The equity market has not witnessed a year as dramatic as 2020. During the year the market crashed to a multi-year low due to the uncertainty, a consequence of the pandemic, but it quickly soared to reach all time highs. This was something no expert had anticipated.

The bellwether Nifty 50 index has gained 75% from its March lows and around 9% on YTD basis, till December 21, 2020. Most of this has been on the back of aggressive inflows from foreign portfolio investors (FIIs) over the past couple of months.

Consequently, equity mutual fund returns improved as well with many schemes across categories delivering double-digit growth in the last one year period. But this has not stopped investors from redeeming their holdings in equity funds.

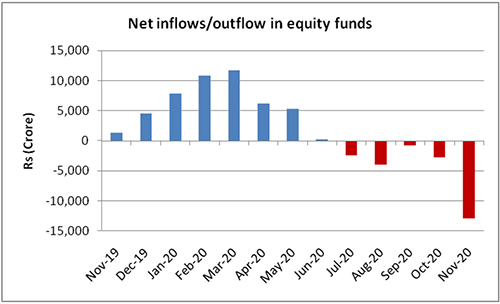

The latest data from AMFI shows that equity funds witnessed its worst monthly outflows in November at Rs 12,917 crore. This is the fifth consecutive month of outflows from equity funds.

Graph 1: Equity funds witness outflows for five months in a row

Data as of November 30, 2020

(Source: AMFI, PersonalFN Research)

Moreover, SIP contribution which is the preferred mode of investment for retail investors too saw a decline as compared to the previous month. SIP contributions in November stood at Rs 7,300 crore, 6.4% lower than the previous month and down 15.5% from its peak in March.

Why are investors redeeming equity funds?

A significant number of funds have not been able to outperform the respective benchmark index even on the longer time frames. Large cap funds and multi cap funds had the most number of schemes underperforming the benchmark.

As a result, investors who were patient with their investment in such funds for years saw the recent market rally as an opportunity to redeem their holdings and book profits. Notably, over the past few months there has been a spike in the number of new trading accounts, which indicates that direct equity investment through stocks has emerged as a new preferred mode.

Should you too book profits in equity funds?

The RBI expects GDP to recover and grow by 9.5% in the next financial year. Various global rating agencies have revised India’s GDP growth forecast upward due to the rebound in various economic activities, especially the manufacturing sector. India stands strong among emerging markets, as is evident from the recent hike in India’s weightage in the MSCI emerging market index to 8.7% from 8.1%.

The current low interest rate scenario and liquidity infusion by government and the RBI makes it easy for corporates to access capital that can be used for business expansion, innovation, and other growth measures. This bodes well for corporate earnings.

Moreover, there is hope of rollout of COVID-19 vaccine in India from early next year that can lead the country towards normalcy.

Furthermore, Finance Minister Ms Sitharaman has promised a ‘never before’ like budget and is seeking inputs from India Inc to push economy back on the growth track.

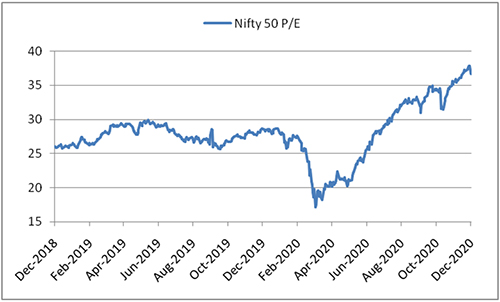

The thing is, the market seems to have already taken this into account and has run ahead of the fundamentals. The trailing Nifty 50 P/E is currently trading at 35x as compared to P/E of 25-28x we’ve seen over the past couple of years. The one-year forward P/E too is trading higher than its long term average. This is a clear indication of markets being in the overvalued zone.

It remains to be seen if the fundamentals improve as expected in the coming quarters to support the current valuations.

Graph 2: Nifty 50 P/E in an overvalued zone

Data as on December 21, 2020

(Source: nseindia.com, PersonalFN Research)

Due to expensive valuations, the upside on high growth stocks could be limited and may even witness correction to a certain extent. But remember that growth stocks may continue to have a long run despite high valuations.

As the saying goes, “No price is too low for a bear or too high for a bull”.

Going forward, mid and small caps could outperform as they are not as overvalued as large caps, provided there is economic recovery. Moreover, quality value stocks could make a comeback.

At the same time, it is important to track various domestic and global events that could impact the market and eventually your investments. Just recently, the market witnessed its worst fall in 7 months when reports of a new COVID-19 mutant strain in Britain that is expected to be more contagious spooked investors.

However, this does not mean investors should book profits from equity funds. If you have invested in equity funds for your long term goals, redeem it only in the following circumstances:

- The fund’s performance has consistently trailed the benchmark and category peers

- To gradually shift to safer avenues when your financial goal is approaching

- During portfolio rebalancing to maintain the desired asset allocation

- The fund objective changes and is no longer in congruence with your own objective

- The fund risk profile changes and doesn’t match your current risk appetite

- In case of a financial emergency when you have no other option

- You wish to adopt change in investment style (value, growth, blend, aggressive, conservative, etc.)

Given the volatile investment environment, be cautious in your approach. If you are making fresh investments do so in a staggered manner, preferably through the SIP route. Investing through SIP allows investors to mitigate the impact of volatility, average out the investment cost, and optimise returns through the power of compounding.

In an upward market phase, it is easy to assume high risk and invest in funds based on the recent attractive returns. But when the going gets tough, most funds fail to contain the downside and this prompts investors to redeem their investments.

Therefore, it is important to invest in a diversified portfolio of worthy schemes that performs well in bear and bull market phases. By doing this, you will eliminate the need to constantly churn your portfolio.

Additionally, diversify your investment across asset classes viz. Equity, debt, gold, and cash based on your personalised asset allocation plan that will help in generating better risk-adjusted returns.

This article first appeared on PersonalFN here

{kind=link}