The post-lockdown recovery seems to have taken an interesting turn. India’s GDP growth has returned to the positive, India’s Manufacturing Purchasing Manager’s Index (PMI) data for February is well-placed at 57.5 (backed by new orders and rise in production), and so is the Services PMI at 55.3 on improved demand and favourable market conditions.

In fact, the Services PMI data indicates the sharpest recovery over the last one year. Thus, the Composite PMI Index (which measures both, manufacturing and services activities) is well poised at 57.3 (noticeably better than the 8-year average reading) reflects the data released in February 2021.

However, a matter of concern is the escalating input cost; it is currently at an eight-year high. It remains to be seen if India’s economic growth is weighed by the rising input cost.

On this backdrop, evaluating the prospects of India’s financial sector, which is an important component of India’s GDP representing nearly 30% of the country’s economic output, becomes crucial. The financial services sector is the mainstay of the services economy in India. Banks and Non-Banking Financial Companies (NBFCs) usually tend to perform well when the economy is expanding and vice versa.

In Q3FY21 while India’s GDP clocked 0.4% growth, “Financial, Real Estate and Professional Services” made a stronger come back registering 6.6% growth.

This brings us to a question: As an investor, should you increase your bets or go overweight on the Banking and Financial Services sector at this juncture?

Well, that could be risky!

Some banks, NBFCs in financial services have, of course, multiplied investors’ wealth multifold over the last two decades. But it would be imprudent to skew your portfolio to the Banking and Financial Services sector in an attempt to outperform the broader markets. Such a strategy may not prove rewarding always. Over the last one year, although the Indian equity market witnessed a remarkable recovery, the Nifty Financial Services Index (which comprises of banks, NBFCs, insurance companies, etc.) faltered on wealth creation.

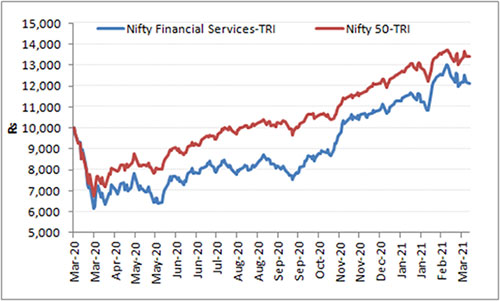

Graph: Nifty Financial Services-TRI vs. Nifty 50-TRI

Index values adjusted to the base: Rs 10,000

Data as of March 8, 2021

(Source: NSE, PersonalFN Research)

The Nifty 50 on the other, where financial services have a 39.5% weight in the index as per the factsheet National Stock Exchange (NSE)’s factsheet as of February 26, 2021, has fared far better. The Nifty 50-TRI generated +37.7% absolute returns over the last 1 year, while the Nifty Financial Services-TRI clocked an absolute return of +24.8%.

The graph above depicts that the Banking and Financial Services sector witnessed a steeper fall when the Indian equity markets plunged last year and the subsequent upswing did not compensate enough.

Table: A report card – Returns generated by Banking and Financial services Funds

| Scheme Name | Absolute (%) | CAGR (%) | ||||

| 6 Months | 1 Year | 2 Years | 3 Years | 5 Years | 7 Years | |

| SBI Banking & Financial Services Fund(G) | 47.6 | 25.9 | 18.9 | 18.8 | 23.5 | – |

| Tata Banking & Financial Services Fund(G) | 44.6 | 27.1 | 20.0 | 16.4 | 22.5 | – |

| Taurus Banking & Fin Serv Fund(G) | 46.2 | 23.1 | 17.6 | 15.6 | 19.5 | 16.5 |

| Sundaram Fin Serv Opp Fund(G) | 48.9 | 27.7 | 20.9 | 14.6 | 19.5 | 17.4 |

| Baroda Banking & Fin Serv Fund(G) | 48.8 | 22.0 | 16.5 | 13.7 | 17.8 | 16.4 |

| Invesco India Financial Services Fund(G) | 41.1 | 22.9 | 16.7 | 13.6 | 20.5 | 19.8 |

| Aditya Birla SL Banking & Financial Services Fund(G) | 49.1 | 25.0 | 13.6 | 11.3 | 19.1 | 19.8 |

| ICICI Pru Banking & Fin Serv Fund(G) | 48.5 | 24.5 | 12.3 | 11.2 | 20.6 | 20.5 |

| LIC MF Banking & Financial Services Fund(G) | 42.3 | 19.2 | 13.2 | 8.2 | 12.5 | – |

| Nippon India Banking Fund(G) | 53.3 | 22.7 | 8.9 | 7.6 | 16.4 | 16.8 |

| UTI Banking and Financial Services Fund(G) | 49.8 | 23.2 | 8.2 | 6.8 | 15.5 | 14.9 |

| IDBI Banking & Financial Services Fund-Reg(G) | 44.7 | 23.3 | 13.6 | – | – | – |

| Nifty Financial Services – TRI | 46.9 | 24.8 | 18.8 | 17.4 | 21.7 | 19.5 |

| NIFTY 50 – TRI | 32.7 | 37.7 | 17.8 | 14.9 | 16.3 | 14.0 |

| NIFTY 500 – TRI | 35.2 | 40.1 | 18.1 | 13.0 | 16.4 | 15.3 |

Data as of March 8, 2021

Direct Plans considered.

Point-to-point returns considered.

(Source: ACE MF, PersonalFN Research)

Speaking of the returns generated by Banking and Financial Services Funds, not many schemes have outperformed the Nifty Financial Services – TRI across time frames. When compared to the returns generated by the Nifty 50-TRI and Nifty 500-TRI over 3 years, again not all schemes have been able to generate enough alpha, many have failed. Only over longer time frames like 5 years and 7 years, certain schemes have fared well.

What are the likely reasons for underperformance?

The Nifty Financial Services Index is a 20-stock index and top-5 index constituents, namely HDFC Bank Ltd., HDFC Ltd., ICICI Bank Ltd., Kotak Mahindra Bank Ltd., and Axis Bank Ltd. account for over 75% of the index as per NSE’s factsheet as of February 26, 2021. PSU Banks have a limited representation in the index. In the run-up to the budget and even thereafter, PSUs have outperformed index-heavy private sector banks by far.

So, concentration risk is often hard to deal with even for fund managers. Likewise, the opportunities that may exist in the other spheres of the sector or theme viz. insurance, asset management, etc. may be given a trivial weight or missed at times. The effect of all this weighs on your portfolio returns. That is why making the right choice is the key when you add mutual fund schemes to your investment portfolio.

What is the purpose of skewing your investment to only Banking and Financial Service Funds if they lag in ferocious rallies such as these?

The Financial Stability Report (FSR) released by RBI doesn’t paint an encouraging picture as regards the asset quality of Indian banks. The FSR points out that NPAs could rise to 13.5% by September 2021 (from 7.5% in September 2020), and in the worst-case scenario could mount to 14.8%. Should banks do worse, Banking and Financial Services Funds could turn into wealth destroyers. Thus, placing high bets on these schemes would be risky.

I have said this quite a few times and will say this again—sectoral and thematic funds are risky and they can sometimes give you jitters. Hence, be smart and follow a prudent investment strategy when approaching equities.

I recommend that you follow the ‘Core & Satellite’ approach. It is a strategy followed by some of the most successful equity investors follow to build wealth — and particularly useful when Indian equity markets are near their all-time high.

The term ‘Core’ applies to more stable, long-term holdings of the portfolio; while the ‘Satellite’ applies to the strategic portion that would help push up the overall returns of the portfolio in good market conditions.

As per this strategy, a Large-cap Fund, Multicap/Flexicap Fund, and a Value Style Fund should comprise your ‘Core holdings’, which make up 65%-70% of your entire equity mutual portfolio. The ‘Satellite’ holdings may account for 30%-35% of your portfolio and comprise of a Mid-cap Fund, a Large-cap & Mid-cap Fund, and an Aggressive Hybrid Fund.

Following this approach may help you get the best of both worlds, i.e. the stability of large-sized companies in the Core holdings and the high return potential of smaller companies in the Satellite holdings. The Satellite portion could strategically boost your portfolio returns, in good market conditions, and on the other hand, the Core portion would provide the required stability during volatile market conditions.

Note that this allocation to the satellite portfolio should change based on the market outlook. If the outlook is extremely gloomy, you may avoid mid-caps altogether and add more exposure to aggressive hybrid funds to add stability.

To build a ‘Core & Satellite’ portfolio of some of the best equity mutual fund schemes, here are some ground rules:

- Consider funds that have a strong track record of at least 5 years and have been amongst the top performers in their respective categories.

- The schemes should be diversified across investment styles and fund management.

- Ensure that each selected scheme abides with its stated objectives, indicated asset allocation, and investment style.

- You should not only invest across investment styles (such as growth and value) but also across fund houses.

- The mutual fund schemes should be managed by experienced and competent fund managers and belong to fund houses that have well-defined investment systems and processes in place.

- Not more than five schemes managed by the same fund manager should be included in the portfolio.

- Not more than two schemes from the same fund house shall be included in the portfolio.

- Each scheme that is to be included in the portfolio should have seen an outperformance over at least three market cycles.

- You should restrict the count of mutual fund schemes in your portfolio to seven.

And once the all-weather portfolio is created, monitor it regularly (bi-annually) rather than timing the market

A sensibly constructed “Core and Satellite” portfolio of equity mutual funds adduces the following benefits:

Facilities optimal diversification

Reduce the need to frequently churn the portfolio

Reduce the risk profile to your portfolio

- Enable you to enjoy the benefits of a variety of investment strategies

Create wealth cushioning the downside

- Potentially outperform the market

The core & Satellite investment strategy may work for you in 2021 and beyond; it is an evergreen approach that brings along immense benefits. With a strategic portfolio of diversified equity funds, you can plan for your envisioned financial goals better.

This article first appeared on PersonalFN here

{kind=link}