The COVID-19 pandemic is proving regressive for India’s socio-economic growth. India made impressive progress on poverty alleviation between 2011 and 2019, but now the lockdowns and restrictions imposed to curb the spread of the deadly virus are wreaking havoc.

According to Washington-based Pew Research Center, 26.2 crore people came out of poverty in the last decade before the coronavirus pandemic hit the world badly last year. However, considering the virus-induced economic slowdown and job losses in India, more citizens are feared to have gotten trapped in the clutches of poverty yet again. Nearly 6.7 crore people from the middle-income and lower-income groups got marginalized while the number of poor rose sharply to 7.5 crore amidst the ongoing pandemic, as per Pew Research. These numbers point out that India’s 3-4 years’ of progress on poverty alleviation has been negated by the COVID-19 pandemic.

According to the Center for Monitoring Indian Economy (CMIE) data, 72.2 lakh people have lost their jobs in April and several salaried people are vulnerable to losing their jobs, going forward. A more worrisome observation is that the unemployment rate of 7.97% in April 2021, largely reflects agriculture job losses — which are seasonal — and does not show the full impact of the second wave. Mr Mahesh Vyas, MD and CEO of CMIE, believes India’s unemployment problem is more structural in nature.

The aforesaid developments bring us to a question: Is India’s consumption-led growth story waning and is likely to get severely impacted in the coming quarters?

Well, the signs are already visible.

The overall auto sales are down by a massive 30% in April 2021. The impact on the recent month-on-month sales is also visible. And due to the complete nationwide lockdown in April 2020, the year-on-year numbers aren’t comparable. Even the two-wheeler sales did worse and fell 35.4%. The second wave of COVID-19 has surely hit discretionary spending severely.

Dull consumer sentiment has weighed on the demand for consumer durable goods such as air conditioners and refrigerators (also known as white goods) compared to the peak season. The prohibition on the use of oxygen for the industrial activity (justifiably so, to make up for the oxygen shortage amid rising cases), shortage of manpower (not necessarily because of migration but because a number of people falling ill), and regional lockdowns, are some of the primary reasons why white goods manufacturers have been experiencing production losses.

The ongoing second wave of infections is so strong that 50% of the total daily cases reported in the world are from India. The daily death toll has crossed the 4,000 mark. You can imagine how badly the consumer sentiment might have got shaken up.

The RBI’s bi-monthly Consumer Confidence Survey for March 2021 (report released in April 2021) revealed that 81.1% of the respondents expected the rate of inflation to increase over one year. Also, the respondents were less enthused about spending on non-essential items and expected to reduce their spending over the next one year as well. Worryingly, a majority of respondents felt the employment situation was likely to deteriorate one year ahead.

Note that the survey was conducted during March 2021 and, thus, does not reflect the complete effects of the second wave on consumer confidence, inflation expectations and spending. With millions of Indians contracting the virus and many of them succumbing to it; discretionary spending is likely to drop further. On this backdrop, it is possible that the RBI Consumer Confidence Survey data for May 2021 could also plummet.

This makes me believe that the consumption theme is losing steam and the performance of consumption funds in the foreseeable future may drag.

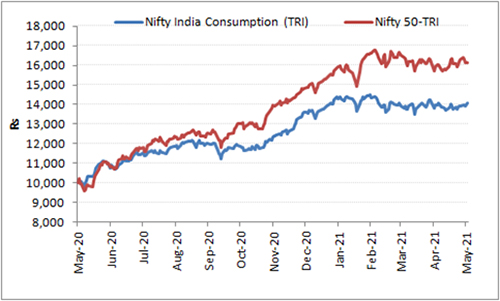

Graph: Nifty India Consumption Total Return Index v/s Nifty 50 Total Return Index

Data as of May 14, 2021

(Source: NSE, PersonalFN Research)

Since the upward movement of the Indian equity market since March 2020, the Nifty India Consumption Total Return Index (TRI) has underperformed the bellwether, Nifty 50 TRI. Pricey valuations negatively impacted the performance of the FMCG basket, and mobility-related restrictions due to strict lockdowns dragged the autos. During the unlocking from September 2020 to February 2021, the consumer durables and autos did display substantial improvement but could not sustain the growth when the second wave of COVID-19 gripped the nation.

Table 1: Report card of thematic consumption-oriented mutual fund schemes

| Scheme Name | Absolute (%) | CAGR (%) | ||||

| 6 Months | 1 Year | 2 Years | 3 Years | 5 Years | 7 Years | |

| Quant Consumption Fund | 50.5 | 115.3 | 38.7 | 20.9 | 22.5 | 21.2 |

| Nippon India Consumption Fund | 23.0 | 59.7 | 21.3 | 12.6 | 11.5 | 13.0 |

| Mirae Asset Great Consumer Fund | 20.0 | 58.6 | 18.4 | 11.8 | 18.1 | 17.5 |

| Aditya Birla SL Mfg. Equity Fund | 29.1 | 67.5 | 21.9 | 9.1 | 14.1 | – |

| Tata India Consumer Fund | 14.7 | 47.0 | 16.4 | 7.2 | 18.3 | – |

| ICICI Pru FMCG Fund | 11.1 | 32.4 | 8.3 | 7.1 | 12.4 | 12.6 |

| UTI India Consumer Fund | 13.7 | 40.5 | 14.7 | 6.6 | 11.3 | 10.6 |

| SBI Consumption Opp Fund | 30.4 | 69.3 | 14.3 | 6.4 | 15.0 | 14.7 |

| BNP Paribas India Consumption Fund | 17.8 | 47.4 | 22.9 | – | – | – |

| ICICI Pru Bharat Consumption Fund | 14.6 | 42.6 | 13.2 | – | – | – |

| Mahindra Manulife Rural Bharat and Consumption Yojana | 21.2 | 50.7 | 13.2 | – | – | – |

| Average returns generated by consumption funds | 22.4 | 57.4 | 18.5 | 10.2 | 15.4 | 14.9 |

| Average returns generated by diversified equity funds | 26.1 | 72.3 | 20.1 | 11.2 | 14.9 | 15.9 |

| NIFTY Consumption-TRI | 12.3 | 39.1 | 14.0 | 7.1 | 12.1 | 13.0 |

| NIFTY 50 – TRI | 16.1 | 61.4 | 15.4 | 12.1 | 14.7 | 12.3 |

Data as of May 12, 2021

Direct Plan and Growth Option considered.

Source: (ACE MF, PersonalFN Research)

The performance of thematic consumption-oriented mutual fund schemes has been a mixed bag. If you exclude Quant Consumption Fund, the performance may rather appear muted. Quant Consumption Fund is running a diversified equity fund by extending the meaning of consumption beyond its obvious connotation. Moreover, its portfolio is dominated by mid and small-cap companies. It is not only investing in consumer-facing companies but also power utilities, banks, refineries etc.

Interestingly, ICICI Prudential Mutual Fund has two schemes focusing on the consumption theme, and surprisingly it hasn’t merged them yet.

You see, thematic funds allow you to take advantage of attractive investment opportunities in a much-focused manner. However, despite following this top-down approach for its stock selection process, the stock-specific risks and the concentration risks have weighed heavily on thematic funds. Not all schemes have been able to outperform the bellwether Nifty 50 TRI over a 3-year and 5-year time periods.

What to expect from consumption funds in future?

Nearly a little over 56% of the Nifty India Consumption Index is made up of FMCG companies. Autos and telecom sectors account for 19.9% and 9.2% respectively. In other words, three sectors — Consumer Goods, Automobile, and Telecom — make up around 85% of the Nifty India consumption index.

And interestingly, the response of consumer spending to these sectors is unlikely to be uniform. For instance, there’s hardly any scope for citizens to lower their mobile phone bills and data plan expenditures. Thus, the telecom space may not be as much impacted. But then again, India’s telecom sector, as you may know, is witnessing fierce competition — making gains for few companies, while resulting in losses for the others.

Similarly, within FMCG too, spending on life essentials such as toothpaste, oils etc. won’t be impacted much but that on cosmetics and beauty products may drop substantially. Likewise, consumer durables or autos may face an impact for a long time due to weak consumer sentiments amidst the pandemic.

Currently, although a number of consumer-facing listed companies have reported impressive growth numbers in Q4FY21, the rising input costs are now threatening to affect their profitability. To make things worse, their ability to pass on the price rises is substantially capped due to the weak consumer sentiment.

The performance of the thematic consumption-oriented mutual fund schemes would largely depend on their exposure to various underlying sectors. So, do not make a very simplistic assumption that India’s demographic dividend will always translate into a wealth-creating idea for you with India’s consumption-led growth story. You need to revisit your strategy.

I would like to share with you a secret time-tested investment strategy followed by some of the most successful equity investors across the world to build an equity portfolio. It is called the ‘Core & Satellite’ Investment Strategy.

The term ‘Core’ applies to the more stable, long-term holdings of the portfolio, while the term ‘Satellite’ applies to the strategic portion that would help push up the overall returns of the portfolio, across market conditions.

By wisely structuring and timely reviewing the Core and Satellite portions and the holdings therein, you would be able to add stability to the portfolio and at the same time strategically boost your portfolio returns.

The ‘Core’ holding should comprise around 65-70% of your equity mutual fund portfolio and consist of a large-cap fund, multi-cap fund, and a value style fund. Whereas, the ‘Satellite’ holdings of the portfolio can be around 30-35% comprising of a mid-cap fund, a large & mid-cap fund, and an aggressive hybrid fund.

While you add equity mutual fund schemes to your investment portfolio based on the Core & Satellite strategy, here a few fundamental rules to follow:

- Consider funds that have a strong track record of at least 5 years and have been amongst the top performers in their respective categories

- The schemes should be diversified across investment styles and fund management

- Ensure that each selected scheme abides with its stated objectives, indicated asset allocation, and investment style

- You should not only invest across investment styles (such as growth and value) but also across fund houses

- The mutual fund schemes should be managed by experienced and competent fund managers and belong to fund houses that have well-defined investment systems and processes in place

- Not more than five schemes managed by the same fund manager should be included in the portfolio

- Not more than two schemes from the same fund house shall be included in the portfolio

- Each scheme that is to be included in the portfolio should have seen an outperformance over at least three market cycles

- You should restrict the count of mutual fund schemes in your portfolio to seven

Moreover, after the portfolio is constructed make it a point to review it at least bi-annually. The allocation to the satellite portfolio should change based on the market outlook. If the outlook is extremely gloomy, you may avoid mid-caps altogether and add more exposure to aggressive hybrid funds to add stability.

Following the ‘Core & Satellite’ approach to equity investing would yield you the following benefits:

- Facilitate optimal diversification among equity mutual fund schemes

- Reduce the need to frequently churn your entire portfolio

- Reduce the risk to your portfolio

- Enable you to benefit from a variety of investment styles and strategies

- Create wealth cushioning the downside

- Help you potentially outperform the market

Given the uncertainty looming, and the Indian equity market would remain very volatile until normalcy returns’, prefer the Systematic Investment Plan (SIP) route while you build the portfolio of equity-oriented mutual fund schemes following the ‘Core and Satellite’ approach. Moreover, do not forget to align your investments with your risk appetite, broader investment objective, financial goals, and time horizon to accomplish the envisioned financial goals.

Note, the Core & Satellite investment strategy may work for you in 2021 and beyond.

{kind=link}