Recent events that occurred in debt markets have enabled the RBI to lower interest rates consecutively and retain the status quo as, “accommodative stance as long as it is necessary to revive growth and mitigate the impact of COVID-19 on the economy”.

The bond yields were most affected in the last three months, after the Reserve Bank of India (RBI) announced measures to allay the market fears over rising yields and higher borrowing programmes. In fact, the bond yield and prices move in opposite directions. This happens largely because the bond market is driven by the supply and demand of capital in the system.

Since the bond price and yields are inversely proportional to each other, the fall in the yields favoured the bond prices to make debt fund investment lucrative. Debt funds with a higher maturity, which are at the longer end of the yield curve–gilt funds and long-term bond funds benefited the most due to the fall in the bond yields, but they are extremely sensitive to the interest rate movement as compared to short-term papers.

Besides this, certain norms recently introduced by the capital market regulator are making investment in debt mutual funds more transparent for the investors’ interest and better returns. In the wake of this, investing in Banking and PSU debt funds might seem like a sensible approach because they hold higher rated bonds or debt security papers that have low risk.

Therefore, ITI Mutual Fund launched ITI Banking and PSU Debt Fund, an open-ended debt scheme constructed to invest in debt and money market instruments issued by entities such as Scheduled Commercial Banks, Public Financial Institutions (PFIs), Public Sector Undertakings (PSUs) and Municipal Bonds.

The fund house is of the view that due to the following reasons, investing in banking and PSU debt fund now is a perfect investment opportunity for a period of 5 years for risk-averse investors.

- Credit spreads have widened creating opportunity to invest in high quality debt instruments at attractive yields.

- Yields are still relatively high in India compared to developed markets.

- Investment in high credit quality are potentially good investment option in the current debt market environment where default risks have gone up.

Besides a Banking and PSU debt fund, have higher share of investments in top rated Debt Instruments, enjoy the highest average exposure to liquid assets, and provide stable returns compared to most other categories.

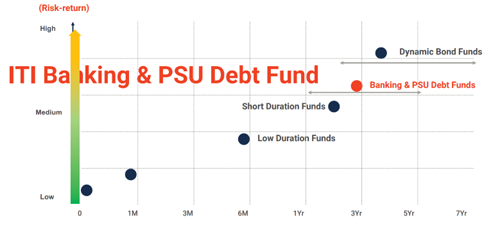

Graph: Fund’s positioning

(Source: ITI Banking &PSU Debt Fund’s Presentation)

ITI Banking & PSU Debt Fund is suitable for investors who are willing to take moderate risk and have the investment duration of more than one year, looking for stability, regular income, and high liquidity.

Table 1: ITI Banking & PSU Debt Fund

| Type | An open-ended debt scheme predominately investing in debt instruments of banks, Public Sector Undertakings, Public Financial Institutions and Municipal Bonds | Category | Banking & PSU Fund |

| Investment Objective | To generate income / capital appreciation through investments in debt and money market instruments consisting predominantly of securities issued by entities such as Scheduled Commercial Banks(SCBs), Public Sector undertakings(PSUs), Public Financial Institutions(PFIs) and Municipal Bonds. However, there can be no assurance or guarantee that the investment objective of the scheme would be achieved. |

||

| Min. Investment | Rs 5,000 and in multiples of Re 1 thereafter | Face Value | Rs 10 per unit |

| Plans |

|

Options |

|

| Entry Load | Nil | Exit Load | Nil |

| Fund Manager | Mr Milan Mody Mr George Heber Joseph |

Benchmark Index | CRISIL Banking and PSU Debt Index |

| Issue Opens: | October 05, 2020 | Issue Closes: | October 19, 2020 |

(Source: Scheme Information Document)

How will the scheme allocate its assets?

Under normal circumstances, it is anticipated that the asset allocation of the scheme will be as follows:

Table 2: ITI Banking & PSU Debt Fund’s Asset Allocation

| Instruments | Indicative Allocation (% of total assets) | Risk Profile | |

| Maximum | Minimum | ||

| Debt (including securitised debt) and Money Market Instruments issued by Scheduled Commercial Banks (SCBs), Public Sector Undertakings (PSUs), Public Financial Institutions (PFIs) and Municipal Bonds | 100 | 80 | Low to Medium |

| Debt (including government securities) and Money Market Instruments issued by entities other than the above | 20 | 0 | Low to Medium |

| Units issued by REITs & InvITs | 10 | 0 | Medium to High |

(Source: Scheme Information Document)

What is the Investment Strategy?

The Scheme shall endeavour to generate optimum returns with low credit risk. Investment in debt and money market securities issued by banks, PSU, PFI, and Municipal Bonds is primarily with the intention of maintaining high credit quality of the portfolio and to ensure safety in terms of timely repayment of interest and maturity proceeds.

The investment team of the AMC will carry out rigorous in-depth credit evaluation of the money market and debt instruments proposed to be invested in. The credit evaluation includes a study of the operating environment of the issuer, the past track record as well as the future prospects of the issuer and the short-term/ long-term financial health of the issuer.

Who will manage ITI Banking and PSU Debt Fund?

ITI Banking & PSU Debt Fund will be co-managed by Mr Milan Mody and Mr. George Heber Joseph.

Mr Milan Mody has done his BCom and MBA in Finance. He joined ITI Asset Management Limited in November 2017 and has over 17 years of work experience in Fund Management and Dealing in Fixed Income.

Before joining ITI AMC, Mr Mody, Product & Investment Manager – ZyFin Research Private Ltd from Nov 2015 to October 2017. He was managing Indian Fixed Income ETFs covering Indian Sovereign Bond ETF and PSU Corporate Bond ETF with a total assets over USD 75 million, other managed ETFs include Zyfin Turkey Sovereign Bond ETF and Zyfin MSCI India ETF in collaboration with foreign institutional players.

During his tenure he was responsible for Fund Management and Product Development covering fixed income markets. Prior to joining ZyFin Research Private Ltd, he was a Fund Manager at Sahara India Life Insurance Company Ltd managing ULIPs and Traditional scheme portfolios and he was associated with the company from November 2005 till October 2015. During his tenure he has managed six ULIP schemes with participating and nonparticipating funds (traditional schemes) along with his team. He was also associated with debt Intermediaries like Darashaw and BRICS securities (who caters to institutional investors and FPIs in Wholesale Debt Market from 2002 to 2005.

At the fund house currently, he co-manages ITI Liquid Fund, ITI Overnight Fund, and ITI Arbitrage Fund.

Mr George Heber Joseph is the Chief Executive Officer (CEO) and Chief Investment Officer (CIO) at ITI Mutual Fund. He holds a bachelor’s degree in English language & Literature (BA) and commerce (BCom). Mr George is also a qualified member of associate member of Chartered Accountants of India and an associate member of Cost and Management Accountants of India. He has over 16 years of work experience in Fund Management, Equity Research and Capital Markets.

Prior to joining, ITI Mutual Fund, he was working as a Senior Fund Manager (Vice President Grade & Key Management Personnel) at ICICI Prudential Asset Management Co. Ltd. handling two flagship funds. He was associated with the Fund Management Team of ICICI Prudential Asset Management Company Limited for nearly a decade tracking various sectors and a wide variety of stocks.

During his tenure, he was also heading the Portfolio Management Services Division, was responsible to oversee fund managers activities, managing research analysts, performance measurement, and worked as a sounding board for fund managers as well. Before that, in his previous assignments, he has been associated with organisations like DSP Merrill Lynch Ltd, Wipro Ltd, MetLife India, Cholamandalam Investments & Finance Company Ltd and Tanfac Industries Ltd where he has handled fund management and corporate treasury responsibilities.

Some of the other schemes co-managed by Mr George Heber Joseph include ITI Liquid Fund, ITI Multi-Cap Fund, ITI Long Term Equity Fund, ITI Arbitrage Fund, ITI Overnight Fund, ITI Balanced Advantage Fund.

Table 3: Performance of Schemes managed by both the fund managers

| Scheme Name | Scheme Benchmark | Managing since | Scheme returns (%) | Benchmark returns (%) |

| ITI Liquid Fund | Crisil Liquid Fund Index | Apr-19 | 4.38 | 5.68 |

| ITI Arbitrage Fund | Nifty 50 Arbitrage Index | Sep-19 | 4.44 | 2.91 |

| ITI Overnight Fund | Crisil Composite Bond Fund Index | Oct-19 | 3.48 | 10.39 |

Data as on October 8, 2020

(Source: ACE MF; PersonalFN Research)

As seen from the table above, the schemes co-managed by both fund managers haven’t been performing well. Besides, the funds have barely completed a year. Hence this doesn’t give in much confidence.

Outlook for ITI Banking & PSU Debt Fund

The Indian fixed income market, one of the largest and most developed in South Asia, is well integrated with the global financial markets. The RBI reviews the monetary policy six times a year, giving guidance to the market on direction of interest rate movement, liquidity, and credit expansion. The central bank has been operating as an independent authority, formulating the policies to maintain price stability and adequate liquidity.

But RBI has successively cut interest rates to boost the waning economy. In the falling interest rate scenario, these funds benefitted from capital appreciation.

Interest rates on small savings schemes and Bank deposits have been on the decline since RBI started reducing policy rates. So, if you are willing to take slightly higher risk for higher returns, Banking and PSU funds can be considered as a worthy alternative to these investments.

[Read: Why Banking and PSU Debt Funds Are Grabbing Investors’ Attention]

Do note that while credit risk in this category is low, it is prone to interest rate fluctuations. When interest rates rise, these funds generate lower returns. Interest rate risk associated with debt instruments depends on the macroeconomic environment. It includes the market price changes due to change in yields as well as coupon reinvestment rate risk. Corporate papers carry higher liquidity risk as compared to gilts due to the depth of the gilt market.

So, ITI Banking & PSU Debt Fund may be affected, inter alia, by changes in the market conditions, interest rates, trading volumes, settlement periods, and transfer procedure.

This article first appeared on PersonalFN here

{kind=link}