed during the pandemic?

Global central banks infused unprecedented liquidity in the financial system to tackle the adverse effects of the COVID-19 pandemic. Most central banks adopted an accommodative monetary policy stance.

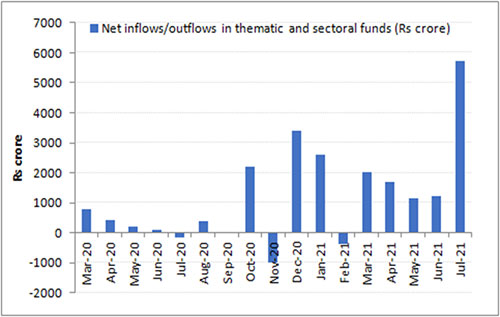

But honestly, nobody imagined that the Indian equity markets will come such a long way — more than double across capitalizations — from their March 2020 lows. In this rally, Sectoral and Thematic funds have been the biggest beneficiaries (see Graph below).

Graph: Net Inflows/Outflows Sectoral and Thematic Funds

Data as of July 2021

(Source: AMFI, PersonalFN Research)

The AUM of Sectoral and Thematic Funds have risen mainly due to the Indian equity market scaling new highs, the IPO buzz, and a spate of New Fund Offers (NFOs) from mutual fund houses during the pandemic. The new launches included Sectoral and Thematic Funds and a variety of other mutual fund schemes. In July 2021, two NFOs: Axis Quant Fund and HDFC Banking and Financial Services Fund, collectively mopped up Rs 3,536 crore.

Going forward as well, a couple of Sectoral and Thematic Funds and other NFO launches are lined up by mutual fund houses. Fund houses are making hay while the sun shines, capitalising on the favourable market sentiments in the race to garner more AUM.

Table 1: How Sectoral and Thematic Funds fared versus other sub-categories of Equity Funds

| Category | Returns (%) | ||||

| Absolute | CAGR | ||||

| 1 Year | 2 Years | 3 Years | 5 Years | 7 Years | |

| Technology Funds | 87.9 | 51.7 | 32.7 | 27.6 | 21.2 |

| Pharma & Healthcare Funds | 35.7 | 47.8 | 26.1 | 14.1 | 14.3 |

| Small-cap Funds | 80.6 | 44.6 | 19.1 | 17.4 | 18.4 |

| Energy & Power Sector Funds | 61.0 | 35.8 | 18.1 | 16.5 | 14.0 |

| Mid-cap Funds | 61.0 | 35.6 | 17.1 | 16.0 | 16.9 |

| Thematic Funds | 55.6 | 30.4 | 16.7 | 15.9 | 14.2 |

| Services Industries Funds | 57.3 | 30.4 | 13.7 | 12.9 | 14.0 |

| Contra Funds | 55.6 | 30.2 | 15.3 | 16.2 | 15.4 |

| Multi Cap Funds | 58.1 | 30.0 | 16.7 | 15.7 | 15.2 |

| Dividend Yield Funds | 50.7 | 29.0 | 14.2 | 14.6 | 12.9 |

| Large & Mid Cap Funds | 53.8 | 28.6 | 14.9 | 15.2 | 15.3 |

| Consumption Funds | 44.3 | 27.3 | 13.7 | 15.4 | 14.9 |

| Infrastructure Funds | 62.8 | 26.9 | 12.8 | 12.5 | 11.8 |

| Focused Funds | 48.5 | 26.5 | 14.1 | 14.9 | 14.3 |

| MNC Funds | 39.7 | 26.5 | 11.0 | 12.2 | 14.7 |

| Flexi Cap Funds | 49.8 | 26.4 | 14.7 | 14.8 | 14.1 |

| Value Funds | 53.8 | 26.4 | 12.2 | 13.3 | 14.0 |

| Large Cap Funds | 45.6 | 23.5 | 13.4 | 13.8 | 13.1 |

| Auto Sector Funds | 34.2 | 21.1 | 0.4 | 5.0 | 9.5 |

| Global Funds | 27.8 | 20.2 | 14.1 | 13.7 | 10.7 |

| Banking & Financial Services Funds | 56.0 | 15.5 | 9.1 | 12.9 | 14.0 |

| NIFTY 50 – TRI | 47.2 | 23.5 | 13.8 | 15.1 | 12.5 |

| Nifty Midcap 150 – TRI | 61.6 | 34.8 | 15.2 | 16.5 | 17.2 |

| Nifty Smallcap 250 – TRI | 77.3 | 39.0 | 13.4 | 13.0 | 13.1 |

| NIFTY 500 – TRI | 50.4 | 26.0 | 13.6 | 14.8 | 13.2 |

Data as of August 20, 2021

Growth Option and Direct Plans considered

(Source: ACE MF, PersonalFN Research)

Compared to the pre-pandemic levels, Technology Funds, Pharma and Healthcare Funds, Energy & Power Sector Funds have done well. Thus, among the funds that existed in March 2020, Technology Funds, Pharma funds garnered the maximum AUM.

In recent times, with awareness about environmental issues, social issues, and governance-related factors on the rise; investors have also shown a keen interest in ESG Funds.

On the other hand, Consumption Funds, MNC Funds, Banking and Services sector Funds, and Infrastructure Funds have witnessed noticeable net outflows, owing to their lacklustre performance.

This perhaps indicates that investors switched out of categories that didn’t perform and moved into those where wealth creation looked promising. In other words, investors preferred to go with the rising tide and sort of attempted to time their investment moves.

Table 2: Recent performance pushed up the long-term averages of certain schemes

| Category | Returns (%) | ||||

| Absolute | CAGR | ||||

| 1 Year | 2 Years | 3 Years | 5 Years | 7 Years | |

| SBI Small Cap Fund | 62.6 | 39.6 | 19.9 | 22.5 | 24.8 |

| Aditya Birla SL Digital India Fund | 91.8 | 57.1 | 34.7 | 30.6 | 23.6 |

| ICICI Pru Technology Fund | 108.0 | 59.6 | 37.1 | 31.5 | 23.4 |

| Mirae Asset Emerging Bluechip | 59.3 | 34.9 | 21.9 | 21.2 | 22.8 |

| Nippon India Small Cap Fund | 86.5 | 46.8 | 20.6 | 22.4 | 21.8 |

| Kotak Small Cap Fund | 97.6 | 53.1 | 26.7 | 20.5 | 21.6 |

| SBI Technology Opp Fund | 92.5 | 48.7 | 32.7 | 26.7 | 21.0 |

| Axis Small Cap Fund | 71.4 | 40.0 | 27.0 | 21.5 | 20.7 |

| Kotak Emerging Equity Fund | 66.9 | 37.9 | 20.2 | 18.0 | 20.5 |

| Canara Rob Emerg Equities Fund | 54.9 | 34.3 | 16.8 | 18.8 | 20.1 |

| NIFTY 500 – TRI | 50.4 | 26.0 | 13.6 | 14.8 | 13.2 |

Data as of August 20, 2021

Growth Option and Direct Plans considered

(Source: ACE MF, PersonalFN Research)

The evaluation of 203 unique equity schemes (including Sectoral and Thematic Funds) suggests that the remarkable rally since the COVID-19 pandemic in mid and small-caps — across many sectors — helped generate market-beating returns and pushed up the longer period averages of most mutual fund schemes, particularly those with dominant exposure to mid-and-small cap companies.

What to expect from Sector and Thematic Funds in 2021 and beyond?

If excess liquidity got these funds success since the pandemic began in March 2020, normalisation of monitory policies in the major developed markets may cause a quick unwinding. In Emerging Market Economies (EMEs) such as Brazil, Mexico, and Russia the central banks have already raised interest rates.

While themes such as ESG and quant strategies provide you with reasonable diversification, other categories of Sectoral and Thematic funds expose you to concentration risk.

If you recall, Infrastructure Funds and Power Sector Funds were extremely popular in the last multi-year bull market of 2003-08. Unfortunately, those who had invested in NFOs, lured by the NAV of Rs 10 towards the end of the cycle, couldn’t recover their capital for years.

If you invest in Sectoral and Thematic Funds thinking that this will help you accelerate your portfolio’s return, you may be proved wrong if the underlying sector or theme fails to perform.

In the current market scenario, where equity markets are scaling new highs and chances of some correction (5% to 10% from the current overheated levels) cannot be ruled out, taking concentration risk with Sectoral and Thematic funds may not be a very wise thing to do.

Instead, to earn optimal returns, I suggest following the ‘Core & Satellite Approach’ –a time-tested investment strategy adopted by some of the most successive equity investors in the world.

The term ‘Core’ applies to the more stable, long-term holdings of the portfolio, while the term ‘Satellite’ applies to the strategic portion that would help push up the overall returns of the portfolio, across market conditions.

The ‘Core’ holding should comprise around 65%-70% of your equity mutual fund portfolio and consist of a Large-cap Fund, Flexi-cap Fund, and Value Fund/Contra Fund. The ‘Satellite’ holdings of the portfolio can be around 30%-35%, comprising of a Mid-cap Fund and an Aggressive Hybrid Fund.

By selecting schemes wisely, structuring the portfolio between the Core and Satellite portions, you will be able to add stability to the portfolio and at the same time strategically boost your portfolio returns.

Note, Sectoral and Thematic Funds neither find a place in the ‘Core’ nor ‘Satellite’ portion of the portfolio.

You mainly need a diversified equity fund for your ‘Core & Satellite’ mutual fund portfolio.

To build a ‘Core & Satellite’ mutual fund portfolio of some of the best diversified equity mutual fund schemes, here are some ground rules:

- Consider funds that have a strong track record of at least 5 years and have been amongst the top performers in their respective categories.

- The schemes should be diversified across investment styles and fund management.

- Ensure that each selected scheme abides with its stated objectives, indicated asset allocation, and investment style.

- You should not only invest across investment styles (such as growth and value), but also across fund houses.

- The mutual fund schemes should be managed by experienced and competent fund managers and belong to fund houses that have well-defined investment systems and processes in place.

- Not more than five schemes managed by the same fund manager should be included in the portfolio.

- Not more than two schemes from the same fund house shall be included in the portfolio.

- Each scheme that is to be included in the portfolio should have seen an outperformance over at least three market cycles.

- You should restrict the count of mutual fund schemes in your portfolio to seven.

And once the portfolio is created, monitor it regularly (bi-annually) rather than timing the market.

You see, a sensibly constructed “Core and Satellite” portfolio of equity mutual funds adduces the following six benefits:

- Facilitates optimal diversification

- Reduces the need to frequently churn the portfolio

- Reduces the risk profile to your portfolio

- Enables you to enjoy the benefits of a variety of investment strategies

- Creates wealth cushioning the downside

- Holds the potential to outperform the market

Given that volatility in the Indian equity market would intensify in the near future, I suggest taking the Systematic Investment Plan (SIP) route as you build the portfolio of equity-oriented mutual fund schemes following the ‘Core and Satellite’ approach.

This article first appeared on PersonalFN here

{kind=link}