Over the past couple of years, we have witnessed mutual fund houses launch a growing number of schemes in the passive investment style category such as Exchange Traded Funds (ETFs), Index Funds, and Fund of Funds (FoFs). The number of schemes in the passive funds category has risen from 193 in March 2020 to 224 in February 2021.

With this, the category seems to have caught investors’ attention — the average asset under management (AAUM) as well as the number of folios in the category have nearly doubled in the last one year. As a result, the category has witnessed net inflows in most of the months in the last one year even as equity funds saw consecutive months of massive outflows.

Earlier, most passive equity funds tracked only the large-cap index such as the Nifty 50 and S&P BSE Sensex, plus few sectors such as banking. However, in the recent months, mutual funds have launched passive funds that track various categories (Equity, Debt, Gold), Themes (ESG, Global), sectors (Pharma, IT), as well as other innovative products to help investors create a diversified portfolio.

[Read: Mutual Funds Launch Innovative Products. Are They Worth Investing in? Know Here…]

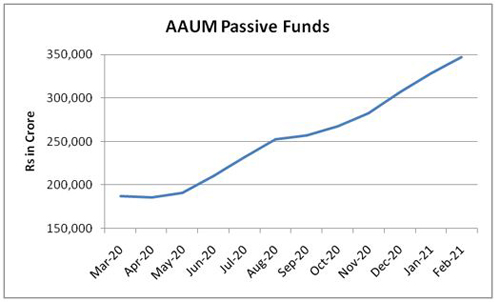

Graph: Steady rise in the AAUM of Passive Funds

Data as of February 28, 2021

(Source: AMFI)

Why are mutual fund houses increasingly launching passive funds?

In the last few years, due to the absence of a broad-based market rally amidst the prolonged economic slowdown, only a handful of stocks across market capitalisation have witnessed a surge in prices. Since mutual funds follow a single stock limit of 10% to avoid concentration risk, it prevents them from taking full advantage of the rally in these select stocks if it grows beyond the specified limit.

Moreover, SEBI’s norms on categorization of mutual funds to ensure that schemes remain true to label also created challenges for actively managed funds to create alpha since it limited the universe of stocks from which a scheme belonging to a particular category can invest.

Therefore, a significant number of actively managed mutual funds have not only found it increasingly difficult to generate sustainable alpha but have also underperformed their respective benchmark indices. This, in turn, has elicited investors’ interest towards passively managed funds.

Table: Category wise % of schemes underperforming benchmark indices

| Category | % of schemes underperforming on 3-year return basis |

| Flexi Cap Fund | 71% |

| Large & Mid Cap Fund | 68% |

| Large Cap Fund | 79% |

| Mid Cap Fund | 13% |

| Multi Cap Fund | 75% |

| Small cap Fund | 7% |

Data as on March 08, 2021

(Source: ACE MF, PersonalFN Research)

Should you invest in passive funds?

Passive funds provide a low-cost investment offering for investors looking to earn decent returns from equities by tracking the respective benchmark index and/or underlying fund and do not have the appetite for high volatility, making it ideal for new investors who have just started their investment journey. It is also a simple and convenient option for investors who find it difficult to choose the right fund from the plethora of available active funds.

However, with the slew of passive funds being launched across different market capitalisation, investment style, as well as attractive-looking themes, investors may find it difficult to build a portfolio of passive funds.

So if you are looking to invest in passive funds you can begin by investing in passive funds that track large-cap indices such as Nifty 50, S&P BSE Sensex, Nifty Next 50, and so on. You could also invest in funds that track broader indices such as Nifty 500 to gain exposure across market capitalisation.

As seen in the table above, actively managed large-cap funds, flexi-cap funds (that are usually large-cap biased), and multi-cap funds (the category held large-cap biased portfolio before SEBI’s recategorisation of multi-cap funds) have the most number of schemes underperforming the benchmark. Thus, a passive investment strategy can make more sense for this segment.

Once you have built a well-diversified portfolio of equity fund, you can consider investing up to 15-20% of your portfolio overseas passive funds that track indices such as Nasdaq 100, S&P 500, etc. to benefit from geographical diversification.

On the other hand, India being an emerging economy stocks in the mid-cap and small-cap segment have a better scope of outperformance over the long term. Going forward, as the economy recovers, the market could witness a sustainable broad-based rally and therefore, mid-cap funds and small-cap funds could generate superior returns. Thus, actively managed mid-cap funds and small-cap funds can still give the fund managers the opportunity to generate high alpha for its investors.

When you build a portfolio of mutual funds assess your financial goals, investment time horizon and risk appetite, and invest accordingly to create a diversified portfolio of large, mid and small cap stocks. While selecting passive funds, pick the one with low expense ratio and low tracking error to earn reasonably higher returns than the index over the long term.

However, keep in mind that market crash impacts passive funds as well. Unlike passive funds, actively managed funds are better poised to take advantage of dynamic market conditions and make tactical allocation in attractive looking stocks/sectors/market cap depending on the outlook.

During the market crash, the actively managed funds get the opportunity to pick strong companies available at attractive valuations. Hence, they can outperform the market with a remarkable margin during recovery and bull phase. Thus, if you pick the right scheme, it can reward you with high alpha over the long term. So, if your strategy is to get alpha-generating returns, passive funds may not be the right option for you.

The decision on whether to invest in an actively managed fund or passive fund, or a combination of both should depend on financial objective, investment horizon, and risk-taking ability. Ideally, while investing in equity funds ensure that you have a time horizon of 5-7 years to tide over the market volatility. And lastly, avoid investing in too many schemes as it can make it difficult to monitor its performance and eliminate the laggards.

This article first appeared on PersonalFN here

{kind=link}