Retirement is a phase where you lead a worry-free life and reap the fruits of your hard work. Assuming that you had made prudent investment choices during your work life, you would have accumulated a good retirement corpus for your golden years.

Now the question arises, how should you manage your investment portfolio once you have retired? This is important because your regular source of income stops and you will depend on these investments to manage expenses and meet contingencies during your retirement years.

Considering the current low interest rate environment, earning inflation-beating returns from bank deposits will be a challenging task. Therefore, to lead a financially independent life even after retirement, you need to have a proper financial plan in place.

Recently, one of our esteemed readers of PersonalFN’s Daily Wealth Letter Mr S Kumaresan reached out to us. Mr Kumaresan is a retiree and wants to explore an investment option in Equity Savings fund. If you too are a retiree and are looking to invest in mutual funds post retirement, then read on to know if Equity Savings Funds are a suitable category to invest in.

What are Equity Savings Funds?

Equity Saving Funds are hybrid mutual funds that aim to generate stable returns from investment in equity, debt, and arbitrage opportunities. These funds have a mandate to invest minimum 65% of its assets in equity and equity-related instruments (including arbitrage) along with minimum 10% of its assets in debt.

By investing in arbitrage opportunities, fund managers aim to exploit the price difference in the cash and derivative segment of the equity market. This difference makes Equity Savings Fund less volatile when compared to Aggressive Hybrid Fund and pure equity schemes where the equity portion is mostly unhedged (non-arbitraged).

The minimum hedged and unhedged portion in an Equity Savings Fund differs from one scheme to another. The scheme has to mention the minimum hedged and unhedged exposure it will have at any given point in the scheme information document (SID).

Equity Savings Funds have the flexibility to invest across market caps. Most schemes in the category predominantly invest in large-cap stocks with some tactical allocation to mid-cap and small-cap stocks. While Equity Savings Funds aim to identify arbitrage opportunities to reduce volatility, such opportunities are not always available. In such situations, the unhedged exposure of the portfolio can rise substantially, say 40% or more. This can make the portfolio prone to higher volatility.

Moreover, if the scheme has higher exposure to mid-cap and small-cap stocks, the risk can intensify further. Most schemes in the category have mid and small-cap exposure in the range of 10%-20%.

Similarly, for the debt exposure, Equity Savings Funds have the flexibility to invest across credit profiles and duration. If the scheme has significant allocation to debt papers below AAA rating, it could expose investors to credit risk.

Should retirees consider investing in Equity Savings Funds?

It is important to note that Equity Savings Funds do not offer guaranteed returns. Its performance will depend on the equity market movement, arbitrage opportunities available, as well as the interest rate and credit environment. Moreover, the performance of the category (over the 3-year and 5-year period) when compared to other debt funds or even hybrid funds category has been nothing to boast about.

When you are young, you have time on your side to make up for any potential losses and therefore you can invest in riskier avenues. On the other hand, retirees cannot take much risk with their money. The priority is to maintain a regular flow of income while at the same time to generate inflation-beating returns on the corpus they have accumulated.

Accordingly, a debt-oriented portfolio would be best suited for your needs. Choose from relatively safer debt mutual fund categories such as, Banking & PSU Debt Funds, Liquid Funds, and other short duration debt funds. In addition, to accomodate the rising cost of living, it makes sense for senior citizens to allocate 25%-30% of the investment pool to equities via Large-cap mutual funds and Aggressive Hybrid Funds.

And because Gold has proved its potential as an efficient portfolio diversifier, it makes sense to allocate some of your assets in it. Consider allocating 5%-10% of your investment portfolio in the segment, preferably via Gold Exchange Traded Funds (ETFs) or Gold Savings Fund.

Table: Allocation to mutual funds for retirees

| Asset Class | Allocation |

| Debt | |

| Banking & PSU Debt Fund | ~70% |

| Liquid Fund | |

| Equity | |

| Large Cap Funds | ~25% |

| Aggressive Hybrid Fund | |

| Gold | |

| Gold Fund | ~5 |

Note: The table is for illustrative purpose only

Diversify across equity, debt, and gold asset class by assessing whether you want to follow a conservative approach or are willing to take some risk. Rebalance your portfolio from time to time if an asset allocation drifts significantly from the initial allocation. By rebalancing your portfolio to your standard allocation, you will adjust the allocation of each asset class to their fair level.

When you choose debt mutual funds, be careful of the credit risk the fund manager is taking. Stick to debt funds that are safely managed and focus primarily on instruments issued by Government and Quasi-Government issuers. Remember, debt funds are not risk-free.

How retirees can earn regular income from mutual funds?

Systematic Withdrawal Plan (SWP) is an effective way to earn regular income from mutual funds. Through an SWP, you can withdraw a fixed sum of money from a mutual fund scheme regularly (monthly, quarterly, half-yearly or annually) and hold the potential to clock returns on the remaining investments over a period of time. It not only provides you with a fixed source of income, but also inculcates a disciplined approach while spending.

Following are the benefits of opting for SWP:

- Facilitates better planning of withdrawals, as per your need

- Enables rupee-cost averaging

- The remaining investments/units would benefit from the power of compounding

- Can be one of the effective ways to source your retirement needs

That said, keep in mind that the withdrawals are subject to tax.

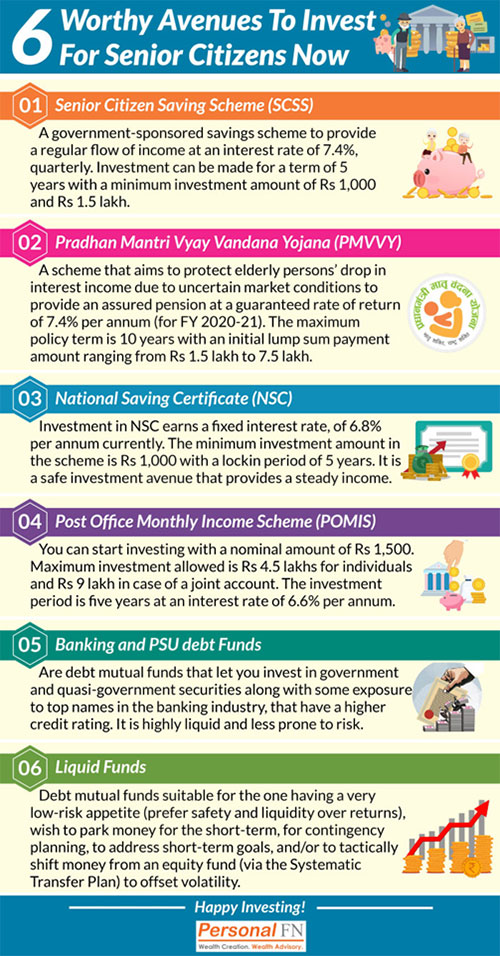

Apart from mutual funds, retirees should also consider setting aside some funds in small savings schemes such as, Senior Citizen Saving Scheme, Pradhan Mantri Vyay Vandana Yojana, National Saving Certificate, etc. Even though the interest rate on these schemes are currently at a multi-year low, they are safe avenues that can provide stable source of income.

You can pave the path to blissful retired life by investing sensibly and diversifying your investments across asset classes and investment avenues. Moreover, you should recognize your risk profile and be optimally insured for health and life.

This article first appeared on PersonalFN here

{kind=link}