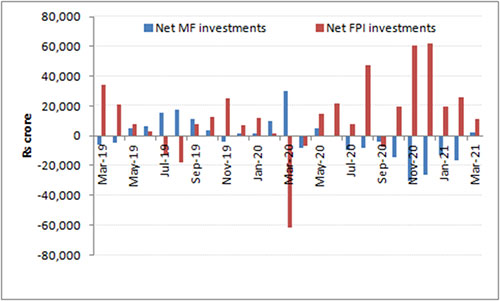

A strong second wave of COVID-19 has increased the volatility in the Indian equity markets. Foreign Portfolio Investors (FPIs), who net purchased Rs 2,74,502 crore worth of Indian equities since April last year, have now turned cautious; they tapered their investments in March 2021.

On the other hand, domestic mutual funds have turned net buyers to the tune of Rs 2,476 crore in the Indian equity markets in March 2021 for the first time in the last 10 months, perhaps seeing some value buying opportunity (and gauging the margin of safety) after witnessing a correction since the peak of 52,516.76 points (made on February 16, 2021) on the S&P BSE Sensex. That said, in FY21 domestic mutual funds were net sellers to the tune of Rs 1,23,826 crore in Indian equities.

Graph 1: FPI vs. MF activity in the secondary markets

Data of March 31, 2021

(Source: ACE MF, PersonalFN Research)

The other prominent reasons for domestic mutual fund turning net buyers in March 2021 could be…

Redemption pressure on equity mutual funds might have eased

While the data on the subscription and redemption is awaited –– and I will observe it minutely once it is released –– it appears that redemption pressure has eased for fund managers, and in certain sub-categories of equity mutual funds, investors have deployed their hard-earned money in the pursuit of wealth creation and to accomplish financial goals. Investors now are recognising that the returns on some traditional investment avenues are not very respectable once adjusted for inflation.

End of the season inflows in Equity Linked Savings Schemes (ELSS)

March is a busy month for tax planning, as most people keep investments in tax-saving investment avenues for the last minute. The Equity Linked Saving Schemes (ELSS), also known as tax-saving mutual funds, may have reported inflows given their ability to clock better returns over the three-year lock-in period or more when selected prudently. Plus, the fact that the lock-in period in the case of ELSS is the least compared to other tax-saving investment instruments.

A slew of New Fund offers

Quite a few fund houses such as Axis Mutual Fund, Aditya Birla Mutual Fund, and Nippon India Mutual Fund amongst others launched Index Funds in March 2021. This in turn could have also accelerated the net investments of mutual funds in the Indian equity markets.

Participation by mutual funds in IPOs

Indian companies raised over Rs 31,000 crore from the primary markets in FY21. Some companies that floated IPOs at attractive valuations and with robust underlying fundamentals perhaps encouraged domestic mutual funds to participate in the IPO rush, like many other participants. But it is also noteworthy that some IPOs despite high participation, did not list at a premium and the ones who did; could not continue to command the premium in the ensuing trading sessions post-listing.

Are Robinhood investors finally coming to terms with market realities?

Seeing the meteoric rise of the Indian equity market since its March 2020 lows, many Robinhood investors are entering the markets even at the market high. The total demat accounts in the country have touched a record high of over 5 crore in FY21, and more than a crore of these are newly opened during FY21.

However, the big concern is that many of these newbies who have embarked on a rollercoaster for an enthralling experience, to make fast profits; may not necessarily have the stomach for high risk and haven’t experienced the discomfort of deeper corrections so far.

In my view, if you wish to ride the volatility maturely, the Systematic Investment Plan (SIP) route offered by mutual funds is worthwhile (if the schemes are suitably selected and among the best performing ones) rather than timing the market — which could prove hazardous for wealth and health. What is important is the ‘time in the market’.

If you are SIP-ping into worthy mutual fund schemes, do not commit the mistake of discontinuing or stopping your SIPs. It could put brakes on the compounding process. Going forward, even if the market corrects or hits turbulence and volatility increases, the inherent rupee-cost averaging feature would help mitigate the risk involved while you endeavour to compound your hard-earned money. More units would be allotted against your SIP instalment when the market falls, and when the market begins to ascend again, it would compound your wealth. Keep in mind, by devising a sensible investment strategy you can be a successful investor.

With the S&P BSE Sensex around 50,000 levels and a strong second wave of COVID-19, I suggest following the ‘Core & Satellite’ approach. It is a strategy pursued by some of the most successful equity investors to build wealth.

The term ‘Core’ applies to more stable, long-term holdings of the portfolio; while the ‘Satellite’ applies to the strategic portion that would help push up the overall returns of the portfolio in good market conditions.

As per this strategy, your ‘Core holdings’ should constitute 65%-70% of your entire equity mutual portfolio and include a Large-cap Fund, Multicap/Flexicap Fund, and a Value Style Fund. The ‘Satellite’ holdings may account for 30%-35% of your portfolio and comprise of a Mid-cap Fund, a Large-cap & Mid-cap Fund, and an Aggressive Hybrid Fund.

Note that this allocation to the satellite portfolio should change based on the market outlook. If the outlook is extremely gloomy, you may avoid mid-caps altogether and add more exposure to aggressive hybrid funds to add stability.

By wisely reviewing the Core and Satellite portions and the holdings therein, you would be able to add stability to the portfolio and at the same time strategically boost your portfolio returns.

A sensibly built “Core and Satellite” portfolio of equity mutual funds brings with it six key benefits:

-

Facilitates optimal diversification

-

Reduces the need to frequently churn the portfolio

-

Reduces the risk profile to your portfolio

-

Enables you to enjoy the benefits of a variety of investment strategies

-

Creates wealth cushioning the downside

-

Potentially outperforms the market

Note, the Core & Satellite investment strategy may work for you in 2021 and beyond; it is an evergreen approach that brings along immense benefits. With a strategic portfolio of diversified equity funds, you can plan for your envisioned financial goals better.

This article first appeared on PersonalFN here

{kind=link}