The second wave of COVID-19 has been brutal for India and has affected all socioeconomic classes. The last two months have thrown the Indian healthcare system in total disarray. The daily caseload surpassed the 4 lakh mark in the first week of May 2021. Thankfully, the new cases have dropped substantially of late, and currently, as of May 30, 2021, India has reported 1.27 lakh new cases — the lowest daily count in the last 50 days.

Although the vaccination drive has been progressing, it is at a slower pace (due to shortage) and has taken a toll on the economy and jobs. As per the Centre for Monitoring India Economy (CMIE), nearly 1 crore Indians have lost jobs in May 2021 (21.3 crore Indians have received at least one jab so far).

Having been hit hard by the second wave, the states have adopted a cautious approach to unlock activities – many have extended lockdowns and restrictions. And thus, the financial aftereffects of this on the economy and its people at large are likely to be severe.

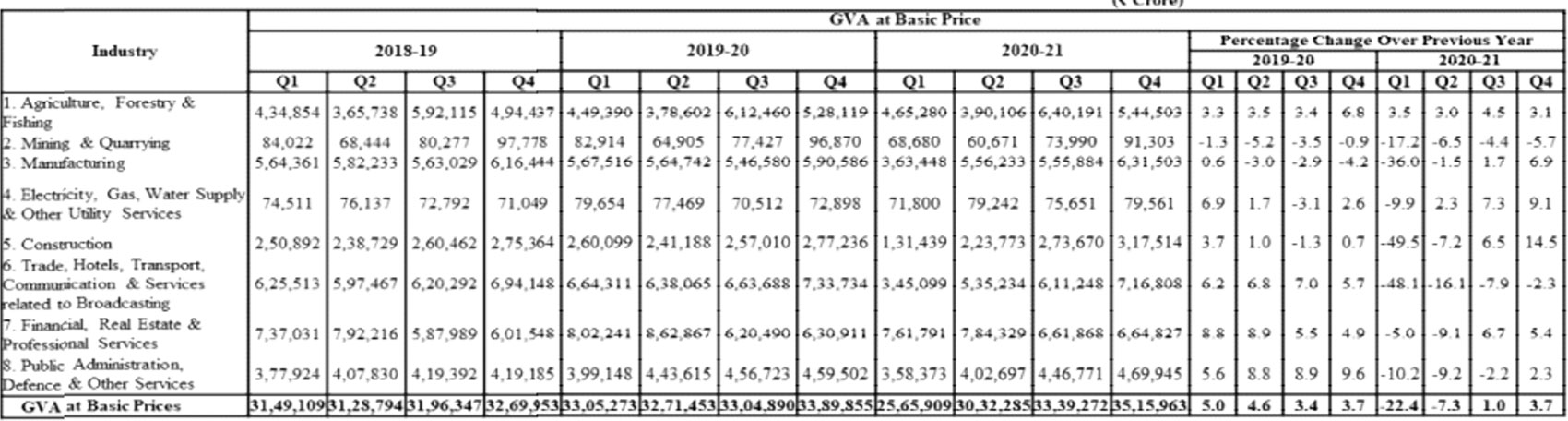

The Q4FY21 GDP data has reported an expansion of +1.6% backed by certain components of the GDP and growth measured by Gross Value Added (GVA) stood at +3.7%. GDP growth at constant prices (2011-12) is estimated at -7.3% in 2020-21 (FY21) via-á-vis +4.0% in 2019-20 (FY20), while the GVA growth at -6.2% in FY21 vis-á-vis +4.1% in FY20.

The Private Final Consumption (PFC) has jumped to +2.7% in Q4FY21 from -2.8% in the previous quarter, but contracted -9.1% for the full year FY21. The Gross Fixed Capital Formation (GCFC), which speaks about the investments in the country, also rose to +10.9% in Q4FY21 from +2.6% in the previous quarter, while for the full year FY21, it contracted by -10.8%.

Table 1: Quarterly Estimates of GVA at Basic Prices for 2020-21 (at 2011-12 prices)

(Source: Press Release, Ministry of Statistics & Programme Implementation Government of India)

In my view, nothing positive can be extrapolated from those numbers about the potential growth in Q1FY22 and Q2FY22. The lockdowns or restrictions enforced since mid-April 2021 by many states to contain infections would most likely weigh on the ensuing GDP growth readings for Q1FY22 and Q2FY22. Plus, if we face the third wave in August-September, as medical experts foresee, that may weigh heavily on the GDP data for a quarter or two.

That said, the Indian equity markets seem unmoved by all these developments. As the situation on the pandemic front has improved a bit over the last few days, animal spirits are getting reinvigorated in the Indian equity markets, and the bellwether indices are once again scaling new highs.

Graph 1: Nifty 50 TRI v/s Nifty 50 P/E

Data as of May 28, 2021

(Source: NSE)

The performance of India Inc. has been satisfactory in Q4FY21 despite the toughest business conditions. Even the full-year numbers for FY21 have been quite encouraging. At Rs 5.31 lakh crore, corporate profits as a percentage of GDP hit a 10-year high of 2.63% in FY21, as reported by the Business Standard. The profit growth of Nifty 50 companies in FY22 and FY23 is estimated to outdo India’s nominal GDP growth.

Post Q4FY21 numbers, the P/E multiple of Nifty 50 has dropped noticeably despite the on-going rally. At present, the Nifty 50 trades at the P/E of 29x on a Trailing Twelve Month (TTM) earnings, while the Nifty 500 and Nifty Mid Smallcap 400 Index commands a P/E of 31 and 38 respectively.

In other words, earnings of mid and small-cap companies aren’t keeping pace with the movement in their stock prices, which have moved way ahead of their fundamentals. Thus, you can conclude that the margin of safety is better available in the large-cap space than in the mid and small caps.

Since the second wave has dented household savings, at some point it is likely to dampen the overall demand in the economy. This phenomenon may affect smaller unorganized and regional players more. Even the listed small and mid-sized companies in the organised space may have to encounter challenges ahead, while some heavyweights in the index might do relatively well.

As you may know, large-sized companies are usually leaders in their respective industries. These companies are less likely to be impacted by the potential economic slowdown. The large-cap domain is highly liquid compared to mid and small-cap space; and, mind you, liquidity plays a very important role in tough market conditions. Given this, a large-cap fund in my view may offer growth with stability, and therefore, it should ideally form part of the core portfolio of every investor.

Having said that, what matters is your selection. You can’t afford to invest blindly because not all large-cap mutual fund schemes may do well.

Table 2: How have large-cap funds performed? Take a look…

| Scheme Name | Absolute (%) | CAGR (%) | ||||

| 6 Months | 1 Year | 2 Years | 3 Years | 5 Years | 7 Years | |

| Canara Rob Bluechip Equity Fund(G)-Direct Plan | 19.3 | 58.9 | 21.7 | 18.1 | 17.9 | 15.2 |

| Axis Bluechip Fund(G)-Direct Plan | 15.1 | 52.2 | 18.5 | 16.5 | 17.4 | 15.3 |

| Kotak Bluechip Fund(G)-Direct Plan | 20.7 | 65.2 | 18.3 | 15.2 | 14.8 | 14.9 |

| BNP Paribas Large Cap Fund(G)-Direct Plan | 17.6 | 52.8 | 17.4 | 15.1 | 14.5 | 14.7 |

| Mirae Asset Large Cap Fund(G)-Direct Plan | 19.4 | 63.1 | 15.5 | 14.7 | 16.8 | 16.6 |

| IDBI India Top 100 Equity Fund(G)-Direct Plan | 21.6 | 62.0 | 19.2 | 14.0 | 14.0 | 13.9 |

| UTI Mastershare(G)-Direct Plan | 19.8 | 62.1 | 17.4 | 14.0 | 14.7 | 13.9 |

| PGIM India Large Cap Fund(G)-Direct Plan | 20.1 | 62.7 | 15.8 | 13.9 | 14.0 | 13.9 |

| Edelweiss Large Cap Fund(G)-Direct Plan | 18.2 | 62.0 | 16.3 | 13.6 | 15.1 | 14.2 |

| Franklin India Bluechip Fund(G)-Direct Plan | 29.6 | 71.8 | 17.1 | 13.6 | 13.1 | 13.3 |

| Category average | 19.8 | 59.5 | 15.2 | 13.0 | 14.1 | 13.4 |

| NIFTY 50 – TRI | 19.4 | 64.3 | 15.0 | 14.4 | 15.1 | 12.6 |

| NIFTY 100 – TRI | 20.0 | 63.8 | 15.3 | 13.7 | 15.1 | 13.0 |

Data as of May 28, 2021

(Source: ACE MF, PersonalFN Research)

We considered large-cap schemes that have at least 3 years of track record for analysis. Out of 28 such schemes, only 12 outperformed the Nifty 50 Total Return Index (TRI) over the last 3 years. The average returns generated by large-cap schemes on 1-year, 3-year, and 5-year timeframes have been lower than the returns generated by Nifty 50 TRI. This highlights that selection is the key!

Note that the role of a large-cap fund in the portfolio isn’t really to accelerate wealth creation, but rather to provide some stability to the portfolio by outperforming the benchmark index.

At this point, I would like to share with you a secret time-tested investment strategy some of the most successful equity investors across the world follow to build an equity portfolio. It is called the ‘Core & Satellite’ Investment Strategy.

The term ‘Core’ applies to the more stable, long-term holdings of the portfolio, while the term ‘Satellite’ applies to the strategic portion that would help push up the overall returns of the portfolio, across market conditions.

By wisely structuring and timely reviewing the Core and Satellite portions and the holdings therein, you would be able to add stability to the portfolio and at the same time strategically boost your portfolio returns.

The ‘Core’ holding should comprise around 65-70% of your equity mutual fund portfolio and consist of a large-cap fund, multi-cap fund, and a value style fund. Whereas, the ‘Satellite’ holdings of the portfolio can be around 30-35% comprising of a mid-cap fund, a large & mid-cap fund, and an aggressive hybrid fund.

While you add equity mutual fund schemes to your investment portfolio based on the Core & Satellite strategy, here a few fundamental rules to follow:

- Consider funds that have a strong track record of at least 5 years and have been amongst the top performers in their respective categories

- The schemes should be diversified across investment styles and fund management

- Ensure that each selected scheme abides with its stated objectives, indicated asset allocation, and investment style

- You should not only invest across investment styles (such as growth and value) but also across fund houses

- The mutual fund schemes should be managed by experienced and competent fund managers and belong to fund houses that have well-defined investment systems and processes in place

- Not more than five schemes managed by the same fund manager should be included in the portfolio

- Not more than two schemes from the same fund house shall be included in the portfolio

- Each scheme that is to be included in the portfolio should have seen an outperformance over at least three market cycles

- You should restrict the count of mutual fund schemes in your portfolio to seven

Moreover, after the portfolio is constructed, make a point to review it at least bi-annually. The allocation to the satellite portfolio should change based on the market outlook. If the outlook is extremely gloomy, you may avoid mid-caps altogether and add more exposure to aggressive hybrid funds to add stability.

Given the uncertainty looming and that the Indian equity market would remain very volatile until normalcy returns’, I suggest opting for the Systematic Investment Plan (SIP) route while you build the portfolio of equity-oriented mutual fund schemes following the ‘Core and Satellite’ approach.

Moreover, do not forget to align your investments with your risk appetite, broader investment objective, financial goals, and time horizon to accomplish the envisioned financial goals.

Following the ‘Core & Satellite’ approach while investing in equity mutual funds would adduce the benefits such as:

- Facilitate optimal diversification among equity mutual fund schemes

- Reduce the need to frequently churn your entire portfolio

- Reduce the risk to your portfolio

- Enable you to benefit from a variety of investment styles and strategies

- Create wealth cushioning the downside

- Help you potentially outperform the market

Note, the Core & Satellite investment strategy may work for you in 2021 and beyond.

This article first appeared on PersonalFN here

{kind=link}