The pandemic situation in India has worsened over the past few weeks. With the world’s highest-ever surge at 3.32 lakh reported on April 22, India’s active COVID-19 cases have breached the 24 lakh mark. Experts believe that we are at least 3-4 weeks away from reaching the peak of second wave.

Many parts of the country have implemented lockdown-like restrictions to slow down the spread of the disease and to boost the healthcare infrastructure overburdened by the rising cases.

The grim statistics, as well as the restrictions to curb the spread, have triggered worry that economic activities would be impacted which will delay the recovery process. Recently, RBI Governor Mr Shaktikanta Das too expressed that rapidly rising cases of COVID-19 is the single biggest challenge to ongoing recovery in the Indian economy.

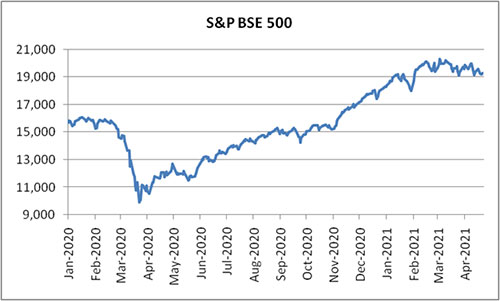

Consequently, the equity market volatility has intensified. The S&P BSE 500 index is down around 5% from its all-time high of March 03, 2021 and may witness further selloff in the coming days.

Graph: Equity market have turned volatile amid the second wave of COVID-19

Data as on April 22, 2021

(Source: ACE MF, PersonalFN Research)

It is said that investors often feel the pain of loss more acutely than they feel the pleasure of gain. Market volatility can cause you to take irrational decisions that could impact your financial well-being.

But if you have invested in equity mutual funds for your long term goals, you should know that market and volatility go hand-in-hand. The silver lightning here is that impact of volatility on your portfolio can be mitigated.

Here is how you can protect your mutual fund portfolio from downside risk amid the COVID second wave:

1) Focus on your goal

It is always advisable to align investment with your goals. Equity mutual funds are long term investment vehicle and therefore short term blip on the market should not worry you. If the goal for which you are investing is still at least 3-5 years away then there is no reason to think about redeeming or stopping your investment in equity mutual fund. Remember that frequent churning of the portfolio can do more harm than good to your long term plans and you may risk falling short of your financial goals.

That said, if your financial goal is nearing or if you are a conservative investor it would be better to gradually shift allocation from equity mutual fund to safer and less volatile assets such as debt fund. Ensure that you choose schemes (both equity and debt) carefully by assessing its worthiness based on various quantitative and qualitative parameters.

2) Don’t keep all your eggs in one basket

Depending on your risk appetite, financial goals, and investment horizon, your portfolio must be spread across a range of assets such as equity, debt, gold, and cash. Historical data suggests that no two asset classes move in the same direction always. When equities fall other asset classes such as gold may witness a surge in prices, and vice versa. In addition, the presence of debt securities in your portfolio can add the much needed stability and steady growth during uncertain and volatile market environment.

Once you have decided on your personalised asset allocation plan stick to it regardless of the market conditions and rebalance if necessary to earn better risk-adjusted returns.

3) Diversify

Just like it is important to spread investment across assets classes, it is equally important to invest across various sub-categories and investment style. Invest in a well-diversified portfolio of equity funds containing Large-cap Funds, Large & Mid Cap Fund, Multi Cap/Flexi Cap Fund, Mid Cap Fund, Aggressive Hybrid Fund, etc. By diversifying investment across market capitalisation you can benefit from the stability of large caps and the high growth potential of mid and small caps.

Though certain sub-categories like Small-cap funds and Thematic/sectoral fund have very high return potential, invest only if you have a very high risk appetite and limit the holding to around 10-20% of your assets.

It can also prove beneficial to diversify across investment styles – growth as well as value-oriented funds. Value funds act as a good portfolio diversifier when growth-oriented funds underperform.

4) Avoid timing the market

During extreme and volatile market conditions, investors tend to make investment decisions by trying to time the market. But the fact is, accurately forecasting the market movement is difficult even for seasoned investors. This is because economic, political, social, and other factors that affect the stock market are highly unpredictable. Besides, markets may continue to rise even if it is overvalued, and/or it could prolong its fall even after huge corrections.

So instead of trying to time your investment, opt for the SIP mode of investing in mutual funds. Investing regularly via SIP ensures that you automatically purchase more units when the NAV is lower and less units when the NAV is higher. This will save you from the worry of timing the market. As you purchase more when the price is low, you are rewarded with higher returns over a period of time. You also benefit from low investment cost and the power of compounding of wealth.

5) Review your portfolio

After the portfolio is constructed make it a point to review it at least bi-annually. At times even high quality funds can trail its peers and the benchmark index if the investment strategies/styles adopted by the fund manager move out of favour. However, if your fund consistently lags in terms of risk-reward parameters across most time period and scores low on qualitative parameters it may be time to replace it with a better alternative. You do not want the portfolio returns to be dragged down by laggards.

The proceeds from redeeming inefficient schemes can be invested in worthy schemes that perform consistently well across various market phases and cycles.

At PersonalFN, we believe following the time-tested Core & Satellite Approach — a strategy followed by some of the most successful investors can help you build a robust all-weather portfolio with the best equity mutual fund schemes.

The term ‘Core’ applies to more stable, long-term holdings of the portfolio; while the ‘Satellite’ applies to the strategic portion that would help push up the overall returns of the portfolio in good market conditions.

As per this strategy, your ‘Core holdings’ should constitute around 60% of your entire equity mutual fund portfolio and include a Large-cap Fund, Multicap/Flexicap Fund, and a Value Style Fund. The ‘Satellite’ holdings may account for around 40% of your portfolio and comprise of a Mid-cap Fund, a Large-cap & Mid-cap Fund, and an Aggressive Hybrid Fund.

The allocation to the satellite portfolio can be changed based on the market outlook. By wisely reviewing the Core and Satellite portions and the holdings therein, you would be able to add stability to the portfolio and at the same time strategically boost your portfolio returns.

Following a sensible approach in the “Core and Satellite” strategy, will yield the following six key benefits:

- Facilitate optimal diversification among equity mutual fund schemes

- Reduce the need to frequently churn the portfolio

- Reduce the risk profile to your portfolio

- Enable you to enjoy the benefits of a variety of investment styles

- Create wealth cushioning the downside

- Potentially outperforms the market

Note, the Core & Satellite investment strategy may work for you in 2021 and beyond; it is an evergreen approach that brings along immense benefits.

This article first appeared on PersonalFN here

{kind=link}