The dramatic market recovery from the March lows is a pleasant surprise for all investors, including the seasoned institutional investors.

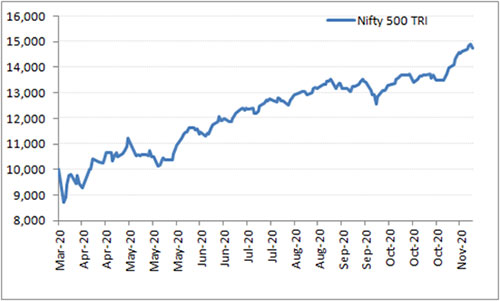

The Nifty 500 — an index which represents approximately 95% of the free-float market capitalization of Indian markets — has generated 70.3% returns since its March lows.

Graph: Going up from strength to strength

Data as on November 20, 2020

(Source: NSE, PersonalFN Research)

On this backdrop, we decided to evaluate the performance of various sub-categories of diversified equity schemes. The results aren’t encouraging. Except for the small-cap funds, mid-cap funds and contra funds, all other sub-categories of diversified equity schemes have underperformed broader markets over the last six months.

[Read: Why Do Certain Mutual Fund Schemes Underperform?]

Table 1: Performance of various sub-categories of diversified equity schemes

| Category Average | Absolute (%) | CAGR (%) | ||||

| 6 Months | 1 Year | 2 Years | 3 Years | 5 Years | 7 Years | |

| Small Cap | 54.4 | 21.0 | 8.5 | 0.9 | 9.6 | 18.1 |

| Contra | 43.7 | 12.8 | 10.2 | 6.0 | 11.7 | 15.8 |

| Mid Cap | 43.3 | 16.5 | 11.5 | 4.4 | 10.4 | 18.4 |

| Value Fund | 41.5 | 7.9 | 5.8 | 1.4 | 9.0 | 15.2 |

| ELSS | 39.1 | 8.9 | 9.6 | 5.0 | 10.4 | 15.1 |

| Large & Mid Cap | 38.9 | 9.0 | 10.2 | 4.6 | 10.9 | 15.8 |

| Multi Cap | 37.8 | 8.8 | 10.5 | 5.9 | 10.4 | 15.0 |

| Focused Funds | 37.1 | 9.0 | 11.2 | 6.0 | 11.2 | 15.4 |

| Large Cap | 37.0 | 7.4 | 10.7 | 6.9 | 10.6 | 13.7 |

| Dividend Yield | 35.0 | 9.7 | 6.4 | 2.3 | 8.7 | 12.6 |

| NIFTY 50 – TRI | 42.1 | 8.6 | 9.9 | 6.9 | 11.3 | 13.2 |

| NIFTY 500 – TRI | 43.1 | 9.5 | 9.8 | 6.1 | 11.1 | 13.5 |

Data as of November 20, 2020

Category Average returns of various sub-categories depicted considering Direct Plan and Growth Option

(Source: ACE MF, PersonalFN Research)

We also assessed the performance of 190 diversified equity schemes that have completed 3 years, just to see how they have fared individually.

Only 1 in every 4 schemes has outperformed broader markets over the past 6 months (see Table 2). And if you think this scenario may change dramatically if we consider the medium term, then on 3-year time period as well, only 40% equity-oriented schemes have managed to outperform the Nifty-500 Total Return Index (TRI).

Table 2: Not all diversified equity schemes have fared well

| Scheme Name | Absolute (%) | CAGR (%) | |||||

| Category | 6 Months | 1 Year | 2 Years | 3 Years | 5 Years | 7 Years | |

| Franklin India Smaller Cos Fund(G) | Small cap Fund | 55.4 | 8.8 | 2.1 | -2.8 | 7.3 | 18.0 |

| HSBC Small Cap Equity Fund(G) | Small cap Fund | 54.2 | 19.2 | 4.1 | -4.3 | 6.4 | 17.5 |

| Sundaram Mid Cap Fund(G) | Mid Cap Fund | 40.3 | 4.9 | 4.1 | -2.0 | 7.2 | 17.1 |

| Aditya Birla SL Pure Value Fund(G) | Value Fund | 39.2 | 5.2 | -1.0 | -7.5 | 6.1 | 16.7 |

| Franklin India Bluechip Fund(G) | Large Cap Fund | 39.1 | 7.0 | 7.2 | 4.1 | 8.5 | 12.0 |

| Nippon India Large Cap Fund(G) | Large Cap Fund | 39.0 | -2.7 | 3.1 | 2.8 | 9.0 | 14.5 |

| Kotak Standard Multicap Fund(G) | Multi Cap Fund | 38.9 | 6.5 | 10.9 | 7.3 | 12.7 | 17.6 |

| HDFC Equity Fund(G) | Multi Cap Fund | 36.9 | -3.6 | 2.8 | 1.0 | 8.3 | 13.1 |

| ICICI Pru Large & Mid Cap Fund(G) | Large & Mid Cap | 35.9 | 3.7 | 5.5 | 2.1 | 9.2 | 11.9 |

| L&T Equity Fund(G) | Multi Cap Fund | 34.8 | 5.9 | 6.2 | 3.6 | 8.7 | 13.3 |

| HDFC Focused 30 Fund(G) | Focused Fund | 33.8 | -5.6 | 0.9 | -2.8 | 4.9 | 11.5 |

| HDFC TaxSaver(G) | ELSS | 33.6 | -2.9 | 1.6 | -1.9 | 6.5 | 11.5 |

| SBI Focused Equity Fund(G) | Focused Fund | 33.1 | 8.8 | 14.9 | 9.6 | 13.4 | 18.6 |

| L&T Large and Midcap Fund(G) | Large & Mid Cap | 33.1 | 8.5 | 7.7 | 2.4 | 9.3 | 14.2 |

| ICICI Pru Focused Equity Fund(G) | Focused Fund | 28.7 | 13.0 | 7.5 | 5.7 | 9.8 | 12.2 |

| NIFTY 50 – TRI | 42.1 | 8.6 | 9.9 | 6.9 | 11.3 | 13.2 | |

| NIFTY 500 – TRI | 43.1 | 9.5 | 9.8 | 6.1 | 11.1 | 13.5 | |

Data as of November 20, 2020

Direct Plan and Growth Option considered.

(Source: ACE MF, PersonalFN Research)

Noting such underperformance, many experts and journalists have started questioning the effectiveness of actively managed mutual funds. But in my view, active vs. passive comparison is slightly misplaced and unwarranted at this juncture.

The underperformance on 3-year time period does not suggest that the active mutual funds have been the laggards for this long. It is the short term underperformance that has weighed on the medium-term performance of certain schemes. When looked at 7-year averages, most sub-categories of diversified equity schemes have managed to beat their key indices; built wealth for their investors in the long term.

Why certain actively managed equity diversified funds have lagged or underperformed despite markets touching an all-time high:

-

Only a handful of heavyweight stocks in the index gained disproportionately initially since the March 23, 2020 low. And recognizing that valuations in the small and midcap universe were very attractively placed, later it got the attention of several investors to these market capitalisation segments. That said, some small and mid-cap schemes segment could not overpower the underperformance of the past three years.

-

In the pre-COVID times, many mutual fund houses were underweight on 'Pharmaceuticals' and 'Technology' and overweight on 'Financials' and 'Consumer Goods' companies. Amid the challenging economic conditions, Technology and Pharmaceuticals outpaced the many other sectors. The FMCGs, despite better Q1FY21 and Q2FY21 results, have underperformed broader markets while Financials have begun to ascend of late. As a result, mutual fund schemes have not yet recovered completely from this surprising market rotation.

-

Leading mutual fund schemes have preferred to stay away from some cyclical stocks despite their recent outperformance — metals for instance. In turn, this has affected their overall return.

-

Fund houses that had created cash positions when the markets bottomed in March, were averse to going gung-ho and deploy money in the Indian equity markets on the backdrop of the challenges brought forward by the COVID-19 pandemic. Fund managers could not foresee the exceptional upturn in equities.

Notwithstanding the above it is also possible that the schemes which outperformed, churned their portfolios (chased momentum) while the ones that underperformed did everything as per their investment mandate and followed well-defined processes and systems.

You see, do not place your bets on mutual fund schemes that depend excessively on star fund managers. Remember, fund managers, do not have a magic wand. The fund manager needs to respect the mandate of the scheme and invest accordingly, not as per his/her whims and fancies. If he/she has indulged in momentum playing to clock alpha, but if the bets fell through, it would have a bearing on fund returns making them look inconsistent.

It is in your, the investors’ interest to choose mutual fund schemes from fund houses that follow robust investment systems and processes to achieve the stated invested objective (of capital appreciation).

What to do if mutual fund schemes in the portfolio have underperformed?

It is natural for you, the investor to be upset about the underperformance of schemes in your portfolio –particularly when the Indian equity markets have scaled a new all-time high.

I suggest, comprehensively review your investment portfolio seeking professional help. Here’s how a prudently carried out portfolio review would help:

- Spot mutual fund schemes that haven’t aligned their portfolios with their stated investment objectives and aren’t suitable to you as per your risk appetite

- Identify persistent underperformers and cull them out

- Replace and restructures your portfolio astutely with deserving and suitable alternatives

- Align the investments as per your risk profile, investment objective, envisioned financial goals, and the time in hand to achieve those goals

- Ensure that your portfolio is in line with your financial goals, present circumstances and asset allocation best suited for you

- Facilitate portfolio consolidation and rebalancing

- Ensure optimal structuring and diversification of the portfolio (which is one of the basic tenets of investing)

- Improve the return potential of the portfolio and make sure you are on track to accomplish the envisioned financial goals

If you conduct a comprehensive portfolio review now, it can prove to be an effective antidote that will help you deal with the risk of a deadly pathogen detrimentally impacting your investment portfolio and your long-term financial wellbeing.

This article first appeared on PersonalFN here

{kind=link}